I hear from people every week who think their tax problem is the end of the world. It usually isn't. I'm Darrin Mish. I've resolved over $100 million in tax debt for clients. Here's what you should know.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

Most people think bankruptcy solves everything. File, get the discharge, walk away clean. That's true for credit cards, medical bills, even some business debts. But tax debt doesn't play by those rules. The IRS gets special treatment in bankruptcy court, and most tax liabilities survive the process entirely. You can file Chapter 7 and still owe the IRS every dollar you owed before, plus interest that kept running during your case.

That's where a bankruptcy and tax attorney becomes essential. You're not dealing with one problem; you're dealing with two legal systems that interact in unpredictable ways. Timing matters. The age of the debt matters. Whether you filed returns matters. The bankruptcy and tax attorney who understands both systems can tell you which debts disappear, which ones stick around, and how to structure the filing so you're not worse off than when you started.

When Bankruptcy Actually Discharges Tax Debt

The IRS doesn't forgive easily, but bankruptcy can eliminate certain tax debts if you meet specific requirements. These aren't guidelines. They're rigid statutory tests.

First, the tax debt must be income tax. Payroll taxes, trust fund penalties, and fraud penalties never discharge in bankruptcy. Never. The bankruptcy and tax attorney who promises to wipe out 941 liabilities through Chapter 7 is either confused or lying.

