I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Owing money to the IRS can feel overwhelming, especially when you're staring at notices demanding payment for back taxes. Maybe you fell behind during a tough financial year, or perhaps an unexpected audit revealed you owe more than anticipated. Whatever the reason, you're not alone. Millions of Americans struggle to pay IRS back taxes each year, and the good news is that you have more options than you might think. The IRS actually wants to work with you (yes, really), because getting some payment is better than getting nothing. But navigating the system requires understanding your rights, knowing which payment strategies make sense for your situation, and acting before the IRS takes aggressive collection action.

Understanding What Back Taxes Really Mean

When we talk about back taxes, we're referring to any tax debt from previous years that remains unpaid. This could be from one tax year or several. The moment you miss the April tax deadline without filing an extension or paying what you owe, the IRS starts adding penalties and interest to your balance.

Here's what makes back taxes different from current-year tax debt:

- Penalties compound quickly (failure-to-file and failure-to-pay penalties can add up to 25% of your debt)

- Interest accrues daily based on the federal short-term rate plus 3%

- The IRS has broader collection powers after a certain period

- Your options for resolution may change depending on how old the debt is

The IRS typically has 10 years from the date of assessment to collect tax debt, known as the Collection Statute Expiration Date. Understanding this timeline matters because it affects which strategies make the most sense for your situation.

How Interest and Penalties Pile Up

Let's say you owe $10,000 in back taxes from 2024. If you don't address this debt, here's approximately what happens:

| Time Period | Original Debt | Penalties | Interest | Total Owed |

|---|---|---|---|---|

| Initial | $10,000 | $0 | $0 | $10,000 |

| 6 months | $10,000 | $500 | $300 | $10,800 |

| 1 year | $10,000 | $1,000 | $650 | $11,650 |

| 2 years | $10,000 | $2,500 | $1,400 | $13,900 |

These numbers demonstrate why addressing back taxes sooner rather than later makes financial sense. The longer you wait, the more you'll ultimately pay.

