Quick answer: The IRS offers four formal tax debt relief programs: Installment Agreements, Offers in Compromise, Currently Not Collectible status, and Penalty Abatement. The right one depends on your numbers — what you owe, what you can pay, and how the IRS scores your assets. Anyone selling a ‘one-size-fits-all’ program is selling you something the IRS doesn’t actually have.

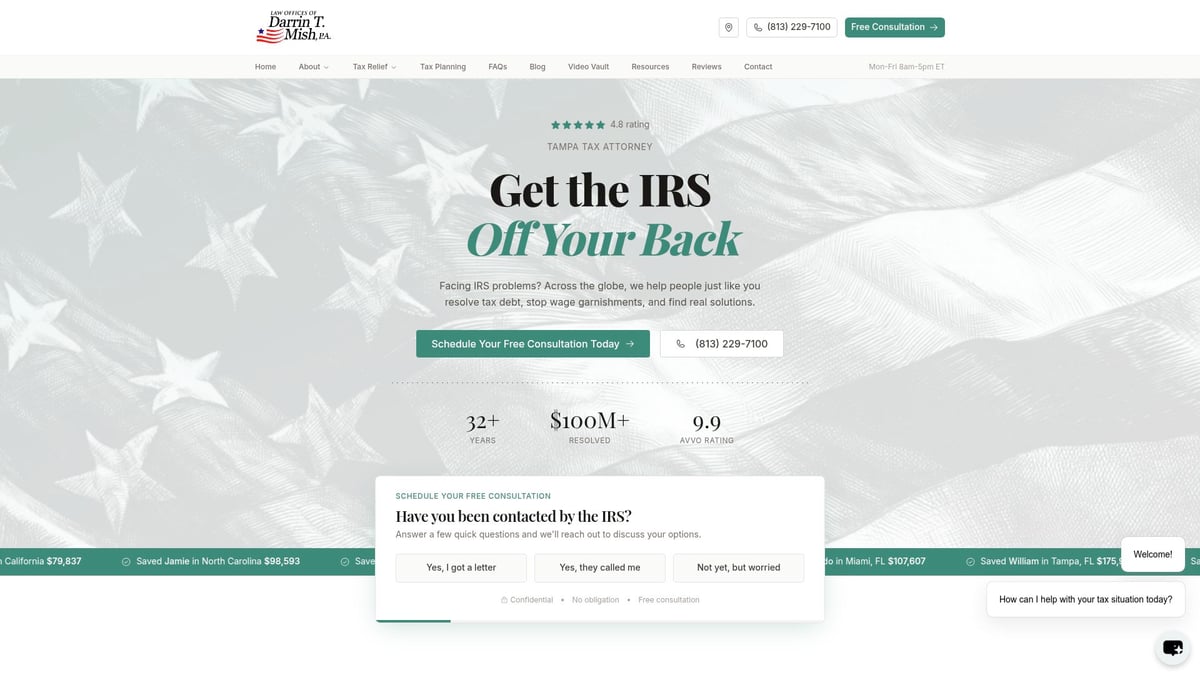

I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Are you feeling overwhelmed by IRS tax debt? If so, you are definitely not alone. Every year, millions of Americans find themselves searching for answers and relief.

The good news is, you have more options than you might think. This guide breaks down the most important irs tax debt relief programs for 2026, showing you how to take control and move toward financial stability.

We will walk through proven solutions, explain who qualifies, outline the steps involved, and share expert tips so you can make informed decisions. Ready to turn stress into a plan of action? Let us get started.

Understanding IRS Tax Debt and Its Consequences

Finding yourself tangled in IRS tax debt can feel like quicksand. The good news? You are not alone. Millions of Americans wrestle with the same challenge, making it crucial to understand what IRS tax debt actually is and how irs tax debt relief programs can help you escape its hold.

What Constitutes IRS Tax Debt?

IRS tax debt is simply any unpaid federal tax you owe under U.S. law. This debt can build up for many reasons. Maybe you underpaid during the year, forgot to file a return, or made a miscalculation on your taxes. Small business owners might run into issues if they misclassify workers or miss payroll tax deadlines.

Here are some common causes:

- Underpayment due to inaccurate withholding

- Failure to file annual returns

- Math or reporting errors

- Business payroll tax mistakes

For example, someone working multiple jobs might not have enough withholding, leading to a surprise bill at tax time. Or, a small business could face IRS tax debt after missing quarterly estimated payments.

