After 32 years of IRS work — and more than $100 million in resolved tax debt — I've seen just about every version of the problem you're dealing with. I'm Darrin Mish, a tax attorney in Tampa. Here's what you should know.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

The CP91 and CP298 notices aren't threats. They're final warnings before the IRS takes 15% of your Social Security benefits every month until your tax debt is paid. Most people freeze when they see these letters, convinced they've run out of options. They haven't. But the clock is running, and your cp91 cp298 levy notice response needs to happen fast.

You get 30 days from the notice date. Not 30 days from when you opened the envelope. From the date printed on the letter.

What CP91 and CP298 Actually Mean

The CP91 notice and CP298 notice serve the same function with one difference. CP91 goes to taxpayers who filed a return and owe. CP298 targets people the IRS believes didn't file or whose return was prepared by the IRS through a substitute for return.

Both notices announce the IRS's intent to levy your Social Security retirement, survivor, or disability benefits. Not garnish your wages. Not seize your bank account. This is specifically about Social Security.

The levy takes 15% of each monthly payment. That continues indefinitely until the debt is satisfied, you set up a payment plan, or you successfully challenge the levy through a Collection Due Process hearing.

Here's what triggers these notices:

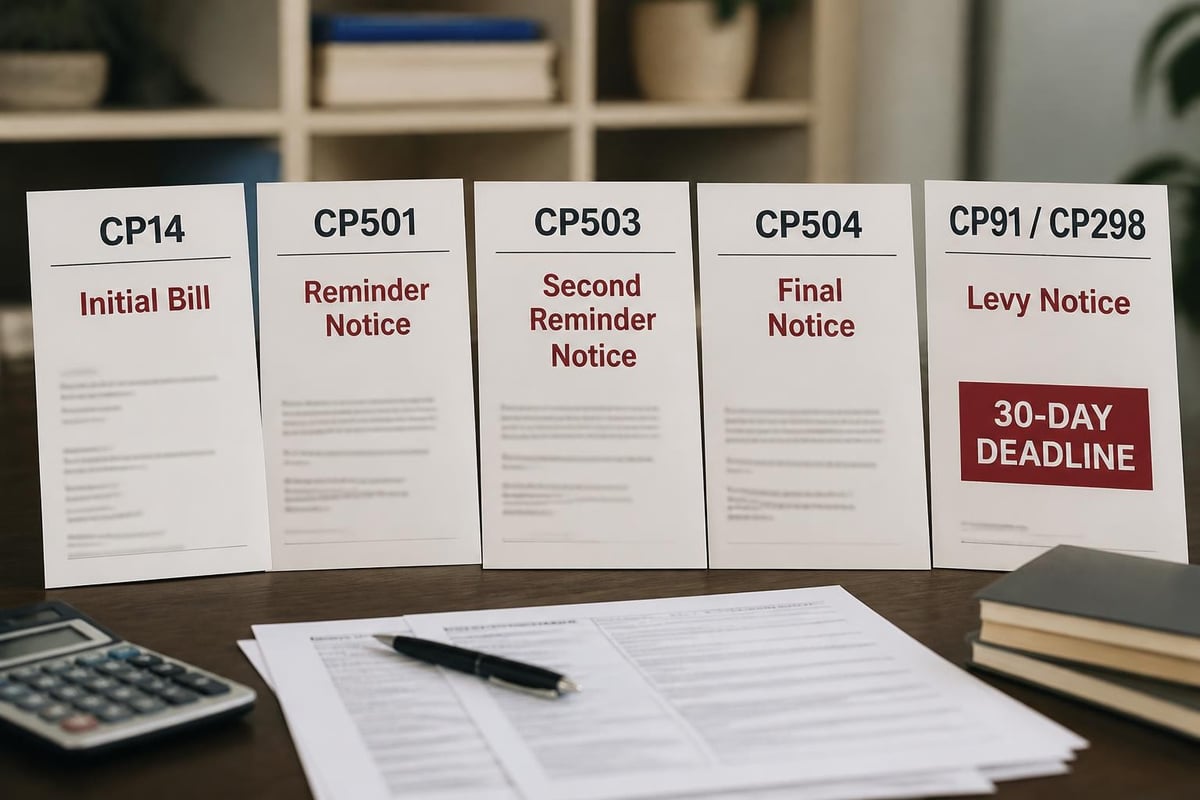

- You owe past-due federal taxes

- The IRS sent you multiple bills (CP14, CP501, CP503, CP504)