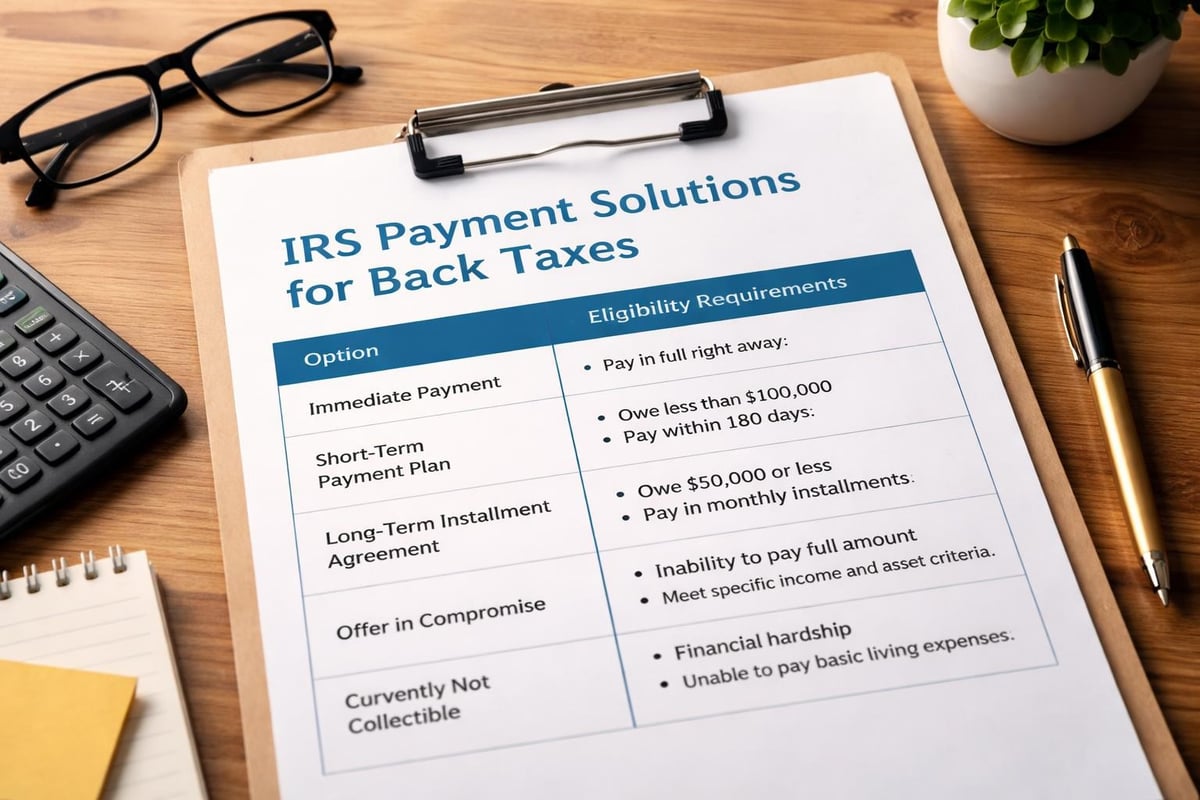

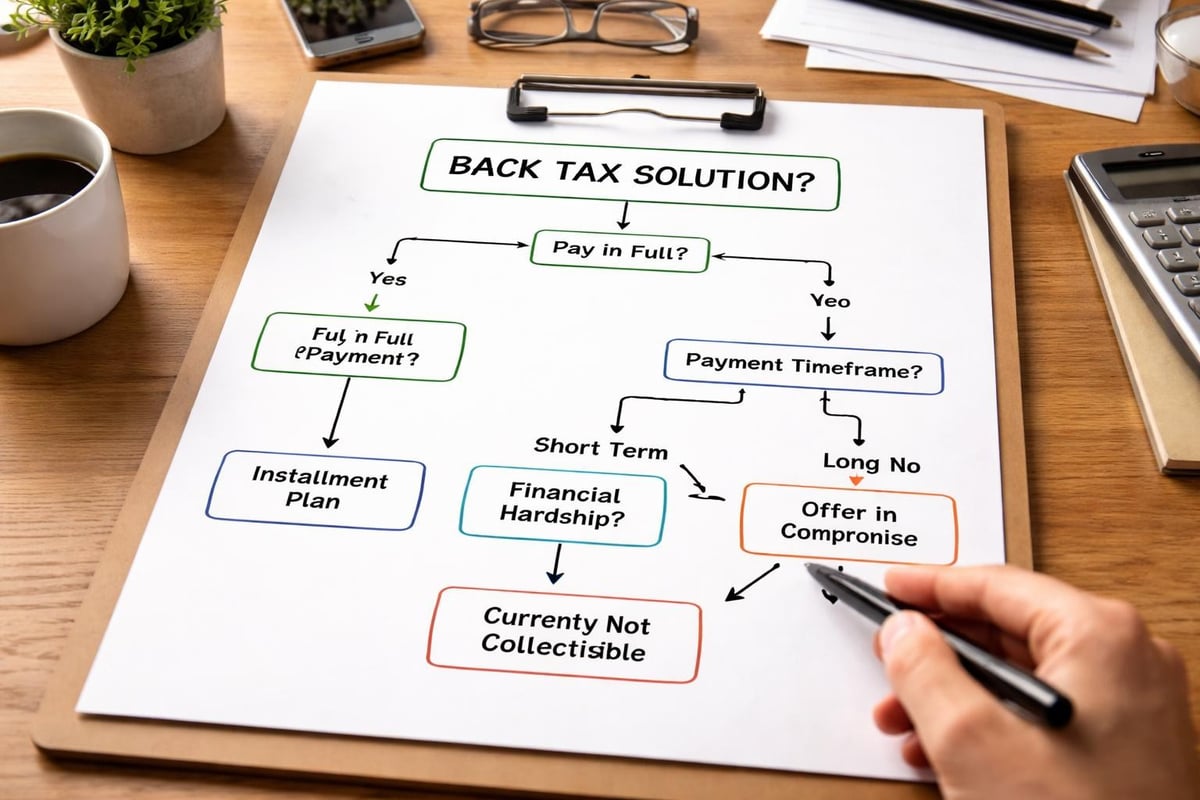

Payment Options When You Owe Back Taxes

The IRS offers several legitimate ways to pay IRS back taxes, and choosing the right one depends on your financial situation. Let's break down each option so you can see which might work for you.

Pay in Full Immediately

If you have the resources, paying your entire tax debt at once is the simplest solution. You'll stop interest from accruing and avoid any collection actions. The IRS accepts various payment methods, including:

- Direct bank transfer (Direct Pay)

- Credit or debit card (with processing fees)

- Check or money order

- Wire transfer

- Same-day payment by phone

The reality check: Most people facing back tax debt don't have thousands of dollars sitting around. That's okay. The other options exist specifically for taxpayers who need more flexibility.

Short-Term Payment Plans

If you can pay your full balance within 180 days, the IRS offers a short-term payment plan. This option works well if you're expecting money soon (like a tax refund from another year, a bonus, or proceeds from selling an asset).