If you are facing these scenarios, exploring IRS tax relief program options can be a practical first step. These programs are designed to help taxpayers just like you find a manageable way out.

Immediate and Long-Term Consequences

What happens if you ignore your IRS tax debt? The IRS does not just wait around. Collection actions can include liens on your property, levies that seize your bank funds, or wage garnishments that take money directly from your paycheck.

Here’s a quick comparison of actions and penalties:

| Action | Impact |

|---|---|

| Lien | Claim on property, hurts credit score |

| Levy | Seizure of funds/assets |

| Wage Garnish | Deducts from paycheck until debt is paid |

On top of that, your credit score can drop, and you may face financial restrictions when seeking loans or credit cards. Penalties and interest pile up fast – late payment penalties alone can reach 25 percent of the original debt.

In 2023, the IRS issued over 780,000 levies and 543,000 liens. These numbers show how serious the agency is about collecting what is owed, and why attention to irs tax debt relief programs is so important.

Why Tax Debt Relief is Critical

Carrying IRS tax debt is not just a financial issue. It can lead to sleepless nights, anxiety, and even put your home or business at risk. The threat of asset seizure or forced business closure is real if you do not take action.

Timely intervention through irs tax debt relief programs is often the difference between regaining control and spiraling deeper into crisis. Acting quickly can minimize penalties, stop collection actions, and help you reclaim your peace of mind.

If you are feeling overwhelmed, remember that help is available. Addressing your IRS tax debt early opens up more options and gives you a fighting chance to rebuild your financial future.

Overview of IRS Tax Debt Relief Programs in 2026

Feeling lost in a sea of tax notices and IRS letters? If you're looking for real solutions, you're in the right place. The IRS tax debt relief programs in 2026 offer a variety of paths to help you regain control of your finances. Each program is designed for different situations, so understanding your options is the first step toward relief.

Offer in Compromise (OIC)

Have you heard of the Offer in Compromise? This cornerstone of irs tax debt relief programs lets you settle your tax debt for less than the full amount. It's designed for people who simply can't pay what they owe, even over time.

In 2023, around 33% of OIC applications were accepted. To qualify, you must prove that paying the full amount would cause financial hardship. The IRS looks at your income, expenses, assets, and ability to pay. Imagine finally seeing a light at the end of the tunnel, knowing you could resolve your tax debt for a fraction of what you owe. For a deeper dive into the process, check out this Offer in Compromise explained resource.

Installment Agreements

Not everyone can pay their tax bill at once. Luckily, irs tax debt relief programs include several types of installment agreements. These allow you to break your debt into manageable monthly payments.

There are guaranteed, streamlined, and partial payment plans. In 2023, over 2.1 million installment agreements were approved, helping taxpayers avoid more aggressive IRS actions. If you qualify, you can set up a plan based on your balance and ability to pay. This structured approach might be just what you need to stay on track and avoid future issues.

Currently Not Collectible (CNC) Status

Sometimes, life throws curveballs that make any payment impossible. That's where the CNC status comes in as part of irs tax debt relief programs. If you can show the IRS that paying anything right now would create a serious financial hardship, they can temporarily pause all collection actions.

While your debt doesn't go away, this status gives you breathing room until your situation improves. Penalties and interest continue to accrue, but you won't face levies or garnishments during this period. It's a lifeline for those in genuine crisis.

Penalty Abatement and Interest Relief

Penalties can pile up fast, making your tax debt even scarier. The irs tax debt relief programs offer penalty abatement if you qualify. First-time penalty abatement is available if you have a good track record with the IRS.

There's also reasonable cause relief for situations like illness or natural disaster. Sometimes, just one phone call or letter can wipe away hundreds or even thousands in penalties. Interest relief is harder to get, but not impossible in rare cases.

Innocent Spouse Relief

Tax problems can get complicated when joint returns are involved. If your spouse made mistakes or hid information, the IRS tax debt relief programs provide Innocent Spouse Relief. This program protects you from being held responsible for a partner’s errors or fraud.

There are three types: innocent spouse, separation of liability, and equitable relief. Each is tailored for different circumstances, so you can find the one that fits your story.

Other Specialized Programs

Beyond the main irs tax debt relief programs, help is available for unique situations. The Taxpayer Advocate Service offers free, independent support if you're facing delays or hardship.