- You ignored them or the IRS rejected your payment arrangement

- The IRS filed a Notice of Federal Tax Lien or decided to skip straight to levy

The agency doesn't need a court order. Social Security Administration turns over the 15% on the IRS's instruction.

The 30-Day Window for Your CP91 CP298 Levy Notice Response

You have 30 days from the notice date to request a Collection Due Process (CDP) hearing. This is not negotiable. Miss it, and your only option is an equivalent hearing, which doesn't stop the levy.

A CDP hearing request stops the levy. The IRS cannot touch your Social Security benefits while the hearing is pending. That pause alone buys you months to work out a solution.

To request the hearing, you file Form 12153, Request for a Collection Due Process or Equivalent Hearing. The form asks why you disagree with the levy and what alternative you're proposing.

What You Can Challenge in the Hearing

| Challenge Type | What It Means | When It Works |

|---|---|---|

| Liability dispute | You don't actually owe the tax | You never received a statutory notice of deficiency or didn't have a chance to dispute the assessment |

| Collection alternative | You can pay through installment agreement or Offer in Compromise | You demonstrate financial hardship or propose a realistic payment plan |

| Lien or levy abuse | The IRS violated procedures | The levy creates immediate economic hardship beyond the norm |

| Spousal defenses | You qualify for innocent spouse relief | The debt arose from your spouse's actions and you didn't benefit |

Most hearings resolve through negotiated payment arrangements. The IRS Office of Appeals isn't looking to crush you. They want the debt paid in a way that doesn't require ongoing enforcement.

Your cp91 cp298 levy notice response should propose a concrete alternative. "I can't afford this" isn't enough. "I can pay $200 per month" backed by a completed Form 433-A or 433-F is a starting point.

Payment Alternatives That Stop the Levy

The IRS won't release a levy just because you asked nicely. You need to give them a reason grounded in the Internal Revenue Code or show them a path to getting paid.

Installment agreements are the most common resolution. You agree to monthly payments that fully pay the debt before the collection statute expires. The IRS typically has 10 years from the date of assessment to collect. If you can pay the balance in that window, even at $50 per month, that's usually acceptable if your financial statement supports it.

Streamlined installment agreements are available for balances under $50,000. You don't need to submit financial documentation. Just set up direct debit and the IRS approves it administratively.

- Balances under $10,000: 72 months to pay

- Balances $10,000-$25,000: 72 months with direct debit

- Balances $25,000-$50,000: 72 months with full financial disclosure

For balances over $50,000, you'll need to complete Form 433-F (individuals) or 433-B (businesses) and substantiate your income and expenses. The IRS calculates your monthly disposable income using national and local expense standards, not your actual spending.

Offer in Compromise as Part of Your Response

An Offer in Compromise settles the debt for less than you owe. It's not a negotiation. It's a mathematical formula based on your equity in assets plus your future income over a specific period (typically 12 or 24 months depending on payment terms).

The IRS accepts offers when collection of the full amount is unlikely or creates economic hardship. After 32 years, I've seen the agency become more flexible on these, but you need documentation. Tax returns, bank statements, pay stubs, asset valuations.

Currently Not Collectible status is an option if you truly can't pay anything. The IRS suspends collection activity when your monthly income doesn't exceed your allowable expenses. They'll still file liens and the debt continues to accrue interest, but they stop active enforcement.

