If you've got an IRS letter on your desk right now, you have a decision to make, and the clock matters. I'm Darrin Mish. I've spent 32 years helping people with exactly this kind of situation. Here's what you should do.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

You didn't file returns for three years, or you filed and couldn't pay, or you've been ignoring notices because you didn't know what else to do. Now you're wondering whether you need a tax attorney for back taxes or if you can fix this yourself.

Here's what matters: the IRS has already decided how this ends if you don't act. They'll file liens against your property, levy your bank account, or garnish your wages. A tax attorney for back taxes doesn't prevent consequences – they give you better options than the IRS's default collection process.

Most people wait too long. They think the problem will resolve itself, or they're paralyzed by fear. By the time they call, the IRS has already started enforcement. That makes everything harder and more expensive.

What a Tax Attorney for Back Taxes Actually Does

A tax attorney doesn't make your debt disappear with magic legal arguments. They negotiate the most favorable resolution based on your financial reality and prevent the IRS from taking enforcement action while you're working toward a solution.

The real value is knowing which resolution option works for your specific situation. The IRS offers installment agreements, offers in compromise, penalty abatement, currently not collectible status, and innocent spouse relief. Each has strict eligibility requirements. Most taxpayers pick the wrong one because they don't understand the criteria.

Reading IRS Notices Correctly

When you receive a CP14 notice about unpaid taxes, you have options. Most people throw it in a drawer. That's the worst response.

Each notice type signals where you are in the collection timeline. CP501 and CP503 are early reminders. The CP504 notice is your final notice before levy action. Once you receive a CP90 or CP91 notice, the IRS is about to levy your assets or Social Security benefits.

A tax attorney for back taxes knows which notices require immediate action and which buy you time. The difference is whether you negotiate from a position of control or panic.

What the IRS Can Actually Take

The IRS has broader collection powers than any creditor. They don't need a court order to levy your bank account. They can garnish up to 70% of your wages. They can seize and sell your house, car, or business assets.

But they rarely do. Bank levies and wage garnishments are standard. Asset seizures are uncommon because they're administratively expensive and politically sensitive. The IRS would rather you pay voluntarily through an installment agreement.

This creates negotiating leverage if you know how to use it. A tax attorney structures payment plans that work within your budget while satisfying IRS collection standards. The IRS won't accept any payment amount you propose – they have formulas based on your income, expenses, and assets.

Installment Agreements vs. Offers in Compromise

These are the two most common resolutions, and most taxpayers confuse them. An installment agreement means you pay the full balance over time. An offer in compromise means the IRS accepts less than you owe.

Installment agreements work when you can afford monthly payments but can't pay the balance immediately. The IRS will approve almost any installment agreement if you owe less than $50,000 and can pay within 72 months. You can set it up online through the IRS payment options system.

For balances above $50,000, the IRS requires a Collection Information Statement (Form 433-F or 433-A). They calculate your disposable income using their allowable expense standards – not your actual expenses. This is where most taxpayers without representation get squeezed into payments they can't sustain.