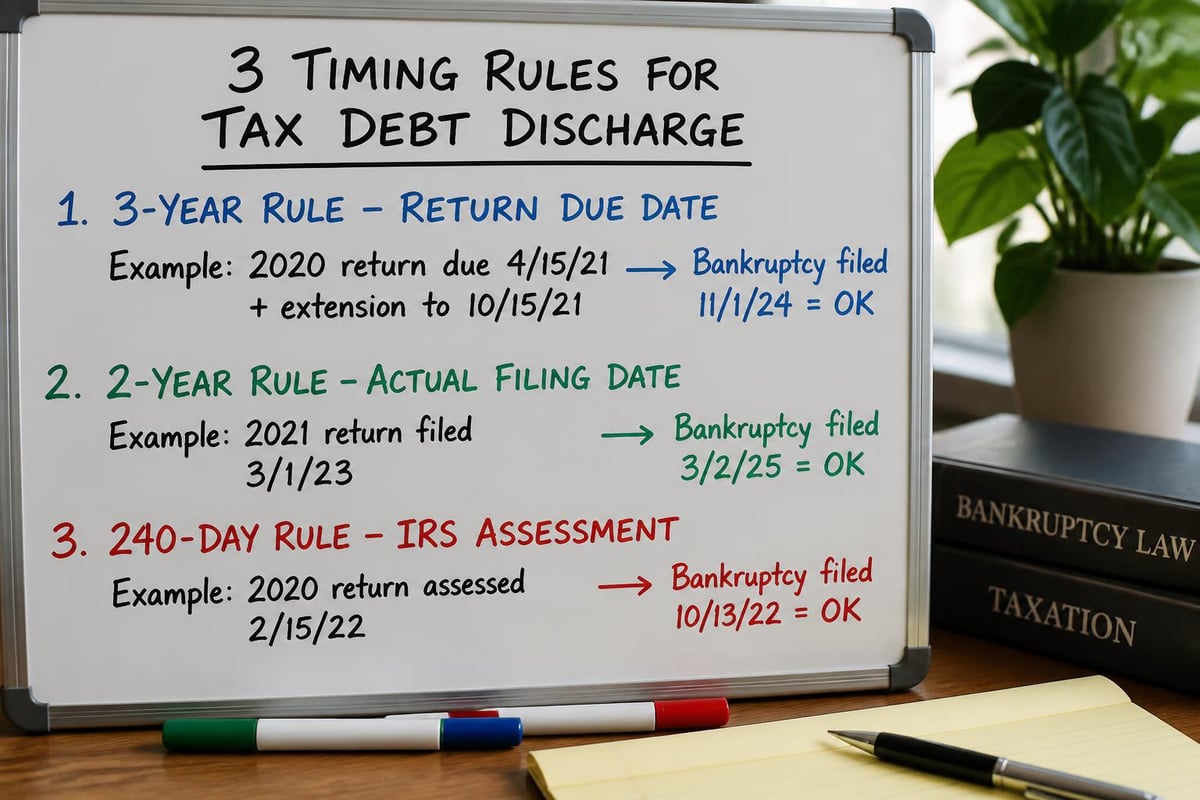

The Three-Year Rule

The tax return for the debt must have been due at least three years before you filed bankruptcy. If you're filing in 2026, we're looking at returns due in April 2023 or earlier. Extensions count. If you extended your 2022 return to October 2023, you can't discharge that debt until October 2026 at the earliest.

Most people miss this. They file bankruptcy too early, thinking any old debt qualifies. It doesn't.

The Two-Year Rule

You must have filed the return at least two years before the bankruptcy filing. This one catches people who didn't file on time. If the IRS filed a substitute return for you, that doesn't count. You had to file the actual return yourself, and it needs two full years of aging before bankruptcy does anything.

- Tax return due date: Starts the three-year clock

- Actual filing date: Starts the two-year clock

- Assessment date: Starts the 240-day clock (below)

- IRS collection activity: Can pause or restart timelines

The 240-Day Rule

The IRS must have assessed the tax at least 240 days before your bankruptcy filing. Assessment happens when the IRS processes your return or creates a substitute assessment. If you challenged the assessment through an audit or offer in compromise, that 240-day period pauses and can extend for years.

I've seen bankruptcies filed one month too early. The debtor walked away still owing $40,000 that would have been discharged if they'd waited thirty more days. That's why a bankruptcy and tax attorney reviews the assessment dates and filing dates before touching the paperwork.

Chapter 7 vs. Chapter 13 for Tax Debt

Chapter 7 discharges qualifying tax debt immediately. You file, wait a few months, get your discharge. If the tax debt meets the three tests above, it's gone. If it doesn't meet those tests, you still owe it all.

Chapter 13 works differently. You propose a payment plan spanning three to five years. Tax debt gets priority treatment, meaning you have to pay it in full through the plan. But here's the advantage: the IRS can’t collect while you’re in Chapter 13. No levies, no liens, no wage garnishments. You make your plan payment, and the IRS waits.

Chapter 7 advantages:

- Fast discharge (90-120 days typically)

- Eliminates qualifying debt permanently

- No payment plan required

- Lower attorney fees

Chapter 13 advantages:

- Stops all IRS collection activity immediately

- Pays priority tax debt over 3-5 years interest-free in many cases

- Can discharge some tax debt at the end if it becomes old enough

- Protects co-signers and wage garnishment victims

The bankruptcy and tax attorney's job is mapping your specific debts against these two frameworks. Some debts qualify for Chapter 7 discharge now. Others need to age another year. Some are payroll taxes that won't discharge ever. You might file Chapter 13 today to stop a levy, then convert to Chapter 7 in eighteen months when the older debts finally qualify for discharge.

Tax Liens Survive Bankruptcy

Here's the part that surprises everyone. Even if bankruptcy discharges your personal liability for the tax debt, any tax lien the IRS filed before bankruptcy stays attached to your property.

The discharge eliminates what you personally owe. The lien stays on the house, the car, the bank account. If you sell the property, the IRS gets paid from the proceeds. If you refinance, the lien blocks the new loan until you deal with it.

| Scenario | Personal Liability | Property Lien |

|---|---|---|

| Discharged tax debt, no lien filed | Eliminated | None |

| Discharged tax debt, lien filed before bankruptcy | Eliminated | Survives bankruptcy |

| Non-dischargeable tax debt, lien filed | Still owed in full | Survives bankruptcy |

| Non-dischargeable tax debt, no lien | Still owed in full | IRS can file lien after bankruptcy |

The only way to remove a tax lien through bankruptcy is to pay the underlying debt in full through a Chapter 13 plan. Then the lien releases. Otherwise, it sits there until the collection statute expires, which can be ten years or longer depending on various tolling events.