This status isn't permanent. The IRS reviews your financial situation periodically and can resume collection if your situation improves.

What Happens If You Ignore the CP91 or CP298

The levy starts. First payment hits about 60-90 days after the 30-day response period expires. You'll see 15% missing from your Social Security deposit, and it continues every month.

You can still request an equivalent hearing after the 30 days, but it won't stop the levy. The IRS continues taking its cut while you work through the appeals process. You'll eventually get the same hearing, same settlement options, same legal protections. Just without the automatic stay.

Some people wait, thinking the IRS will forget or the debt will age out. It won't. The 10-year collection statute gets suspended during bankruptcy, Offer in Compromise consideration, CDP hearings, and any period you're outside the country for six continuous months.

I've seen clients lose two years of Social Security payments before finally calling. That's $3,600 on a $2,000 monthly benefit. Money that doesn't come back even if you later settle for less.

How to File Form 12153 Correctly

The form itself is two pages. Sounds simple. But I've seen dozens rejected for incomplete information or missed deadlines.

Mail it to the address on your CP91 or CP298 notice. Not to your local IRS office. Not to the address where you file returns. The specific address listed on the notice. Each notice includes a dedicated fax number too. Use certified mail or fax with confirmation.

Section I asks for basic information. Name, Social Security number, contact details. Section II identifies what you're appealing. Check the box for "Notice of Intent to Levy."

Section III is where people stumble. You need to explain why you disagree and what you want instead. Be specific:

- "I disagree with the levy because I can pay the balance through an installment agreement of $300 per month."

- "I dispute the underlying liability. I never received a notice of deficiency for tax year 2022."

- "I request an Offer in Compromise. My equity in assets and future income is less than the amount owed."

Attach supporting documents. Financial statements, proof of income, asset valuations, prior correspondence with the IRS. The appeals officer assigned to your case will want this anyway.

Common Mistakes That Delay Your Response

| Mistake | Why It Matters | How to Avoid It |

|---|---|---|

| Missing the postmark deadline | IRS goes by postmark, not delivery date | Mail at least 5 days before the deadline |

| Wrong mailing address | Form gets routed incorrectly or lost | Use only the address on your specific notice |

| No proposed alternative | Appeals has nothing to evaluate | Offer specific payment amount or settlement option |

| Unsigned form | Invalid submission | Sign and date both pages where indicated |

The IRS will send you a letter acknowledging receipt, usually within 30 days. Then it assigns your case to an appeals officer, which can take 90-180 days depending on the backlog. During this time, the levy remains on hold.

Working With Appeals After Your CP91 CP298 Levy Notice Response

The appeals officer will contact you by letter, asking for additional information or scheduling a conference. These aren't court proceedings. No judge, no formal rules of evidence. Just a conversation about your financial situation and what you can realistically pay.

Bring your financial documentation to the conference. Bank statements, pay stubs, tax returns for the last two years, bills, proof of necessary expenses. The officer will compare your claimed expenses against IRS allowable expense standards.

You can represent yourself or have a tax attorney, CPA, or enrolled agent represent you. Representation isn’t legally required, but it helps if the numbers are complicated or you're proposing an Offer in Compromise.

Appeals officers have settlement authority. They can approve installment agreements, offers, partial payment plans, even penalty abatement if there's reasonable cause. They can also uphold the levy if you don't cooperate or your proposal is unrealistic.

Most cases settle. The IRS collects more through negotiated agreements than through enforced levies. They know taking 15% of your Social Security doesn't help if you end up in bankruptcy six months later.