Victims of natural disasters, identity theft, or other emergencies may qualify for special relief programs. No matter your circumstances, there’s likely a program that can offer support and guidance through the IRS process.

Step-by-Step Guide: How to Apply for IRS Tax Debt Relief

Feeling overwhelmed by the process of applying for irs tax debt relief programs? You are not alone. The path to tax debt relief can seem confusing, but breaking it down into clear steps makes it manageable. Let us walk through each stage together, so you know exactly what to expect and how to prepare for a smooth application.

Step 1: Assess Your Tax Debt and Financial Situation

Start by getting a clear picture of your tax debt. Request your IRS account transcripts and review any notices you have received. List out all tax years involved, the total amount owed, and any penalties or interest that have been added.

Understanding your full financial situation is essential for irs tax debt relief programs. Gather details on your monthly income, living expenses, assets, and liabilities. This information will guide your next steps and help you choose the most suitable relief program.

Being honest with yourself here sets a strong foundation for success.

Step 2: Determine Eligibility for Relief Programs

Review the IRS guidelines to see which irs tax debt relief programs match your situation. The IRS offers several options, including Offer in Compromise, Currently Not Collectible status, and payment plans.

To check if an installment plan is right for you, visit the Installment Agreement payment plans page for details on structured repayment options. Also, try the IRS pre-qualifier tools to get an initial sense of eligibility for programs like Offer in Compromise.

Remember, every program has specific requirements based on your income, assets, and household size.

Step 3: Gather Required Documentation

Having your paperwork ready makes applying to irs tax debt relief programs much smoother. Collect recent pay stubs, bank statements, bills, and proof of expenses. If you are claiming financial hardship, include documents showing medical costs, unemployment, or other relevant factors.

You will also need to provide details about your home, vehicles, and retirement accounts. Double-check that all documents are current and accurate. Missing information can delay your application or lead to a denial.

Organize your files in a folder or digitally for easy access.

Step 4: Complete and Submit Applications

Now it is time to fill out the necessary IRS forms. The most common forms for irs tax debt relief programs are 433-A (Collection Information Statement for Wage Earners), 433-F (for individuals), and 656 (for Offer in Compromise).

Read each form's instructions carefully. A common mistake is leaving sections blank or providing inconsistent information. Double-check your entries and consider having a trusted advisor review everything before submission.

Submit your application by mail or online, depending on the program's requirements.

Step 5: Communicate with the IRS

After submitting your application, stay alert for any correspondence from the IRS. They may request additional documents or clarification, especially when evaluating irs tax debt relief programs.

Respond promptly to all requests. Clear, timely communication can help avoid misunderstandings and keep your case moving forward. If you receive a counter-offer or a request for negotiation, review it carefully before accepting or making changes.

Keep a log of all communications and copies of every document sent.

Step 6: Monitor Your Application Status

Each irs tax debt relief program has its own review timeline. Some decisions arrive within weeks, while others may take several months. You can check your application status online through your IRS account or by calling the IRS directly.

It is a good idea to set reminders to follow up if you have not heard back within the expected timeframe. Keeping track of your status ensures you do not miss important updates or deadlines.

Stay patient, but persistent, throughout the process.

Step 7: Fulfill Ongoing Obligations

Once approved for irs tax debt relief programs, your work is not over. You must stay compliant with future tax filings and payments to maintain your relief status. Missing a deadline or defaulting on an agreement can reinstate your full debt and penalties.

Set up calendar alerts for tax due dates. Keep all records organized and consider regular check-ins with a professional if your situation is complex.

By staying proactive, you secure long-term financial stability and peace of mind.

Key Considerations and Common Pitfalls in IRS Relief Applications

Facing the IRS can feel overwhelming, especially when applying for irs tax debt relief programs. Even with the best intentions, many people stumble over avoidable mistakes. Knowing what to watch for can mean the difference between quick approval and frustrating rejection.

Understanding Eligibility Complexities

Eligibility for irs tax debt relief programs is rarely as straightforward as it seems. Many people think they automatically qualify, but the IRS examines your income, assets, expenses, and even household size. Changes to programs, like those discussed in the IRS Fresh Start Program qualifications in 2026, can shift requirements from year to year.

Before applying, review the latest IRS guidelines. Use pre-qualifier tools to gauge your chances. Misunderstanding these details is a common pitfall.

Documentation Errors and Omissions

Submitting incomplete or inaccurate paperwork is a leading cause of rejection for irs tax debt relief programs. Double-check all forms for missing signatures, incorrect Social Security numbers, or forgotten attachments.

