Quick answer: IRS Currently Not Collectible (CNC) status pauses IRS collection — no levies, no garnishments, no demand for payment — when paying would prevent you from meeting basic living expenses. The IRS still records the debt and reviews your status periodically. Penalty and interest continue to accrue. CNC is right for taxpayers with no realistic ability to pay, especially fixed-income retirees.

I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

When tax debt feels overwhelming and your finances are stretched beyond their limits, you might wonder if there's any breathing room available. The good news? The IRS recognizes that some taxpayers simply can't pay their tax debts without creating serious financial hardship. That's where IRS Currently Not Collectible status comes in. This lesser-known option can provide temporary relief from aggressive collection actions, giving you time to get back on your feet. Let's explore what this status means, how it works, and whether it might be the right solution for your situation.

What Is IRS Currently Not Collectible Status?

IRS Currently Not Collectible status is exactly what it sounds like: a determination by the IRS that your tax debt is, for now, not collectible. When you're granted this status, the IRS agrees to temporarily halt collection activities because paying your tax debt would leave you unable to meet basic living expenses.

Think of it as hitting the pause button on collections. The IRS won't garnish your wages, levy your bank accounts, or seize your assets while you're in this status. However, and this is crucial, your tax debt doesn't disappear. Interest and penalties continue to accrue, and the IRS can resume collection efforts if your financial situation improves.

How It Differs From Other Tax Relief Options

You might be wondering how this compares to other solutions like installment agreements or an Offer in Compromise. Here's the distinction:

- Installment Agreement: You make monthly payments toward your debt

- Offer in Compromise: You settle your debt for less than you owe

- Currently Not Collectible: Collections are paused, but you pay nothing

The IRS's Internal Revenue Manual provides detailed guidelines on how revenue officers determine whether a taxpayer qualifies for this special status. The determination centers on one key question: Can you pay your basic living expenses and your tax debt?

Who Qualifies for Currently Not Collectible Status?

Not everyone qualifies for IRS Currently Not Collectible status. The IRS conducts a thorough financial analysis to determine eligibility. Your monthly income must be equal to or less than your allowable living expenses.

Financial Hardship Criteria

The IRS looks at several factors when evaluating your request:

- Total monthly income from all sources

- Allowable living expenses based on IRS standards

- Equity in assets like homes, vehicles, and investments

- Ability to borrow against assets or income

If paying your tax debt would prevent you from covering necessary expenses like housing, food, transportation, and medical care, you might qualify. The keyword here is "necessary." The IRS uses national and local standards to determine what counts as reasonable living expenses.

Common Situations That May Qualify

Several life circumstances often lead to approval for this status:

- Unemployment or underemployment with limited job prospects

- Serious medical conditions creating substantial expenses

- Disability preventing you from working full-time

- Fixed retirement income that barely covers essentials

- Recent bankruptcy that depleted your resources

The Taxpayer Advocate Service provides valuable information about how economic hardship factors into these determinations.

The Application Process: What You Need to Know

Requesting IRS Currently Not Collectible status requires documentation and patience. The IRS doesn't grant this status lightly, so you'll need to prove your financial hardship convincingly.

Required Documentation

To support your request, gather these essential documents:

- Recent pay stubs (last three months)

- Bank statements showing all accounts

- Monthly bills for utilities, rent/mortgage, insurance

- Medical expense records if applicable

- Proof of assets including property values and vehicle worth

- Investment account statements

You'll also need to complete Form 433-F (Collection Information Statement) or Form 433-A if you're self-employed. These forms provide the IRS with a complete financial picture.

Steps to Request CNC Status

The process typically follows this sequence:

- Contact the IRS or wait for them to contact you about your debt

- Request Currently Not Collectible status during the conversation

- Complete the appropriate Collection Information Statement

- Submit supporting financial documentation

- Wait for the IRS to review your information

- Receive a determination letter

Many taxpayers find working with a tax attorney helpful during this process. An experienced professional knows what documentation strengthens your case and can communicate effectively with IRS representatives.

