I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Owing money to the IRS can feel overwhelming, but you're not alone. Every year, millions of Americans face tax debt, and the good news is that you have multiple options to settle tax obligations with the government. Whether you're dealing with a few thousand dollars or a six-figure balance, understanding your settlement options is the first step toward financial freedom. The IRS offers various programs designed to help taxpayers resolve their debts, and with the right approach, you can find a solution that works for your specific situation.

Understanding Your Options to Settle Tax Debt

When you owe the IRS, doing nothing is the worst strategy. The government has significant collection powers, including the ability to garnish your wages, levy your bank accounts, and place liens on your property. But here's what many people don't realize: the IRS would rather work with you than chase you down.

The key to successfully resolving your tax situation is understanding which settlement option fits your circumstances. Not every taxpayer qualifies for every program, and choosing the wrong path can waste valuable time and money.

The Offer in Compromise: Settling for Less

An Offer in Compromise (OIC) allows you to settle tax debt for less than the full amount you owe. It sounds too good to be true, right? Well, there's a catch. The IRS only accepts offers when they believe it's the most they can reasonably collect from you.

To qualify for an OIC, you'll need to demonstrate one of three conditions:

- Doubt as to Collectibility: You can't pay the full amount within the collection statute period

- Doubt as to Liability: There's genuine dispute about whether you owe the tax

- Effective Tax Administration: Collecting the full amount would create economic hardship or would be unfair

The IRS examines your income, expenses, asset equity, and future earning potential. They're looking at your complete financial picture. If you have significant assets or earning capacity, your offer will likely be rejected.

Here's something most people miss: only about 40% of offers are accepted. The application requires detailed financial disclosure, a $205 application fee (waived for low-income taxpayers), and either a lump sum or periodic payment format. You can learn more about tax debt solutions that include the OIC program and other alternatives.

Payment Plans and Installment Agreements

If you can't settle tax obligations for less than you owe, an installment agreement might be your best bet. This approach lets you pay your debt over time in manageable monthly payments.

Short-Term Payment Plans

For debts under $100,000, you can request up to 180 days to pay in full. There's no setup fee, but interest and penalties continue to accrue. This works well if you're expecting a bonus, tax refund, or other lump sum in the near future.

Long-Term Installment Agreements

When you need more than 180 days, long-term payment plans extend the repayment period. The IRS offers several types:

| Agreement Type | Debt Threshold | Setup Fee | Requirements |

|---|---|---|---|

| Guaranteed | Under $10,000 | $31-$225 | Paid within 3 years |

| Streamlined | Under $50,000 | $31-$225 | Paid within 72 months |

| Non-Streamlined | Over $50,000 | $31-$225 | Financial disclosure required |

| Partial Payment | Any amount | $225 | Periodic review required |

Direct debit payments reduce your setup fee significantly. If you're facing wage garnishment or other collection actions, an installment agreement typically halts those activities once approved. For taxpayers concerned about protecting Social Security from garnishment, entering into a payment plan can provide crucial protection.

Currently Not Collectible Status

Sometimes the best way to settle tax issues isn't to pay right away. If paying would prevent you from meeting basic living expenses, the IRS may place your account in Currently Not Collectible (CNC) status.

This isn't debt forgiveness. The IRS simply acknowledges that collecting from you right now would cause financial hardship. They'll pause collection activities, but your debt continues to accrue interest and penalties.

Who Qualifies for CNC Status?

You'll need to prove that your necessary living expenses exceed your income. The IRS uses national and local standards to determine reasonable expense amounts. They won't accept excessive housing costs or luxury vehicle payments.

CNC status typically lasts until your financial situation improves. The IRS periodically reviews your account, and if your income increases, they'll restart collection efforts. However, here's an important detail: the collection statute of limitations continues to run. After 10 years, the IRS can no longer collect the debt, even if it remains unpaid.