- Always gather proof of income, expenses, and assets.

- Keep copies of everything you submit.

- If unsure, ask a professional to review your documents.

A small mistake can set your application back for weeks or months.

Navigating IRS Communication

Timely responses to IRS requests are crucial when pursuing irs tax debt relief programs. The IRS may send follow-up letters or request more information. Ignoring or delaying your reply can lead to automatic denials or missed deadlines.

Be proactive. Open every letter, read it carefully, and respond within the given timeframe. If you receive a notice you do not understand, seek help immediately.

Impact of Professional Representation

Working with a tax professional or attorney can significantly boost your chances of success with irs tax debt relief programs. Experts know what the IRS is looking for and how to present your case clearly. Statistics show higher acceptance rates for those who have professional guidance.

- Professionals help avoid costly mistakes.

- They can communicate directly with the IRS on your behalf.

- Legal experts are invaluable if your case is complex.

Consider consulting a specialist if you are unsure about any part of the process.

Avoiding Scams and Unqualified Providers

Unfortunately, the world of irs tax debt relief programs is also filled with scams. Beware of companies that promise guaranteed results or ask for large upfront fees.

- Verify credentials before hiring anyone.

- Be skeptical of “too good to be true” offers.

- Check reviews and look for complaints with the Better Business Bureau.

Your financial future is too important to trust to unqualified providers.

Reapplying After Rejection

If your application for irs tax debt relief programs is denied, do not lose hope. Many people succeed on their second try by addressing the reasons for rejection and providing new evidence.

- Carefully review your denial letter.

- Fix any errors and gather additional documentation.

- Note the waiting period before reapplying.

Persistence and preparation can make a real difference in your outcome.

Working with a Tax Attorney: When and Why It Matters

Are you wondering if you really need a tax attorney when dealing with irs tax debt relief programs? For many, the idea of involving a lawyer sounds intimidating, but the reality is that professional legal help can make all the difference – especially when the IRS is knocking on your door. Let’s break down when to seek help, what attorneys can do for you, and how to make the most of their expertise.

Complex Cases and High-Stakes Situations

Not every tax issue calls for an attorney, but some situations absolutely do. If you owe a large amount, face a business tax audit, or are being investigated for possible fraud, you’re in high-stakes territory. The IRS takes aggressive action in these scenarios, and mistakes can cost you dearly.

You might need a tax attorney for irs tax debt relief programs if:

- Your tax debt is six figures or more

- You’re facing an IRS audit or criminal investigation

- Your business is at risk of closure due to tax issues

In these situations, professional legal help isn’t just helpful – it’s critical for protecting your assets and your future.

Advantages of Legal Representation

Why should you consider an attorney over handling things solo? Tax attorneys offer more than just paperwork. They negotiate directly with the IRS, develop custom legal strategies, and represent you in appeals or hearings. With irs tax debt relief programs, having a seasoned negotiator can significantly increase your chances of success.

For example, when applying for an Offer in Compromise, success rates are higher for those who use professional representation. If you want to understand the process and your odds, check out this guide on Offer in Compromise acceptance rates and process.

Attorneys also shield you from direct IRS pressure, giving you more breathing room to focus on your life.

Law Offices of Darrin T. Mish, P.A.: Expert IRS Tax Debt Relief Representation

When it comes to irs tax debt relief programs, experience matters. The Law Offices of Darrin T. Mish, P.A. brings over 32 years of hands-on experience resolving over $100 million in tax debt. Their services cover everything from wage garnishment releases and levy removals to penalty abatements and Offers in Compromise.

Clients appreciate their free, confidential consultations, which help you explore solutions tailored to your situation. With high success rates and glowing testimonials, this firm stands out as a reliable partner in your IRS journey.

When to Seek Attorney Help

Are you facing aggressive IRS tactics, like wage garnishments or bank levies? Have you tried irs tax debt relief programs before and been denied? Or do you have years of complicated, backlogged tax issues? These are all signs it’s time to bring in an expert.

A tax attorney can step in and:

- Stop or reverse collection actions

- Reopen denied cases with new evidence

- Navigate multi-year or business tax debt

Acting early gives your attorney the best chance to secure a positive outcome.

Understanding Attorney Fees and Consultations

Worried about the cost? Most tax attorneys offer a free initial consultation, so you can discuss your case without pressure. Fees vary based on complexity, but reputable lawyers are upfront about their pricing models – flat fees, hourly rates, or contingency arrangements.