What Happens While You're in CNC Status?

Once the IRS grants you Currently Not Collectible status, several things occur simultaneously. Understanding both the benefits and the limitations helps you plan accordingly.

The Good News

| Benefit | What It Means |

|---|---|

| No wage garnishments | Your paycheck remains intact |

| No bank levies | Your accounts are protected |

| No asset seizures | The IRS won't take your property |

| Relief from pressure | Collection notices stop |

| Time to recover | You can focus on improving your finances |

The immediate relief can feel life-changing. When you're struggling to pay rent and buy groceries, not having the IRS garnishing your wages makes a real difference.

The Reality Check

However, Currently Not Collectible status isn't a permanent solution:

- Interest continues accruing on your tax debt at the federal rate

- Penalties keep adding up unless you've qualified for penalty abatement

- Your debt grows larger each month you're in this status

- The statute of limitations keeps running (usually 10 years from assessment)

- Tax refunds will be seized and applied to your balance

The IRS also periodically reviews your financial situation. If your income increases or your expenses decrease, they may remove you from CNC status and resume collection activities.

How Long Does CNC Status Last?

There's no fixed duration for IRS Currently Not Collectible status. It lasts as long as your financial hardship continues and the collection statute hasn't expired.

IRS Review Process

The IRS conducts periodic reviews to reassess your financial situation:

- Reviews typically occur every 1-2 years

- You may need to submit updated financial information

- The IRS can also review if they receive information suggesting your finances improved

- You must respond promptly to review requests to maintain your status

Some taxpayers remain in this status for years, while others see their situations improve more quickly. The key is understanding that it's a temporary measure, not a permanent fix.

When CNC Status Ends

Your Currently Not Collectible status terminates when:

- Your financial situation improves sufficiently

- The 10-year collection statute expires

- You fail to respond to IRS review requests

- You receive a large tax refund (indicating underwithheld taxes)

- You acquire significant assets or income

If your status ends due to improved finances, the IRS will resume collection efforts. This might mean setting up a payment plan or exploring other relief options.

Strategic Considerations and Alternatives

While IRS Currently Not Collectible status provides immediate relief, it's worth considering whether it's your best long-term option. Sometimes, other solutions make more sense financially.

Comparing Your Options

| Solution | Stops Collections | Reduces Debt | Monthly Payment | Best For |

|---|---|---|---|---|

| CNC Status | Yes | No | $0 | Severe hardship |

| Installment Agreement | Yes | No | Varies | Stable income |

| Offer in Compromise | Yes | Yes | Varies | Inability to pay full amount |

| Penalty Abatement | No | Partially | N/A | First-time penalty situations |

If you're considering settling with the IRS, an Offer in Compromise might resolve your debt permanently for less than you owe. However, qualifying is more difficult than getting CNC status.

The Growing Debt Problem

Here's something many people don't consider initially: while you're in Currently Not Collectible status, your debt continues growing. A $25,000 tax debt at 6% interest adds $1,500 annually. Over three years in CNC status, you'd owe over $4,500 more just in interest.

This reality makes the 10-year collection statute important. If you can remain in CNC status until the statute expires, the IRS can no longer collect the debt. However, this strategy requires careful monitoring and professional guidance.

Common Mistakes to Avoid

When dealing with IRS Currently Not Collectible status, taxpayers often make errors that complicate their situations. Avoiding these pitfalls protects your status and your future options.

Documentation Errors

The most frequent mistakes include:

- Underreporting income or failing to disclose all sources

- Omitting assets like second vehicles or investment accounts

- Inflating expenses beyond IRS allowable standards

- Missing deadlines for providing requested information

- Ignoring IRS correspondence during review periods

The IRS has access to extensive financial data through third-party reporting. Attempting to hide income or assets can result in denial of your request and potentially fraud charges.