When an Offer in Compromise Actually Works

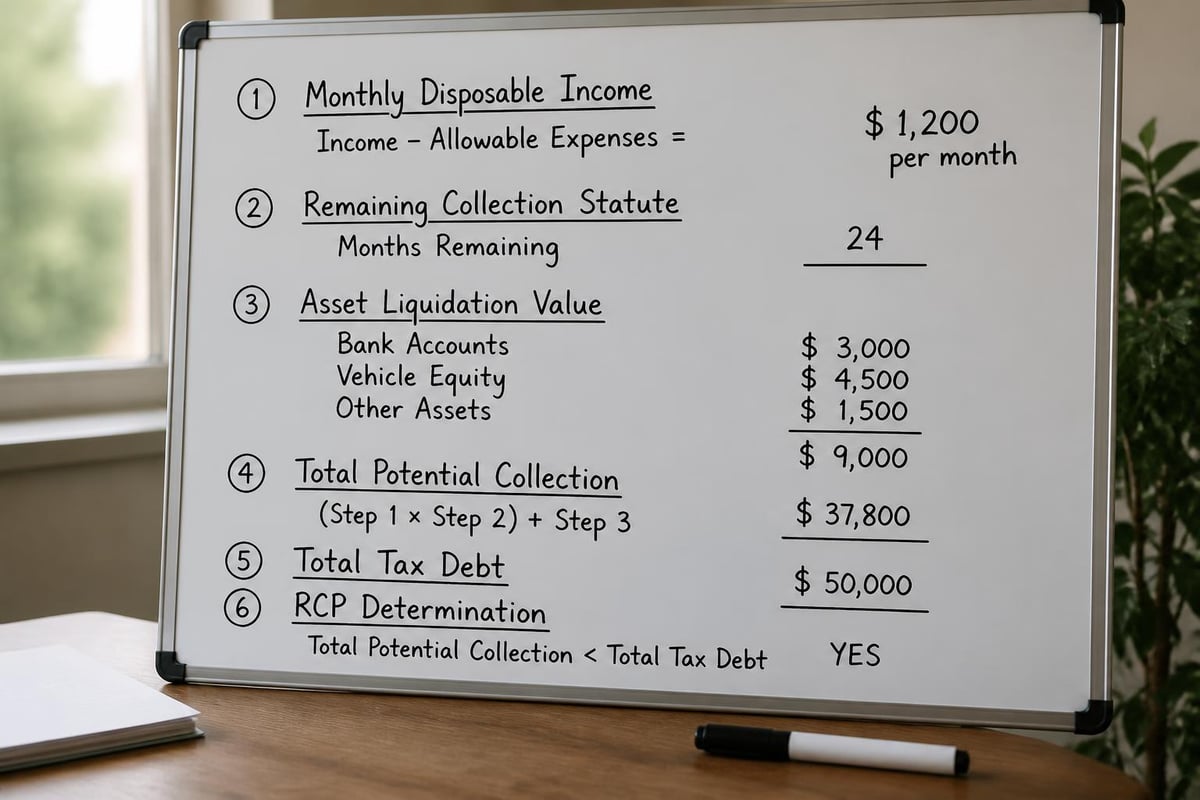

An offer in compromise only works if you genuinely can't pay the full balance within the collection statute expiration date (usually 10 years from assessment). The IRS calculates your reasonable collection potential based on your asset equity and future income.

The formula is: (Monthly disposable income × remaining months on statute) + liquidation value of assets. If this number is less than your tax debt, you might qualify. If it's more, you won't.

| Resolution Type | Best For | Typical Timeline | Success Rate |

|---|---|---|---|

| Installment Agreement | Stable income, manageable debt | 30-60 days | 85-90% |

| Offer in Compromise | Limited income/assets, high debt | 6-12 months | 25-40% |

| Currently Not Collectible | Temporary hardship | 30-90 days | 60-70% |

| Penalty Abatement | First-time penalty, reasonable cause | 30-60 days | 40-60% |

The IRS rejects most offer in compromise applications because taxpayers overestimate their eligibility. They see advertisements promising "settle your tax debt for pennies on the dollar" and assume they qualify. A tax attorney for back taxes runs the calculation before filing the application, saving you the $205 application fee and 12 months of waiting.

Currently Not Collectible Status

This is the most underused resolution option. If you can't afford an installment agreement and don't qualify for an offer in compromise, currently not collectible status temporarily halts collection activity.

The IRS places your account in status 53 hardship. They stop sending notices, won't levy your bank account, and won't garnish your wages. Your balance continues accruing interest and penalties, and the IRS can file a tax lien, but active collection stops.

You stay in this status until your financial situation improves or the collection statute expires. It's not a permanent solution, but it gives you breathing room when you're genuinely broke. Many people in currently not collectible status end up running out the statute expiration without paying the balance.

Penalty Abatement Strategies That Work

About 40% of what you owe might be penalties rather than tax. The IRS assesses failure-to-file penalties (25% of tax), failure-to-pay penalties (0.5% per month up to 25%), and accuracy-related penalties (20% of underpayment).

You can request penalty abatement based on reasonable cause or first-time abatement. Reasonable cause means circumstances beyond your control prevented compliance – serious illness, natural disaster, death in family, unavoidable absence. The IRS evaluates these case-by-case.

First-time abatement is automatic if you meet three criteria:

- No penalties in the prior three years

- Filed all required returns (or filed extensions)

- Paid or arranged to pay any tax due

The IRS doesn't advertise first-time abatement. Most taxpayers don't know it exists. You simply request it by calling or writing. It can eliminate thousands in penalties immediately, even if you still owe the underlying tax.

Penalty Abatement for Businesses

Business tax penalties are harsher. The failure-to-deposit penalty for payroll taxes can reach 15% if you're more than 10 days late. Trust fund recovery penalties make business owners personally liable for unpaid payroll taxes.

A tax attorney for back taxes can negotiate penalty abatement for businesses by demonstrating reasonable cause or showing the penalties were assessed incorrectly. The IRS is more aggressive with business taxes because payroll withholdings are trust fund taxes – money that belongs to employees and the government, not the business.