A bankruptcy and tax attorney looks at the lien filing date before recommending any bankruptcy strategy. If the IRS hasn't filed the lien yet, timing the bankruptcy correctly can prevent the lien from ever attaching. File too late, and you're stuck with lien removal negotiations after the bankruptcy closes.

Payroll Taxes Don't Discharge

Business owners face a specific problem. When you don't pay over employee withholding to the IRS, that creates a trust fund penalty under 26 U.S.C. § 6672. The IRS can assess this penalty against anyone responsible for paying the company's payroll taxes.

Bankruptcy never discharges trust fund penalties. Ever. These are debts you held in trust for someone else (your employees) and failed to pay over. Congress carved out an explicit exception in 11 U.S.C. § 523(a)(1)(B).

I've seen business owners file Chapter 7 thinking it'll clear out $200,000 in 941 liabilities. It doesn't. They get the discharge, and the IRS starts collecting again the next month. A bankruptcy and tax attorney with tax experience spots this before filing and redirects to better options: installment agreements, partial payment plans, or offers in compromise.

The same rule applies to sales taxes, excise taxes, and any other tax you collected from someone else. If you were acting as a collection agent for the government, bankruptcy won't eliminate the liability.

The Automatic Stay and IRS Collection

When you file bankruptcy, the automatic stay under 11 U.S.C. § 362 stops most creditors cold. They can't call, can't sue, can't collect. The IRS has to stop too, but with exceptions.

The IRS can continue a tax audit during bankruptcy. They can issue a notice of deficiency. They can assess tax. What they can't do is actually levy or seize property while the stay is in effect. If they already filed a lien before bankruptcy, that lien stays in place, but they can't enforce it until the case closes.

IRS actions allowed during bankruptcy:

- Conducting audits

- Issuing notices of deficiency

- Assessing additional tax

- Demanding tax returns

IRS actions prohibited during bankruptcy:

- Levying bank accounts

- Garnishing wages

- Seizing property

- Filing new liens (in most circuits)

The stay lasts as long as your bankruptcy case is open. In Chapter 7, that's about four months. In Chapter 13, that's three to five years. During that time, you get breathing room. But the IRS doesn't forget. They note the bankruptcy, pause collection, and resume the moment the case closes unless the debt was actually discharged.

This is where understanding who qualifies for IRS forgiveness programs matters. Some debts that survive bankruptcy can still be resolved through offers in compromise or currently not collectible status after the bankruptcy ends.

Timing Bankruptcy With IRS Payment Plans

Some people are already in an installment agreement when financial trouble hits. Maybe the payment was manageable at $800 per month, but now you lost your job and can't make it. Bankruptcy might make sense, but it terminates your existing payment plan.

If you file Chapter 7 and discharge part of the debt, you can request a new installment agreement for whatever survives. The IRS treats the remaining balance as a fresh case. Your old payment history doesn't matter.

If you file Chapter 13, the bankruptcy plan replaces the installment agreement entirely. You make your plan payment to the trustee, who distributes to creditors including the IRS. At the end of the plan, if you've paid the priority tax debt in full, you're done.

A bankruptcy and tax attorney coordinates this timing. Sometimes it makes sense to default on the IRS agreement, let them start enforced collection, then file bankruptcy to stop the levy. Other times, staying in the agreement and negotiating a lower payment works better than involving the bankruptcy court.

Post-Bankruptcy Tax Planning

Bankruptcy doesn't fix bad tax habits. If you didn't withhold enough in 2023, 2024, and 2025, filing bankruptcy in 2026 doesn't prevent new tax debt from piling up after your discharge. I've seen people file Chapter 7, get their discharge, then owe $30,000 in new taxes two years later because they didn't adjust their withholding or quarterly payments.

The bankruptcy and tax attorney who only handles the filing without addressing ongoing tax compliance is doing half the job. You need withholding adjustments, estimated payment schedules, and a plan to avoid creating new debt while you're recovering from the old debt.