Benefits of short-term plans:

- Minimal setup fees

- Less paperwork than long-term agreements

- Stops immediate collection actions

- Keeps interest and penalties lower than long-term plans

You can apply online through the IRS website if you owe less than $100,000 in combined tax, penalties, and interest. The application process typically takes less than 30 minutes.

Long-Term Installment Agreements

When you need more than six months to pay IRS back taxes, an installment agreement lets you make monthly payments over several years. Think of it like a payment plan for any other debt, except you're paying the federal government.

There are different types of installment agreements:

Streamlined Installment Agreement: For taxpayers owing $50,000 or less (combined tax, penalties, and interest). You can set this up online without providing detailed financial information.

Partial Payment Installment Agreement: For those who genuinely cannot pay the full amount before the collection statute expires. Requires detailed financial disclosure.

Non-Streamlined Installment Agreement: For debts exceeding $50,000. Requires Form 433-A or 433-F and potentially working with a revenue officer.

| Agreement Type | Debt Limit | Financial Info Required | Setup Fee | Monthly Payment |

|---|---|---|---|---|

| Streamlined | Up to $50,000 | Minimal | $31-$130 | Your calculation |

| Partial Payment | No limit | Extensive | $89-$225 | Based on ability to pay |

| Non-Streamlined | Over $50,000 | Extensive | $89-$225 | Negotiated |

The IRS generally wants you to pay off your debt within 72 months, but exceptions exist. Understanding these tax debt solutions helps you negotiate the best possible terms.

Offer in Compromise

An Offer in Compromise (OIC) lets you settle your tax debt for less than you owe. You've probably seen late-night commercials claiming "settle your IRS debt for pennies on the dollar!" While that marketing is exaggerated, an OIC can legitimately reduce your debt if you qualify.

The catch: The IRS only accepts about 40% of OIC applications. They'll approve your offer only if:

- You can't pay the full amount before the collection statute expires

- You have no realistic way to increase your income or liquidate assets

- There's doubt about whether you actually owe the tax (rare)

- Collecting would create economic hardship or be unfair

The application process requires extensive documentation about your income, expenses, assets, and future earning potential. You'll also need to stay current on all tax filings and estimated payments for at least five years after acceptance.

Want to explore whether you might qualify? The offer in compromise program requires careful evaluation of your unique financial circumstances.

What Happens If You Don't Pay IRS Back Taxes

Ignoring back tax debt doesn't make it disappear. The IRS has substantial collection powers that most creditors don't possess. Understanding the collection process as outlined by the IRS helps you know what to expect.

