If you've got an IRS letter on your desk right now, you have a decision to make, and the clock matters. I'm Darrin Mish. I've spent 32 years helping people with exactly this kind of situation. Here's what you should do.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

You're on Social Security Disability Insurance, the IRS says you owe money, and you just heard they can take part of your check. True. But not the nightmare scenario you're imagining. Understanding ssdi irs garnishment 2026 rules means knowing the limits, the process, and what you can do before a dollar disappears from your account.

Most taxpayers assume SSDI is untouchable. It's not. Federal law exempts Social Security benefits from most creditors-but not from other federal agencies. The IRS has specific authority under 26 U.S.C. § 6331 and the Federal Payment Levy Program to intercept disability payments for unpaid tax debt.

How SSDI IRS Garnishment 2026 Actually Works

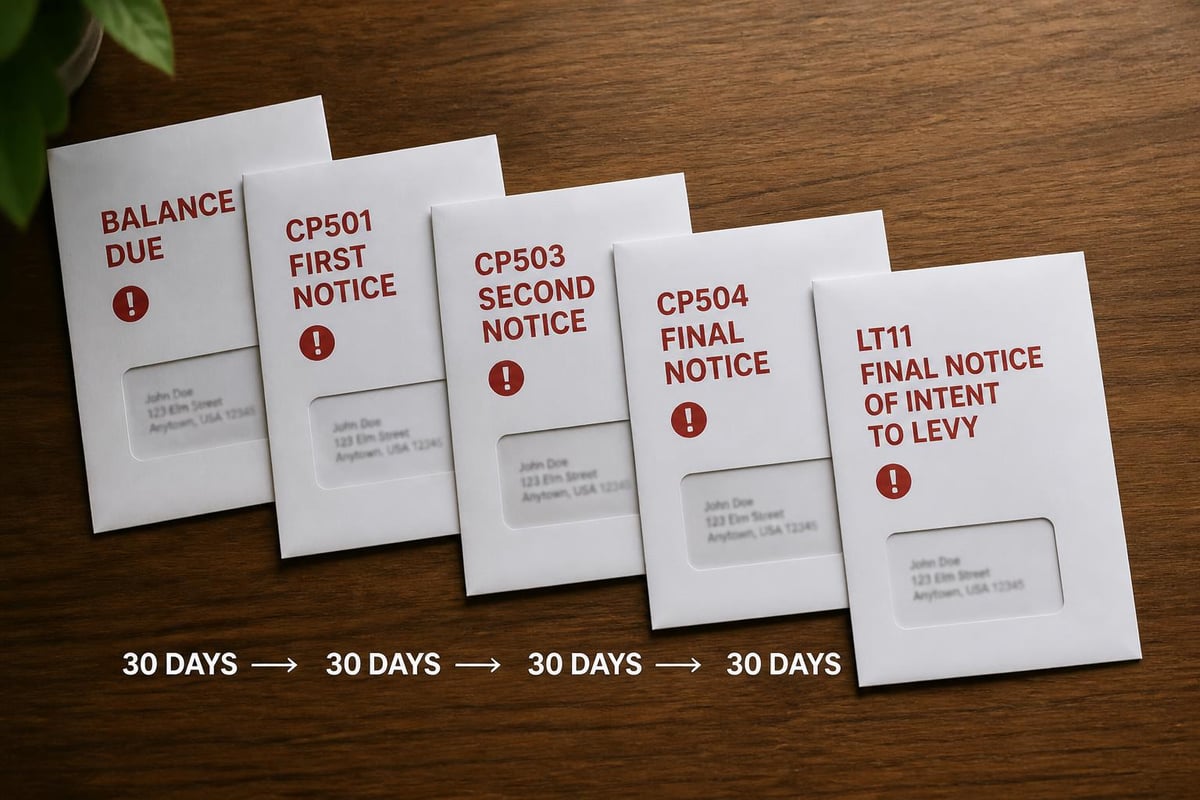

The IRS doesn't just grab your money without warning. They send notices. Lots of them.

First comes the assessment. The IRS calculates what you owe and sends a Notice and Demand for Payment. You get that letter, you've got options. Ignore it, and you're heading down a narrower path. After multiple notices-CP501, CP503, CP504, and finally a Letter 1058 (Final Notice of Intent to Levy)-you have 30 days to respond before the IRS can start collection actions.