Steps After Bankruptcy Discharge

- Request IRS account transcripts to confirm which debts were discharged

- Verify lien releases for any tax debts paid through Chapter 13

- Adjust W-4 withholding to prevent future underpayment

- Set up quarterly estimated payments if self-employed

- File all current-year returns on time with full payment

The IRS doesn't automatically update your account after bankruptcy. You have to monitor it. Sometimes they keep sending notices for discharged debt because their system didn't process the discharge properly. A bankruptcy and tax attorney sends the discharge order to the IRS and follows up until the account reflects the correct balance.

When to Avoid Bankruptcy Entirely

Bankruptcy isn't always the answer. If your only debt is taxes, and those taxes are relatively recent, bankruptcy won't help. You'll pay filing fees, attorney fees, and still owe the IRS everything.

Better options in that scenario:

- Installment agreement: Pay over time, usually 72 months or less

- Offer in compromise: Settle for less than owed if you qualify

- Currently not collectible: Pause collection until finances improve

- Penalty abatement: Eliminate penalties, reduce total owed

I've told clients not to file bankruptcy at least a hundred times. When the numbers don't work, they don't work. Filing just to stop a levy when you could set up a $200/month payment plan wastes time and damages credit for no reason.

But when you have $80,000 in credit card debt, $40,000 in medical bills, and $25,000 in dischargeable tax debt, Chapter 7 makes sense. You clear everything in one filing. The bankruptcy and tax attorney runs the analysis: which debts are dischargeable, what's the total savings, and is the credit impact worth the debt relief.

Combining Bankruptcy With Offers in Compromise

Sometimes you file bankruptcy to discharge non-tax debt, then immediately file an offer in compromise for the tax debt that survived. This strategy works when bankruptcy clears enough monthly payment obligations to make an offer affordable.

Example: You owe $50,000 to credit cards, $60,000 in old income taxes, and $40,000 in recent payroll taxes. Chapter 7 discharges the credit cards and the old income taxes. The payroll taxes survive. After bankruptcy, your monthly expenses drop by $1,200 because the credit card payments are gone. Now you can afford a $500/month offer payment for the payroll taxes.

The IRS evaluates offers based on reasonable collection potential, which includes your monthly disposable income. Bankruptcy changes that calculation by eliminating other debts. A bankruptcy and tax attorney sequences these filings to maximize the benefit.

Working With Both Bankruptcy and Tax Counsel

Some attorneys handle both bankruptcy and tax. Most don't. The attorney who files hundreds of Chapter 7 cases per year probably doesn't spend time negotiating offers in compromise or challenging trust fund penalties. The tax attorney who works IRS cases daily might not know bankruptcy timing rules or lien survival exceptions.

You need someone who genuinely practices in both areas, or you need coordinated counsel: a bankruptcy attorney and a tax attorney working together on your case. They should be communicating about timing, discharge analysis, and post-bankruptcy tax resolution before any filing happens.

Questions to ask:

- How many bankruptcy cases involving significant tax debt have you handled?

- What percentage of your practice is IRS representation versus bankruptcy?

- Can you analyze my IRS transcripts to determine discharge eligibility?

- Will you handle post-bankruptcy tax resolution, or refer that out?

The wrong bankruptcy filing at the wrong time can make tax problems worse. The IRS gets priority in bankruptcy, so if you file Chapter 13 and can't make the plan payments, you've just wasted two years and the tax debt is still there. A bankruptcy and tax attorney prevents that outcome by stress-testing the plan before filing.

Bankruptcy can eliminate some tax debt, but most tax problems need direct IRS negotiation rather than bankruptcy court intervention. The Law Offices of Darrin T. Mish, P.A. handles both: analyzing whether bankruptcy helps your tax situation and representing you in IRS collections regardless of which path makes sense. If you're dealing with tax debt, wage garnishments, or liens and considering bankruptcy, get the analysis done right the first time. Law Offices of Darrin T. Mish, P.A. offers free consultations to review your specific situation and map out the best resolution strategy.