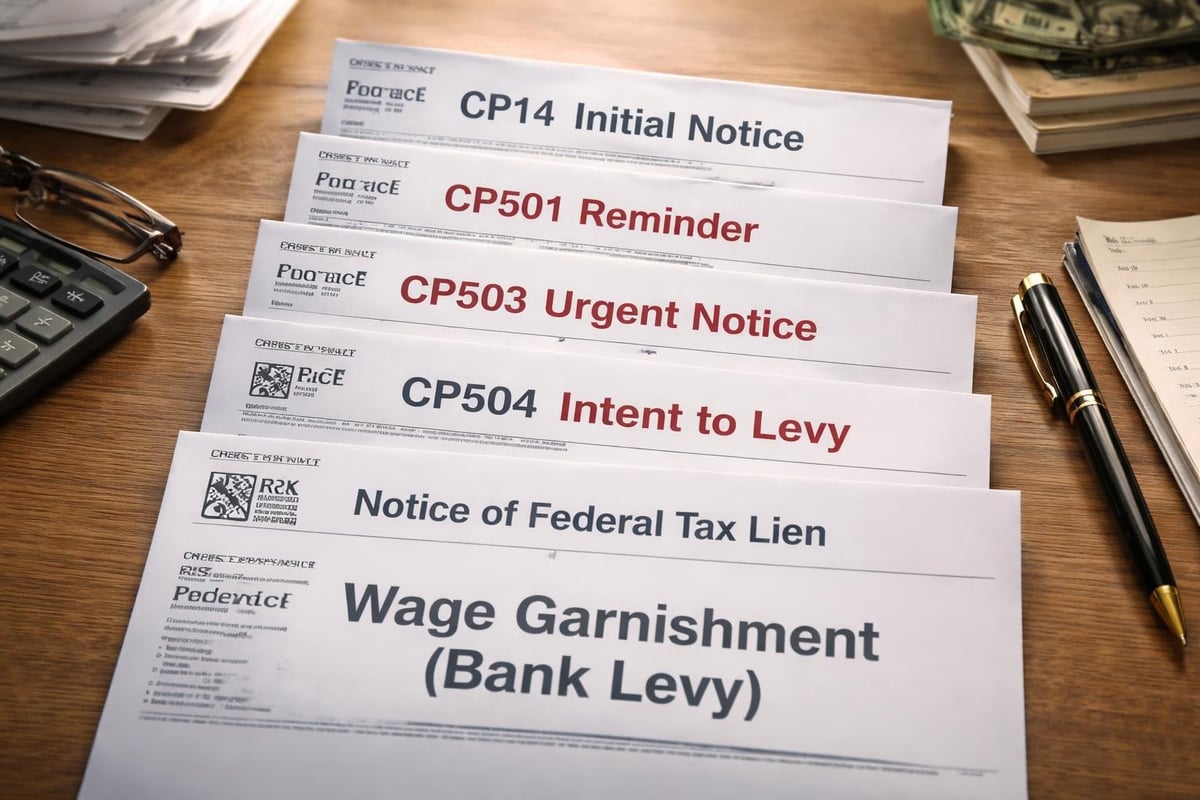

The Collection Notice Progression

The IRS follows a predictable pattern of increasingly urgent notices:

CP14 Notice: Your first notice stating you owe money. You have about 21 days to respond.

CP501: A reminder sent if you haven't responded. Still relatively gentle.

CP503: An urgent reminder. The tone shifts here.

CP504: Notice of intent to levy. This is serious. The IRS is warning they'll seize assets.

Final Notice of Intent to Levy: Your last warning before aggressive collection begins. You have 30 days to appeal.

Between these notices, you might receive phone calls from IRS collection agents. Remember: the IRS will never threaten you with immediate arrest or demand payment via gift cards. Those are scams.

Tax Liens and Levies

When you don't pay IRS back taxes, the government can file a Notice of Federal Tax Lien. This public document tells creditors that the IRS has a legal claim to your property. Tax liens damage your credit score and make it difficult to sell property or get loans.

A levy goes further by actually seizing your property:

- Bank levies freeze and withdraw funds from your accounts

- Wage garnishments take a portion of each paycheck

- Property seizures can take vehicles, real estate, or other assets

The IRS levy programs have some limitations. They generally can't take certain property like necessary work tools (up to certain values) or a portion of your wages needed for basic living expenses. But these protections are limited.

If you're facing wage garnishment, understanding how to protect your income becomes critical, especially if you rely on Social Security or other protected income sources.

Strategic Approaches to Paying Back Taxes

Successfully resolving back tax debt requires strategy, not just picking a payment option at random. Here's how to think through your situation systematically.

Assess Your Complete Financial Picture

Before contacting the IRS, know these numbers:

- Your total tax debt (including all years)

- Current monthly income after taxes

- Essential monthly expenses (housing, food, transportation, medical)

- Assets you own and their current values

- Other debts you're managing

This financial snapshot determines which payment options you'll realistically qualify for and which make sense for your situation.

Prioritize Getting Compliant

If you have unfiled tax returns, file them immediately. The IRS won't approve payment plans or settlement offers if you're not current with filings. Even if you can't pay, filing stops the failure-to-file penalty (which is 5% per month, up to 25%) and shows good faith.

You might discover that filing old returns actually reduces what you owe. Maybe you had deductions or credits you didn't know about. Or perhaps the IRS made an error in their substitute return filed on your behalf.

Consider Penalty Abatement First

Before arranging to pay IRS back taxes, explore whether you qualify for penalty abatement. The IRS may remove or reduce penalties if you have:

- First-time penalty abatement: Available if you've been compliant for the previous three years

- Reasonable cause: Events beyond your control (serious illness, natural disaster, etc.)

- Statutory exception: The IRS gave you bad advice

Penalty abatement doesn't eliminate interest or the tax itself, but removing penalties can significantly reduce your total debt. Penalty abatement strategies are often overlooked but can save thousands of dollars.

Explore Currently Not Collectible Status

If you genuinely cannot afford any payment right now, you might qualify for Currently Not Collectible (CNC) status. This temporarily halts IRS collection activities.

When CNC makes sense:

- Your necessary monthly expenses exceed your income

- Liquidating assets would leave you unable to meet basic needs

- You're unemployed or facing severe financial hardship

The IRS will still add interest to your debt during CNC status, and they'll periodically review your finances. But this option gives you breathing room to stabilize your situation without facing levies or garnishments. Learn more about currently not collectible status and how it works in practice.

Working With Tax Professionals

Should you handle back taxes on your own or hire help? The answer depends on your situation's complexity and the amount you owe.