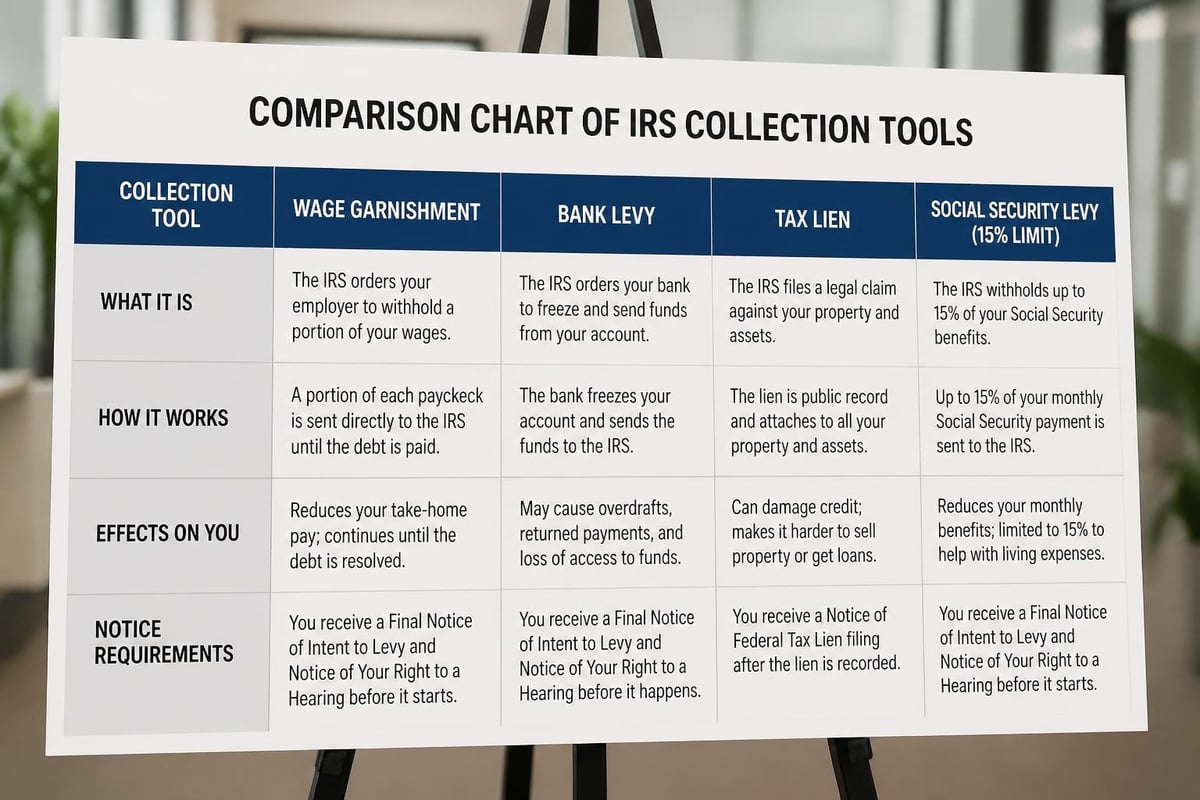

Social Security Levy vs. Other IRS Collection Tools

The IRS has easier collection methods. Wage garnishment grabs a bigger percentage and doesn't require special notices. Bank levies clean out your account in one shot. The IRS typically moves to Social Security levies when those options aren't available.

You're retired. No wages to garnish. Limited bank deposits. Social Security is the only steady income stream, so that's where the IRS goes.

Social Security levies have limitations other levies don't. The 15% cap is statutory. The IRS can't take more even if you owe millions. Compare that to wage garnishment, where the IRS can take 70% or more depending on your filing status and dependents.

Supplemental Security Income (SSI) is exempt from levy entirely. Only Social Security retirement, disability, and survivor benefits are reachable. If you're receiving SSI, the CP91 or CP298 is a mistake and you should contact the IRS immediately.

Statute of Limitations Protection

The IRS has 10 years from the date of assessment to collect. After that, the debt legally expires. But that clock pauses during certain events, and the levy itself doesn't extend it.

Your cp91 cp298 levy notice response can impact the collection statute. Filing a CDP hearing request suspends the statute during the hearing and any subsequent Tax Court appeal. That can add 18-24 months to the IRS's collection window.