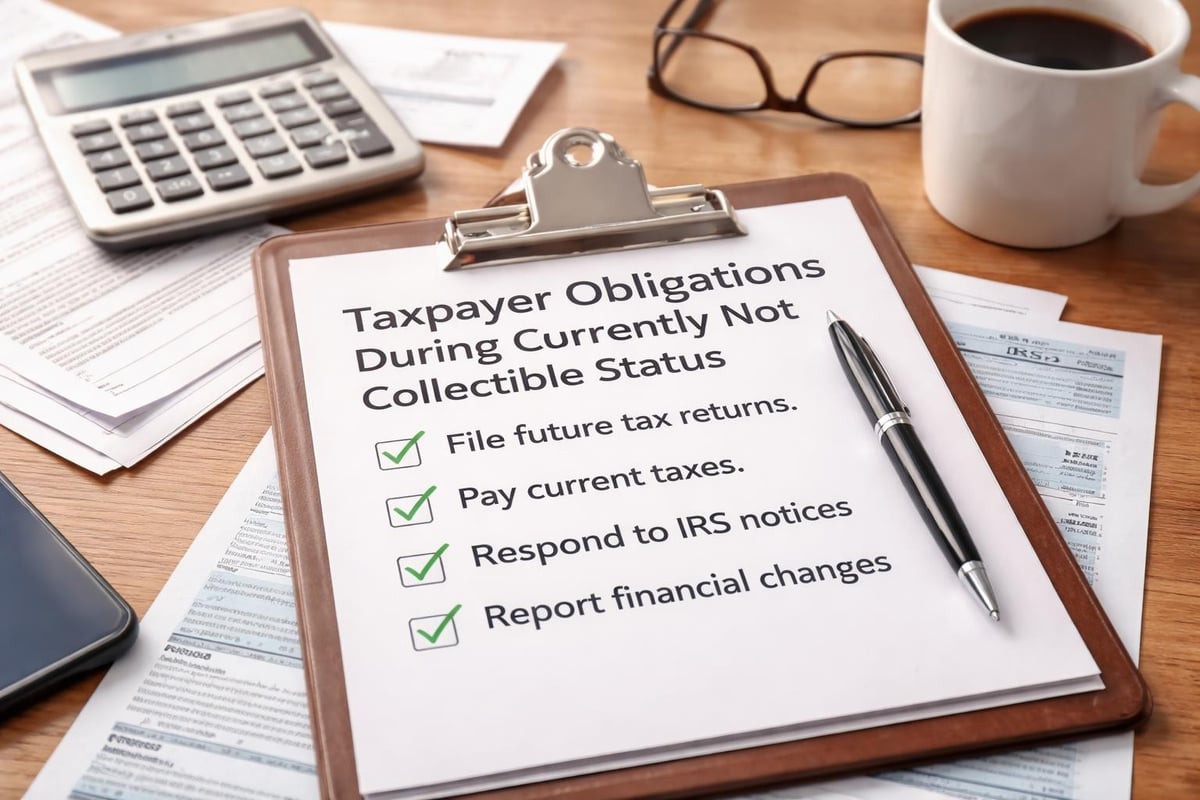

Ongoing Compliance Requirements

Even while in CNC status, you must:

- File all future tax returns on time

- Pay all current tax obligations as they come due

- Respond to IRS notices promptly

- Report significant financial changes to the IRS

- Maintain accurate records of your financial situation

Failing to file returns or pay current taxes can immediately terminate your Currently Not Collectible status. The IRS views these as signs you're not acting in good faith to resolve your tax problems.

Working With Tax Professionals

Navigating IRS Currently Not Collectible status can feel overwhelming, especially when you're already dealing with financial stress. Professional guidance often makes the difference between approval and denial.

What Tax Attorneys Bring to the Table

Experienced tax professionals understand:

- Which expenses the IRS considers allowable

- How to present financial information persuasively

- What documentation strengthens your case

- How to negotiate with revenue officers effectively

- When CNC status is the best option versus alternatives

A tax attorney can also help you understand how tax debt relates to other financial challenges you might be facing, like bankruptcy or debt settlement.