When the IRS moves to garnish SSDI, they use the Federal Payment Levy Program (FPLP). This program intercepts payments automatically through the Bureau of the Fiscal Service. Unlike wage garnishment where your employer gets the notice, this happens at the federal payment level before the money hits your bank account.

The 15 Percent Limit

Here's the number that matters: 15 percent. That's the maximum the IRS can take from your SSDI under the FPLP for most cases. If you receive $1,500 per month in disability benefits, the IRS can garnish up to $225. That's federal law under 31 U.S.C. § 3716(c)(3)(A)(ii).

This is dramatically different from wage garnishment, where the IRS can take considerably more based on filing status and dependents. With SSDI, the 15 percent cap applies regardless of your household size or other income.

One continuous levy. The IRS doesn't have to send a new notice each month. Once the levy attaches, it stays attached until the debt is paid or you work out an alternative arrangement. Month after month, 15 percent comes off the top.

When SSDI Protection Doesn't Apply

Not every Social Security payment gets the same protection. Supplemental Security Income (SSI) cannot be garnished by the IRS-period. SSI is a needs-based program under Title XVI of the Social Security Act, and federal law fully protects those payments from federal tax levies.

SSDI operates under Title II. Different rules. You paid into the system through payroll taxes, you became disabled, you receive benefits based on your work history. The IRS sees that as income they can reach.

Timing matters too. SSDI back pay can be particularly vulnerable. If you receive a lump sum for months or years of retroactive benefits, the IRS can levy the entire amount if you owe tax debt. There's no 15 percent limit on a lump sum sitting in your bank account after deposit. The FPLP limit applies only to ongoing monthly payments.

The Taxability Question

Some SSDI recipients owe tax in the first place because their disability benefits are partially taxable. If your combined income (adjusted gross income plus nontaxable interest plus half of your Social Security benefits) exceeds certain thresholds, up to 85 percent of your SSDI becomes taxable.

For 2026, those thresholds haven't changed in decades:

| Filing Status | Threshold for 50% Taxable | Threshold for 85% Taxable |

|---|---|---|

| Single | $25,000 | $34,000 |

| Married Filing Jointly | $32,000 | $44,000 |

You file single, receive $1,800 monthly SSDI ($21,600 annually), have $15,000 in other income-you're over the threshold. Part of your disability benefit becomes taxable income. Don't report it, don't pay the tax, and eventually you face ssdi irs garnishment 2026 on the very income that created the debt.

What to Do When You Get the Notice

Thirty days. That's your window after the Final Notice of Intent to Levy. You can request a Collection Due Process (CDP) hearing. This stops the levy while the IRS Office of Appeals reviews your case.

At the CDP hearing, you can propose alternatives:

- Installment agreement: Monthly payments you can actually afford based on your income and expenses

- Offer in Compromise: Settle the debt for less than the full amount if you qualify

- Currently Not Collectible status: The IRS temporarily stops collection if you have no ability to pay

- Penalty abatement: Challenge penalties if you have reasonable cause

I've watched taxpayers on SSDI negotiate payment plans as low as $25 per month when that's what their budget allows. The IRS would rather have $25 a month than garnish 15 percent and leave someone unable to pay rent.

The key is responding. Miss that 30-day deadline, and your options narrow. You can still request a levy release or propose alternatives, but you lose the automatic hold that comes with a timely CDP hearing request.

SSDI Garnishment Versus Other IRS Collection Actions

The IRS has a menu of collection tools. Garnishing your SSDI sits in the middle-more aggressive than filing a Notice of Federal Tax Lien, less devastating than levying your bank account or seizing assets.

A lien is a public claim against your property. It wrecks your credit and attaches to anything you own, but it doesn't take money from your pocket today. Federal tax liens follow you until the debt is paid or the 10-year collection statute expires.

A bank levy is a one-time grab. The IRS orders your bank to freeze your account and send whatever's in there. If your SSDI was directly deposited yesterday and you've got $4,500 in your account, the IRS can take it all unless you prove it came from protected sources within the lookback period. Treasury regulations provide some protection, but it requires paperwork and proof.

Continuous SSDI garnishment under FPLP is cleaner in some ways. You know exactly what's coming out each month. It's predictable. Still terrible, but predictable.