If you've been dealing with IRS wage garnishments because of unpaid payroll taxes, reasonable cause abatement might be your only path to reducing the total balance to something manageable.

Tax Liens and How They Actually Work

A federal tax lien is the IRS's legal claim against your property when you owe back taxes. The IRS files the lien in public records, which damages your credit and makes it difficult to sell or refinance assets.

The lien attaches to everything you own – real estate, vehicles, business assets, even property you acquire after the lien filing. It doesn't mean the IRS will seize these assets. It means they have priority over other creditors if you sell or if the assets are liquidated.

You can get a tax lien released three ways:

- Pay the balance in full

- Get the IRS to withdraw the lien (different from release)

- Wait for the lien to expire (10 years plus assessment delays)

Lien withdrawal is possible if you enter a direct debit installment agreement for balances under $25,000 or if the lien was filed in error. The withdrawal removes the public record, which helps your credit. But you still owe the tax.

Subordination and Discharge

If you need to refinance a property with a tax lien, you can request subordination. This allows another creditor to move ahead of the IRS in priority, making refinancing possible. The IRS approves subordination if it increases their likelihood of collecting the debt.

A discharge removes the lien from specific property, usually when you're selling it. The IRS gets paid from the proceeds, and the lien releases from that asset but remains on others.

Most taxpayers don't know these options exist. They assume a tax lien on their property means they can't sell or refinance. A tax attorney for back taxes structures the transaction to satisfy the IRS while allowing you to move forward.

Dealing With Unfiled Returns

You can't resolve back taxes until you file all required returns. The IRS won't process an installment agreement, offer in compromise, or any other resolution if you have unfiled returns.

If you haven't filed in several years, the IRS may have filed substitute returns for you. These are almost always wrong. They don't include deductions, credits, or exemptions you're entitled to. You end up owing more than you should.

Filing delinquent returns often reduces your balance significantly. The IRS has three years from the filing date to audit a return, but there's no statute of limitations if you don't file. By filing, you start the clock and potentially reduce your liability.

How Far Back You Need to File

The IRS typically requires six years of unfiled returns before they'll negotiate. If you're self-employed or have complex returns, you might need to file more. The goal is to establish compliance and calculate your actual liability.

A tax attorney for back taxes can often reconstruct returns from limited records – bank statements, third-party information reporting, prior returns. Most clients think they can't file because they don't have documentation. You can almost always reconstruct enough information to file accurate returns.

Wage Garnishments and Bank Levies

Once the IRS issues a levy, you have limited options. A wage garnishment continues until the balance is paid or you arrange an alternative resolution. A bank levy is one-time – they freeze your account and take whatever's there on the date the bank receives the levy.

You can release a levy by entering an installment agreement or demonstrating economic hardship. Hardship means the levy prevents you from meeting basic living expenses. The IRS will release the levy but your balance doesn't go away.

Most people call after the levy hits. That's too late to prevent it but not too late to stop future collection action. A tax attorney for back taxes can negotiate a levy release and installment agreement within days if you respond immediately.

Levy Appeals and Collection Due Process

You have appeal rights before and after a levy. When you receive a Final Notice of Intent to Levy, you have 30 days to request a Collection Due Process hearing. At the hearing, you can propose alternative collection methods and challenge the liability if you haven't had a prior opportunity.

If you miss the 30-day window, you can request an equivalent hearing. You get the same consideration but not the same appeal rights. Most taxpayers miss these deadlines because they don't understand the notice.

Understanding IRS relief options helps you respond appropriately when you receive collection notices instead of panicking or ignoring them.

When You Need Representation vs. When You Don't

If you owe less than $10,000, have straightforward W-2 income, and can afford monthly payments, you probably don't need a tax attorney for back taxes. Set up an installment agreement online through the IRS payment options portal.

You need representation if:

- You owe more than $50,000

- The IRS has filed liens or issued levies

- You can't afford the installment agreement the IRS calculated

- You're considering an offer in compromise

- You have unfiled returns spanning multiple years

- You're facing trust fund recovery penalties

- Your spouse created the tax debt and you weren't involved

The cost of representation is typically 5-15% of your total liability, depending on complexity. That sounds expensive until you compare it to the cost of choosing the wrong resolution or accepting the IRS's proposed payment plan when better options exist.

What to Look for in a Tax Attorney

Not every lawyer handles tax debt. You want someone who focuses on IRS representation, not someone who does general practice and occasionally handles tax cases.