During your consultation, ask what’s included, how communication works, and what results to expect. Investing in expert help often pays off by saving you far more in the long run.

Staying Compliant After IRS Tax Debt Relief

Getting relief through irs tax debt relief programs is a huge step toward financial freedom, but the journey doesn’t end there. Staying compliant is essential to protect your progress and avoid falling back into old patterns. Let’s break down the most important strategies so you can keep your finances on track for the long haul.

Importance of Ongoing Tax Compliance

Once you benefit from irs tax debt relief programs, you must follow the IRS terms closely. This means filing all future tax returns on time and paying any new taxes you owe. If you miss a filing or payment, the IRS can revoke your relief agreement, and you could face renewed penalties or enforcement actions.

The IRS watches for compliance after granting relief. If you stay current, you avoid extra stress and keep your agreement in good standing. Remember, even one missed deadline can put your financial progress at risk.

Best Practices for Future Tax Filings

Staying on top of your tax filings is critical. Use the IRS e-file system for faster, more accurate returns, and set calendar reminders so you never miss a deadline. Double-check your information to prevent errors that could trigger audits or penalties.

If you have past-due returns, address them quickly. The IRS recently provided penalty relief for 2020 and 2021 tax returns, helping millions avoid further charges. Staying aware of such updates can save you money and stress.

Proactive Tax Planning and Financial Management

Planning ahead is your best defense against future tax debt. Start by budgeting for your tax obligations each month. Review your income and expenses, and set aside a portion for taxes so you’re never caught off guard.

Take advantage of tax credits and deductions. These can lower your overall tax bill and make compliance easier. If you’re unsure which benefits you qualify for, consider consulting a tax professional who understands irs tax debt relief programs.

Consequences of Default or New Noncompliance

Defaulting on your agreement or creating new tax debt can undo all your hard work. If you fall behind, the IRS may reinstate your full debt, add new penalties, and resume collections like wage garnishments.

New noncompliance can also block you from using irs tax debt relief programs again. Protect your progress by catching up quickly if you slip. Communication with the IRS is key if you anticipate payment trouble.

Accessing IRS Educational Resources and Support

The IRS offers many resources to help you stay compliant. Explore the IRS Taxpayer Advocate Service, free online tools, and official guides for up-to-date information. Community organizations and non-profits can also offer support, especially if your situation is complex.

Don’t hesitate to reach out for help if you feel overwhelmed. Many people who use irs tax debt relief programs benefit from ongoing education and support.

Building Long-Term Financial Stability

After resolving your tax debt, focus on creating a stable financial future. Build an emergency fund to cover unexpected expenses, and review your finances regularly to spot potential issues early.

Consider seeking ongoing professional guidance for tax planning. With the right strategies and support, you can use irs tax debt relief programs as a springboard toward lasting stability and peace of mind.

Frequently Asked Questions

When do I need a tax attorney instead of a CPA or enrolled agent?

When your case has criminal exposure, complex litigation posture, or attorney-client privilege as a strategic tool. For straightforward Installment Agreements, a CPA or EA is often the right choice. For audits, Trust Fund Recovery, Tax Court, or anything with potential criminal elements, the attorney premium is justified.

What does a tax attorney consultation cover?

A typical first consultation is 20 to 30 minutes, free, and covers your specific situation, your IRS letters and deadlines, your finances, available resolution options, expected fee range, and whether the firm is the right fit. There is no obligation to engage.

How much does a tax attorney cost?

Tax resolution cases typically range from $5,000 to $25,000 depending on complexity. Trust Fund Recovery defense and Tax Court litigation are higher. The fee is usually a small percentage of what is at stake when proper representation works.

Does hiring a tax attorney trigger an audit?

No. The IRS does not flag taxpayers because they hired representation. Having a Form 2848 Power of Attorney on file usually makes the case run more efficiently.

What is attorney-client privilege in tax cases?

Communications between you and your tax attorney are protected and cannot be compelled in litigation. Communications with a CPA generally have no such protection. The privilege is critical when criminal exposure is possible.

Can a tax attorney negotiate with the IRS for me?

Yes. Once a Form 2848 Power of Attorney is filed, the IRS communicates with your attorney instead of you. The attorney negotiates Installment Agreements, Offers in Compromise, penalty abatements, and represents you in audits and appeals.