The Value of Experience

According to Debt.org, taxpayers who work with tax professionals often achieve better outcomes in their dealings with the IRS. Professionals know how to avoid common pitfalls and can advocate on your behalf throughout the process.

This is particularly important if you're also dealing with unfiled tax returns or wage garnishment situations that need immediate attention.

Life After Currently Not Collectible Status

Eventually, your financial situation will likely improve, or the collection statute will expire. Planning for what comes next ensures you're prepared when CNC status ends.

Building Toward Resolution

While in Currently Not Collectible status, consider:

- Improving your financial literacy to prevent future tax problems

- Building emergency savings when possible

- Increasing your income through education or skill development

- Monitoring the statute of limitations on your tax debt

- Exploring long-term solutions like an Offer in Compromise

Some taxpayers use the breathing room CNC status provides to prepare for a more permanent solution. You might save up a lump sum to propose an Offer in Compromise or improve your income enough to afford a reasonable installment agreement.

Preventing Future Tax Debt

Learning from this experience helps you avoid repeating it:

- Adjust your withholding to match your actual tax liability

- Make estimated tax payments if you're self-employed

- Set aside money regularly for tax obligations

- Consider working with a tax professional for tax planning

- Stay current with all filing and payment requirements

The goal isn't just to survive this tax debt, but to build habits that prevent creating new debt.

Understanding Your Rights and Protections

As a taxpayer dealing with the IRS, you have specific rights protected by law. Understanding these rights empowers you throughout the Currently Not Collectible process.

Taxpayer Bill of Rights

You have the right to:

- Be informed about your tax obligations

- Quality service from IRS employees

- Pay only the correct amount of tax

- Challenge the IRS's position and be heard

- Appeal IRS decisions in an independent forum

- Finality in knowing the maximum time the IRS has to collect

- Privacy and confidentiality

- Professional and courteous treatment

- Representation before the IRS

The Taxpayer Advocate Service serves as an independent organization within the IRS that helps taxpayers resolve problems and ensures these rights are protected.

When to Seek Additional Help

Consider escalating your case if:

- The IRS denies your CNC request despite clear hardship

- Revenue officers treat you unprofessionally

- You face immediate enforcement action despite pending review

- Your financial information is handled improperly

- Standard procedures aren't resolving your situation

Tax attorneys can help you navigate appeals processes and ensure the IRS follows proper procedures in your case.

IRS Currently Not Collectible status offers essential relief when financial hardship makes tax debt impossible to pay, but it requires careful documentation and ongoing compliance. While this status pauses collection activities, your debt continues growing, making professional guidance valuable for long-term planning. If you're struggling with overwhelming tax debt and need expert help navigating your options, the Law Offices of Darrin T. Mish, P.A. offers free consultations to help you understand your best path forward, whether that's CNC status or another solution tailored to your unique situation.

How to Apply for IRS Currently Not Collectible Status

- Step 1: Confirm CNC is the right move CNC pauses collection but doesn’t eliminate debt. Penalties and interest keep accruing. CNC is right when no realistic ability to pay exists for the foreseeable future.

- Step 2: File any missing tax returns The IRS requires compliance before granting CNC. Pull your account transcripts and file every missing return — even if you can’t pay.

- Step 3: Build your Form 433-F or 433-A Document monthly income and allowable expenses (housing, transportation, food, healthcare). Show that monthly disposable income is at or near zero. Use national/local IRS standards plus actual receipts.

- Step 4: Call the IRS to request CNC verbally Often fastest. Call the number on your most recent notice or the Practitioner Priority Service. Have your 433-F ready and request ‘currently not collectible’ status.

- Step 5: Respond to follow-up document requests The IRS may ask for bank statements, paystubs, or expense receipts. Respond promptly with what they ask for. Delays often kill CNC applications.

- Step 6: Watch for periodic review notices The IRS reviews CNC status annually based on your tax return income. If income rises, the IRS may revoke CNC and demand a new financial. Stay on top of this.