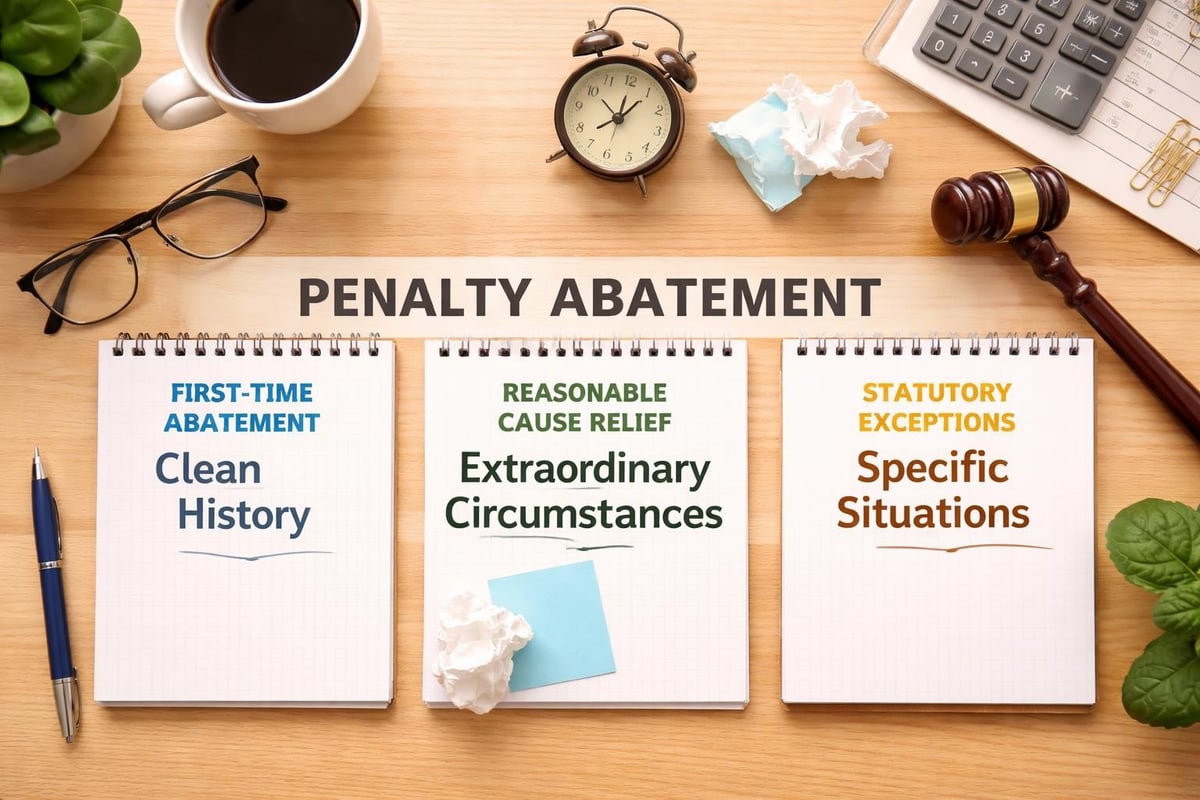

Penalty Abatement: Reducing What You Owe

You might not settle tax debt entirely, but reducing penalties can significantly decrease your balance. Penalties often represent 25% or more of your total debt, so elimination makes a real difference.

The IRS offers several penalty relief options:

- First-Time Penalty Abatement: If you have a clean compliance history

- Reasonable Cause: For penalties resulting from circumstances beyond your control

- Statutory Exceptions: For specific situations defined by law

First-time abatement is the easiest to obtain. If you've filed and paid on time for the previous three years and you're currently compliant, you'll likely qualify. The IRS will waive failure-to-file, failure-to-pay, and failure-to-deposit penalties.

Reasonable cause requires demonstrating that you exercised ordinary business care but couldn't meet your obligations due to circumstances beyond your control. This includes natural disasters, serious illness, death in the family, or reliance on incorrect professional advice.

Innocent Spouse Relief: When Your Partner's Debt Isn't Yours

What happens when you file jointly but your spouse creates the tax problem? You shouldn't have to settle tax obligations that resulted from your spouse's actions, and the law recognizes this through innocent spouse relief.

This relief comes in three forms:

- Classic Innocent Spouse Relief: For understatements of tax due to your spouse's errors

- Separation of Liability: Allocates tax debt between divorced or separated spouses

- Equitable Relief: For situations not covered by the other two types

To qualify, you must prove you didn't know (and had no reason to know) about the understatement when you signed the return. The IRS considers your education level, involvement in finances, and whether you benefited from the understated tax.

The application process involves Form 8857 and detailed documentation. Success stories are powerful. In one case, a client faced over $211,000 in tax debt from their spouse's business activities, and through innocent spouse relief, the entire debt was completely forgiven.

Bankruptcy and Tax Debt

Can you discharge tax debt in bankruptcy? Sometimes, yes. Income tax debt can be eliminated in Chapter 7 bankruptcy if it meets specific criteria:

- The tax debt is from income taxes (not payroll taxes or penalties)

- The tax return was due at least three years ago

- You filed the return at least two years ago

- The IRS assessed the tax at least 240 days ago

- You didn't commit fraud or willful evasion

Even if your tax debt qualifies for discharge, bankruptcy has serious consequences for your credit and financial future. It's typically a last resort after exploring other options to settle tax problems. You'll want to consult both a tax attorney and bankruptcy attorney before proceeding.

Mediation and Appeals

When you disagree with the IRS's position, you don't have to accept their decision. The IRS mediation program provides an alternative dispute resolution process that can help you reach agreement without litigation.

The Appeals Process

IRS Appeals is an independent organization within the IRS. They review cases where taxpayers disagree with IRS examinations, collection actions, or other determinations. The appeals officer considers both the government's position and yours, looking for a mutually acceptable resolution.