When Disability Affects Your Tax Case

Being on SSDI sometimes creates grounds for relief beyond standard collection alternatives. If your disability prevents you from managing your financial affairs, you might qualify for currently not collectible status or an Offer in Compromise based on doubt as to collectibility.

The IRS considers serious illness and disability as factors in determining reasonable collection potential. If your only income is SSDI and you have ongoing medical expenses, your ability to pay may be close to zero. Document it properly, and the IRS might accept $0 monthly payment or settle the debt for pennies on the dollar.

I've resolved cases where the taxpayer's cognitive disability meant they genuinely couldn't manage complex financial obligations. The IRS closed the account as currently not collectible, no monthly payment required. But you've got to prove it with medical documentation, not just claim hardship.

Protecting Your SSDI Before Garnishment Starts

Prevention beats defense. If you owe tax debt and you're on disability, address it before the Final Notice arrives.

File all required returns first. Can't negotiate if you're not in compliance. Every year you didn't file gives the IRS leverage and adds failure-to-file penalties. Those penalties compound-5 percent per month up to 25 percent of the tax due. Filing unfiled returns clears the compliance roadblock.

Then look at payment options. The IRS Fresh Start Program expanded access to installment agreements and Offers in Compromise. If you owe less than $50,000, you can often set up a payment plan online without providing detailed financial statements.

Owe more? You'll submit Form 433-A (Collection Information Statement for Wage Earners and Self-Employed Individuals) or Form 433-F (Collection Information Statement), showing income, expenses, assets, and liabilities. With SSDI as your only income, your allowable expenses often exceed your income. That's how you qualify for currently not collectible or a low Offer amount.

| Option | Best For | Key Requirement |

|---|---|---|

| Installment Agreement | Steady income, manageable debt | Can pay off within 72 months |

| Currently Not Collectible | Income below allowable expenses | Financial statement proving hardship |

| Offer in Compromise | Unlikely to ever pay full amount | Detailed financial disclosure |

| Penalty Abatement | First-time penalty or reasonable cause | Clean compliance history or documented hardship |

Each option requires different forms and proof. Miss a step, and the IRS denies the request. The garnishment proceeds while you scramble to fix the application.

Special Situations: SSA Overpayments and IRS Debt

Sometimes you're fighting collection on two fronts. The Social Security Administration overpays you, decides you weren't entitled to certain benefits, and demands repayment. At the same time, the IRS wants their cut.

SSA can withhold up to 50 percent of your monthly benefit to recover overpayments-far more than the IRS's 15 percent limit. But these are separate processes. The IRS doesn't care that SSA is already clawing back half your check. They'll still take their 15 percent of the gross amount before SSA's withholding.

You receive $2,000 in SSDI. SSA withholds $1,000 for an overpayment. Your net is $1,000. The IRS calculates their levy on the gross $2,000 and takes $300. Now you're down to $700 for the month. That's when people call in a panic.

Both agencies offer appeal rights and repayment plans. For SSA, you can request a lower withholding amount or appeal the overpayment determination entirely. For the IRS, you can use the collection alternatives already discussed. But you've got to work both cases. They won't coordinate for you.

State Taxes and SSDI Garnishment

Federal tax debt triggers the ssdi irs garnishment 2026 process through FPLP. State tax debt is a different animal. Florida has no state income tax, so if you're in Tampa, you're clear. But if you lived in another state before moving or owe tax to a state where you previously worked, state revenue agencies can pursue collection.

Most states cannot garnish Social Security benefits because of federal preemption under 42 U.S.C. § 407. But states can levy bank accounts after the SSDI deposits. Once the money leaves the federal payment system and lands in your checking account, state law governs what creditors can reach.

Some states provide exemptions for funds traceable to Social Security. Others require you to prove the source and claim the exemption affirmatively. Miss the deadline to challenge the levy, and the bank sends your money to the state.

Federal tax debt is cleaner in this sense. The IRS follows federal rules uniformly. State tax debt means learning 50 different collection systems.

How Long Can the IRS Garnish SSDI?

The IRS has 10 years from the date of assessment to collect tax debt. That's the Collection Statute Expiration Date (CSED) under 26 U.S.C. § 6502. Once it expires, the debt is gone. No extension, no revival.