An Offer in Compromise suspends it while the offer is pending, plus 30 days. Bankruptcy stops it entirely during the automatic stay. Time you spend outside the country for six continuous months doesn't count.

I've seen debts that should have expired in 2024 remain collectible until 2027 because of these suspensions. The IRS tracks this carefully. You should too.

Request your account transcript from the IRS to see the exact assessment date and expiration date (called CSED, Collection Statute Expiration Date). If you're close to the statute running, sometimes the best strategy is to request Currently Not Collectible status and wait it out.

When Innocent Spouse Relief Applies

If the tax debt arose from your spouse's or ex-spouse's actions, you might qualify for innocent spouse relief. This eliminates your liability entirely if you meet the requirements.

You must show:

- The tax debt came from your spouse's unreported income or improper deductions

- You didn't know and had no reason to know about the understatement when you signed the return

- It would be unfair to hold you responsible given all the facts

Innocent spouse claims require Form 8857 and supporting documentation. The IRS suspends collection while evaluating the request, including any pending levy.

Separation of liability is an alternative that allocates the debt between you and your spouse based on who earned the income or claimed the deduction. You're only liable for your portion.

These defenses come up frequently in CDP hearings when one spouse handled all the finances and the other signed returns without reviewing them. The IRS evaluates these claims on a case-by-case basis, looking at education level, involvement in finances, and whether there were signs of trouble you should have noticed.

Financial Hardship as a Defense

Economic hardship is a legitimate basis to challenge the levy. But the IRS defines hardship narrowly. You need to show that the levy prevents you from meeting basic living expenses.

Basic doesn't mean your actual lifestyle. It means the IRS's allowable expense standards. National standards for food, clothing, household supplies. Local standards for housing and transportation. Out-of-pocket health care costs if documented.