Ask how many offer in compromise applications they've filed in the past year. Ask about their success rate with penalty abatement. Ask whether they have experience with business payroll tax debt if that's your situation.

Most importantly, ask about their fee structure. Some attorneys charge flat fees for specific services. Others charge hourly. Neither is inherently better, but you should understand what you're paying before you sign.

IRS Collection Statute Expiration

The IRS has 10 years from the date of assessment to collect tax debt. After that, the debt expires. This is the collection statute expiration date (CSED), and it's the single most important date in your case.

Certain actions suspend or extend the statute – filing bankruptcy, submitting an offer in compromise, living outside the U.S., filing a Collection Due Process appeal. These add time to the 10-year period.

If you're close to the CSED, your strategy changes completely. An installment agreement might not make sense. Currently not collectible status might be better, letting you run out the clock. A tax attorney for back taxes calculates your CSED and structures a resolution around it.

Assessment vs. Filing Date

The 10 years runs from assessment, not filing. For most returns, assessment happens when you file. If the IRS files a substitute return for you, assessment happens when they process it. If you amend a return or the IRS audits you, additional assessments reset the 10-year clock for those amounts.

Calculating the exact CSED requires pulling your IRS transcript and tracking every tolling event. Most taxpayers can't do this accurately. Getting it wrong means paying debt that's already expired or making strategic decisions based on wrong dates.

Innocent Spouse Relief

If your spouse or former spouse created tax debt without your knowledge, you might qualify for innocent spouse relief. This applies to joint returns where one spouse understated income or claimed improper deductions.

The IRS considers whether you knew or had reason to know about the understatement, whether you benefited from it, and whether it would be unfair to hold you liable. These are fact-intensive determinations.

There are three types of relief:

- Innocent spouse relief – You didn't know and had no reason to know about the error

- Separation of liability – You're divorced or separated and can show which portion of debt belongs to which spouse

- Equitable relief – You don't qualify for the first two but collecting from you would be unfair

Each type has different eligibility requirements and application deadlines. Most people file for all three simultaneously and let the IRS determine which applies.

Timing Matters for Innocent Spouse Claims

You must request innocent spouse relief within two years of the IRS's first collection action against you. Collection action means levy, lien filing, or offset of your refund.

If you miss the two-year deadline for innocent spouse relief or separation of liability, you can still request equitable relief. There's no deadline for equitable relief as long as collection action hasn't ended.

This is another area where representation matters. The IRS denies most innocent spouse claims filed by taxpayers without representation. An attorney knows which facts matter and how to present them.

State Tax Debt and Back Taxes

Most states have their own collection processes separate from the IRS. If you owe state back taxes, you're dealing with two separate agencies with different procedures and resolutions.

Some states follow IRS programs – they offer installment agreements and penalty abatement. Others have limited options. California, New York, and Florida handle tax debt very differently from each other and from the IRS.

A tax attorney for back taxes practicing in Tampa handles Florida cases regularly, but Florida doesn't have state income tax. If you moved from another state and have state tax debt, you need an attorney familiar with that state's procedures. Some states are more aggressive than the IRS. Others are easier to negotiate with.

Working with someone familiar with back taxes and the IRS process helps you understand how federal and state debt interact, especially if you have both.

Moving Forward When You're Overwhelmed

Most people calling about back taxes are paralyzed by anxiety. They've been avoiding the problem for months or years. They think they're the only person in this situation.

You're not. Millions of taxpayers owe back taxes. The IRS processes thousands of installment agreements, offers in compromise, and penalty abatements every week. Your situation isn't unique or unfixable.

The IRS wants to collect. They'll work with you if you respond and propose a reasonable resolution. What they won't do is go away or forget about the debt.

Start by pulling your IRS transcripts to understand exactly what you owe and when it was assessed. Request transcripts online through the IRS website or by calling. You need your account transcripts, which show all activity on your account.

Next, calculate your actual ability to pay based on the IRS's allowable expense standards, not your preferred budget. The IRS doesn't care about your cable bill or car payment beyond their standardized amounts.

Then decide which resolution makes sense – installment agreement, offer in compromise, currently not collectible status, or waiting out the statute. This is where representation changes outcomes. The wrong choice means paying more than necessary or choosing a resolution you can't maintain.

Back taxes don't resolve through hope or avoidance – they resolve through action and the right strategy. If you're dealing with IRS debt, unfiled returns, or collection notices, Law Offices of Darrin T. Mish, P.A. has spent 32 years resolving these exact problems for clients across the globe. Schedule a free consultation to review your options and build a plan that actually works.