When Professional Help Makes Sense

Consider working with a tax attorney or enrolled agent if:

- You owe more than $10,000

- You're facing a levy or lien

- You've received criminal investigation notices

- You need an Offer in Compromise

- The IRS rejected your initial payment plan request

- You're dealing with payroll tax issues

Tax attorneys provide legal protection that other professionals can't offer. Conversations with your attorney are protected by attorney-client privilege, and they can represent you in Tax Court if needed. With over three decades of experience, professionals who specialize in IRS tax debt relief understand how to navigate complex cases.

DIY Approach for Simpler Cases

You can probably handle it yourself if:

- You owe less than $10,000

- Your financial situation is straightforward

- You're setting up a basic installment agreement

- You have time to research and follow through

The IRS website provides tools and forms for most common situations. Their automated phone system can also handle straightforward payment arrangements.

The middle ground: Many taxpayers benefit from an initial consultation with a professional to understand their options, then handle the actual setup themselves. This gives you expert guidance without the ongoing costs.

Protecting Your Rights as a Taxpayer

You have rights when dealing with the IRS, and knowing them helps you avoid being taken advantage of (whether by the IRS itself or by scammers claiming to help).

The Taxpayer Bill of Rights includes ten fundamental rights:

- Right to be informed

- Right to quality service

- Right to pay no more than the correct amount of tax

- Right to challenge the IRS's position

- Right to appeal IRS decisions

- Right to finality

- Right to privacy

- Right to confidentiality

- Right to representation

- Right to a fair and just tax system

These aren't just nice words. They have practical applications when you pay IRS back taxes. For instance, you have the right to appeal any collection action before it takes effect. If the IRS files a lien, you can request a Collection Due Process hearing to challenge it.

If you believe the IRS has violated your rights, you can contact the Taxpayer Advocate Service, an independent organization within the IRS that helps taxpayers resolve problems. Understanding what to do if the IRS breaks the rules empowers you to stand up for yourself.

Common Mistakes to Avoid

Even well-intentioned taxpayers make errors when trying to resolve back taxes. Here are pitfalls to avoid:

Ignoring IRS notices: Each notice has deadlines. Missing them limits your options and moves you closer to enforced collection.

Withdrawing from retirement accounts prematurely: Yes, you could tap your 401(k) to pay back taxes, but you'll owe penalties and taxes on that withdrawal, often making your situation worse.

Falling for tax relief scams: Companies promising to "stop the IRS immediately" or "settle for pennies on the dollar with our secret method" are usually selling overpriced services you don't need. Legitimate tax relief options don't require secret methods.

Setting up payment plans you can't afford: An installment agreement you default on is worse than not having one. The IRS can immediately levy your assets after a default.

Not filing current returns while resolving old debt: Stay current going forward. Accumulating new debt while paying old debt puts you on a treadmill to nowhere.

Forgetting about state taxes: If you owe the IRS, you probably owe your state too. Most states have their own payment plans and collection powers.

Taking Action Today

The worst thing you can do with back tax debt is nothing. Every day you delay, interest accrues and your options may narrow. But taking that first step feels daunting. Where do you even begin?

Start with these immediate actions:

Step 1: Gather all IRS notices and correspondence. Organize them by tax year. Make sure you know exactly what you owe for each year.

Step 2: Request your tax transcripts from the IRS. These official records show what the IRS has on file for you. You can get them free online or by mail.

Step 3: Calculate your monthly disposable income (what's left after necessary expenses). This number determines which payment options you'll qualify for.

Step 4: Decide whether to handle this yourself or seek professional help. If you're unsure, schedule a consultation with a tax attorney for guidance.

Step 5: Contact the IRS or file the appropriate forms to set up your chosen payment arrangement. Don't wait for perfect timing. There is no perfect timing.

Remember, the IRS isn't evil. They're a bureaucracy following rules. When you work within their system proactively, they're surprisingly willing to work with you. When you ignore them, they have no choice but to follow their collection procedures.

If you're dealing with delinquent taxes from previous years, the sooner you address them, the more options remain available to you.

Dealing with back taxes doesn't have to be a nightmare if you understand your options and take action before the IRS forces your hand. Whether you need a simple installment agreement or a complex offer in compromise, the key is making an informed decision based on your unique financial situation. The Law Offices of Darrin T. Mish, P.A. has spent over 32 years helping taxpayers across the globe resolve their IRS problems, from wage garnishments to tax liens and everything in between. If you're feeling overwhelmed by tax debt and need personalized legal guidance, reach out for a free consultation with Law Offices of Darrin T. Mish, P.A. to explore your best path forward.