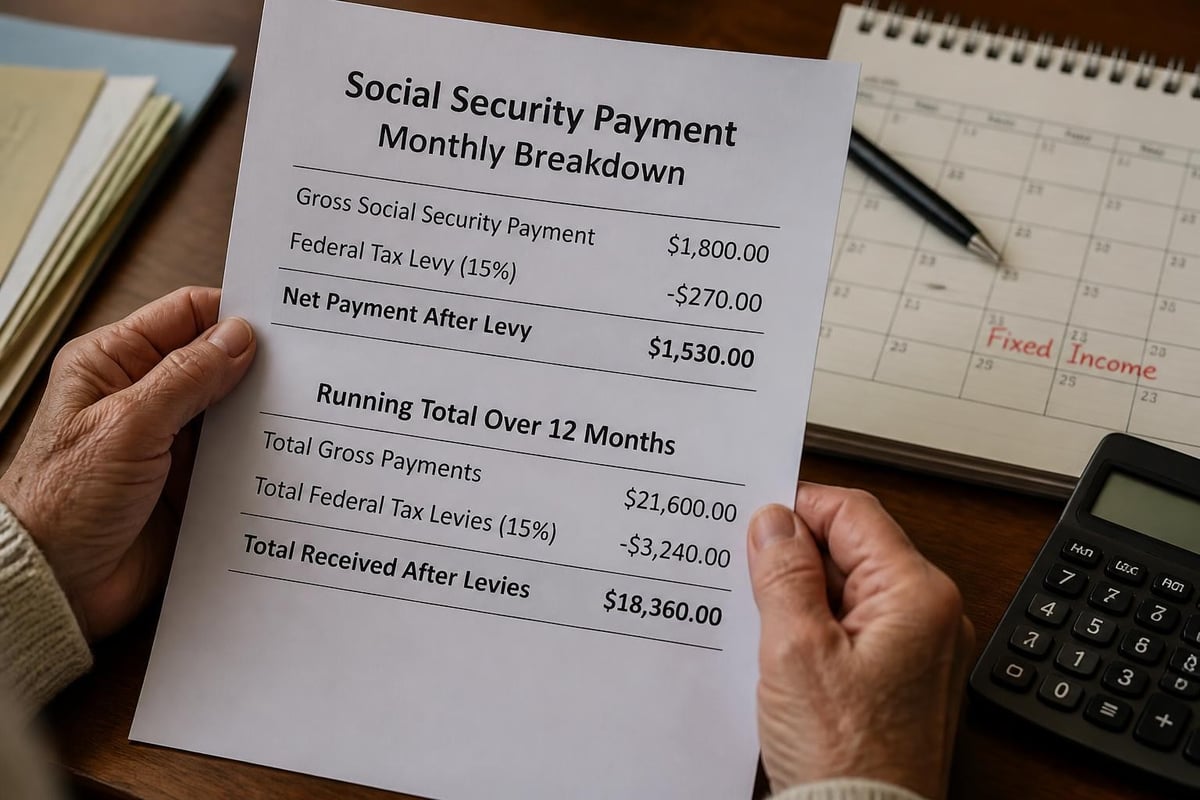

If your Social Security benefit is $1,800 per month and the IRS's allowable expenses for a single person in your county total $2,200, the 15% levy creates a $470 monthly shortfall on top of your existing $400 gap. That's documentable hardship.

You prove hardship through Form 433-A and supporting bills. Rent or mortgage statement, utility bills, car payment, insurance, prescriptions, medical expenses. The appeals officer reviews these against the standards and determines whether the levy should be released based on hardship.

Temporary hardship might result in Currently Not Collectible status. Permanent hardship combined with no assets might support an Offer in Compromise for a nominal amount.

Multiple Tax Years and Levy Priority

If you owe for several years, the IRS applies your Social Security levy payments to the oldest year first. Interest continues accruing on the newer years while the oldest debt gets paid down.

Your installment agreement can specify how payments get applied. You might want to target the year with the highest penalties, or the year closest to the collection statute expiring. The IRS will usually accommodate these requests if the overall payment covers more than they'd collect through levy.

Some taxpayers have a mix of assessed tax and unfiled returns. The IRS will typically refuse to negotiate until you file all required returns. The CP91 or CP298 might reference specific years, but there could be others the IRS hasn't assessed yet.

Filing those unfiled returns before your CDP hearing strengthens your position. It shows good faith and lets the appeals officer see the full scope of your liability when evaluating payment proposals.

What a Tax Attorney Does in Your CP91 CP298 Levy Notice Response

Representation isn't mandatory, but it changes the outcome more often than people expect. The appeals officer talks to your attorney instead of you. Financial information gets presented in the format the IRS expects. Legal arguments get made in the language the IRS understands.

An attorney can request a face-to-face conference when the phone isn't working. We can file motions to supplement the record if new information comes to light. We know which appeals officers settle and which dig in, because we've worked with them before.

After 32 years representing taxpayers, I know what documentation the IRS wants before they ask for it. What financial explanations they'll accept and which ones trigger deeper investigation. When to push for an Offer in Compromise and when to take the installment agreement.

The Law Offices of Darrin T. Mish, P.A. handles these cases nationwide. Initial consultation is free. We look at your notice, review your financial situation, and tell you what's realistic.

Most cases settle without litigation. The IRS wants to collect, not fight. But you need to give them a reason to accept less than the levy would produce. That requires financial analysis, procedural knowledge, and credibility that comes from doing this repeatedly.

Your cp91 cp298 levy notice response determines whether you keep control of your Social Security benefits or lose 15% every month until the debt is paid. The 30-day window is real, and the consequences of missing it are expensive. For 32 years, the Law Offices of Darrin T. Mish, P.A. has helped taxpayers navigate CDP hearings, negotiate payment plans, and stop Social Security levies before they start. If you've received a CP91 or CP298 notice, let's talk: Law Offices of Darrin T. Mish, P.A.