But certain actions toll (pause) the statute:

- Filing bankruptcy adds the time the automatic stay is in effect plus six months

- Requesting a CDP hearing tolls the statute while the case is pending

- Submitting an Offer in Compromise tolls it during consideration and for 30 days after rejection

- Living outside the U.S. for six months or more tolls the statute

If the IRS assessed your 2016 tax debt in April 2017, the CSED is April 2027-unless tolling events extended it. The IRS can garnish your SSDI through FPLP until that date or until the debt is paid, whichever comes first.

After 32 years, I've seen taxpayers tough it out and wait for the statute to expire. High-risk strategy. The IRS can file a suit to reduce the assessment to judgment before the CSED, which creates a 20-year collection period. Or you live month to month with 15 percent gone, counting down to expiration.

Common Myths About SSDI and IRS Garnishment

Myth one: All Social Security is protected. False. SSI is protected. SSDI is not.

Myth two: The IRS takes everything. False. The 15 percent limit applies to monthly payments under FPLP. They can take more from lump sums or through other levy types, but not from your ongoing monthly SSDI check.

Myth three: Once garnishment starts, you're stuck. False. You can still request a levy release, propose a payment plan, or apply for currently not collectible status after the garnishment begins. The IRS releases the levy if you enter a collection alternative agreement.

Myth four: Hiring a tax attorney stops the garnishment immediately. False. A power of attorney doesn't create an automatic hold. We can request a levy release and negotiate a resolution, but the garnishment continues until the IRS agrees to an alternative or we get a CDP hearing scheduled.

Myth five: The IRS won't negotiate if you're on disability. False. Your income source doesn't disqualify you from any resolution program. I've negotiated Offers in Compromise, installment agreements, and CNC status for hundreds of taxpayers whose only income was SSDI. The IRS cares about your ability to pay, not the label on your income.

What Happens to the Garnishment in Different Scenarios

You enter an installment agreement: The FPLP levy releases once the agreement is active and you make your first payment. You're back to receiving your full SSDI check, minus only the monthly payment you agreed to.

You're placed in currently not collectible status: The levy releases. The IRS stops all collection activity. Your full SSDI check resumes. The debt doesn't disappear, but collection is paused, often until your financial situation improves or the statute expires.

Your Offer in Compromise is accepted: You pay the offer amount, the levy releases, and the remaining debt is forgiven. You're done.

You file bankruptcy: The automatic stay stops the levy immediately. Chapter 7 might discharge some tax debt if it meets specific criteria (tax returns filed on time, debt at least three years old, assessment at least 240 days old, no fraud or evasion). Chapter 13 lets you pay tax debt over three to five years while stopping collection.

You ignore everything: The garnishment continues at 15 percent monthly until the debt is paid or the collection statute expires. Could be years. Could be a decade.

Documentation You Need

When you're facing ssdi irs garnishment 2026 or trying to prevent it, gather these documents before contacting the IRS or a tax attorney:

- All IRS notices, especially the Final Notice of Intent to Levy (Letter 1058 or LT11)

- Proof of your SSDI income (SSA-1099 forms, benefit statements)

- Bank statements showing deposits and expenses

- Medical bills and documentation of disability-related expenses

- Statements for all debts (mortgage, car loan, credit cards, medical bills)

- Pay stubs if you have any other income

- Tax returns for all unfiled years

The IRS makes decisions based on documentation, not stories. Claiming hardship without proving income and expenses gets you nowhere. Every collection alternative requires Form 433-A or 433-F unless you qualify for a streamlined installment agreement. Fill those forms out incorrectly, and the IRS rejects your request.

I've seen cases stall for months because the taxpayer didn't include a complete bank statement or left off a vehicle. The IRS sends it back, you correct it, they review again. Meanwhile, the garnishment continues.

The ssdi irs garnishment 2026 rules give the IRS clear authority to take 15 percent of your monthly disability check, but they also give you options to stop it or avoid it entirely. Whether you need an installment agreement, currently not collectible status, or an Offer in Compromise depends on your full financial picture-and the IRS won't figure that out for you. Law Offices of Darrin T. Mish, P.A. has spent three decades resolving exactly these situations for taxpayers nationwide, and we offer free initial consultations to walk through your specific case. Let's talk: Law Offices of Darrin T. Mish, P.A.