You can request appeals consideration for:

- Audit results you disagree with

- Offer in Compromise rejections

- Trust Fund Recovery Penalty assessments

- Collection Due Process hearings

- Innocent spouse claim denials

The appeals process is less formal than Tax Court. You don't need an attorney, though having one often improves your outcome. Appeals officers have settlement authority and can compromise cases based on hazards of litigation.

Working with Tax Professionals

Should you try to settle tax debt on your own or hire help? The answer depends on your situation's complexity and the amount you owe.

For simple payment plans on modest debts, you might handle it yourself. The IRS website provides clear instructions, and the process is straightforward. But for offers in compromise, penalty abatement beyond first-time relief, or innocent spouse claims, professional help usually pays for itself.

Types of Tax Professionals

Different professionals offer different services:

| Professional | Representation Rights | Best For |

|---|---|---|

| Enrolled Agent | Full IRS representation | Most tax matters |

| CPA | Full IRS representation | Complex financial situations |

| Tax Attorney | Full IRS representation + litigation | Legal issues, criminal exposure |

| Tax Resolution Company | Through employed professionals | Straightforward cases |

Tax attorneys bring unique value when legal issues arise. They provide attorney-client privilege, understand tax law intricacies, and can represent you in Tax Court. When dealing with IRS programs and settlement options, experienced legal guidance helps you navigate the system effectively.

Understanding Tax Research and Authority

When you're working to settle tax issues, understanding the hierarchy of tax law helps you evaluate your options. The U.S. tax system relies on authoritative tax references that determine how tax law applies.

Primary authorities include the Internal Revenue Code, Treasury Regulations, and court decisions. Secondary authorities like IRS publications and private letter rulings provide guidance but don't carry the same weight. This distinction matters when negotiating with the IRS or evaluating your position.

State Tax Settlements

Don't forget about state taxes. While this guide focuses on federal obligations, many states offer similar programs to settle tax debt. For instance, Washington State operates a settlement track process for resolving disputes efficiently.

State programs vary significantly. Some states are more flexible than the IRS, while others are stricter. If you owe both federal and state taxes, coordinate your settlement strategy to address both simultaneously.

The Collection Statute of Limitations

Here's something crucial: the IRS generally has 10 years to collect tax debt. This Collection Statute Expiration Date (CSED) starts from the assessment date, not when you filed or the tax was due.

Certain actions extend the CSED:

- Filing an Offer in Compromise (plus 1 year)

- Requesting a Collection Due Process hearing

- Filing bankruptcy

- Living outside the United States for 6+ months

- Filing a request for innocent spouse relief

If you're close to the CSED, waiting might be better than settling. However, the IRS knows this too and may accelerate collection efforts as the deadline approaches. They might file a lawsuit to obtain a judgment, which extends their collection period significantly.

Staying Compliant During Settlement

Whatever method you choose to settle tax obligations, current compliance is non-negotiable. The IRS won't consider installment agreements or offers if you're not filing current returns and paying current taxes.

This creates challenges for self-employed individuals and business owners with ongoing tax obligations. You might be negotiating 2021 debt while owing 2026 estimated taxes. The IRS expects both to be addressed.

Setting up estimated tax payments through withholding or quarterly payments demonstrates good faith. It also prevents your current situation from getting worse while you're resolving past issues. When working with tax debt relief programs, maintaining compliance strengthens your position.

Common Mistakes to Avoid

Having worked with thousands of taxpayers, certain mistakes appear repeatedly. Avoiding these pitfalls improves your chances of successfully resolving your tax situation.

Ignoring IRS notices. Every notice has a deadline and consequences for non-response. Missing deadlines eliminates options and strengthens the IRS's position.

Providing incomplete financial information. The IRS will reject offers and payment plan requests with missing documentation. Complete disclosure upfront saves time and improves outcomes.

Continuing non-compliance. You can't settle past tax problems while creating new ones. File all required returns before requesting settlement.

Accepting the first option presented. IRS revenue officers often push for immediate full payment or quick installment agreements. You might qualify for better terms with proper analysis.

Believing tax resolution company promises. If someone guarantees to settle your debt for "pennies on the dollar," be skeptical. Legitimate professionals explain your actual options, not fantasy scenarios.

Successfully resolving tax debt requires understanding your options, meeting IRS requirements, and choosing the right strategy for your situation. Whether through payment plans, offers in compromise, or penalty abatement, solutions exist for virtually every tax problem. The Law Offices of Darrin T. Mish, P.A. has helped clients worldwide resolve complex IRS issues for over three decades, offering the personalized legal guidance needed to achieve lasting resolution. If you're ready to settle your tax debt and move forward, Law Offices of Darrin T. Mish, P.A. offers free consultations to evaluate your situation and chart the best path forward.