I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Getting a debt forgiven sounds like a dream come true, right? You've been struggling with credit card bills or a personal loan, and suddenly your creditor agrees to settle for less than you owe. But before you celebrate too hard, there's something you need to know: that forgiven amount might create a tax bill you weren't expecting. The debt relief tax can turn financial relief into a tax headache if you're not prepared. Understanding how the IRS treats canceled debt is crucial for anyone seeking debt relief or facing insolvency in 2026.

How the IRS Views Forgiven Debt

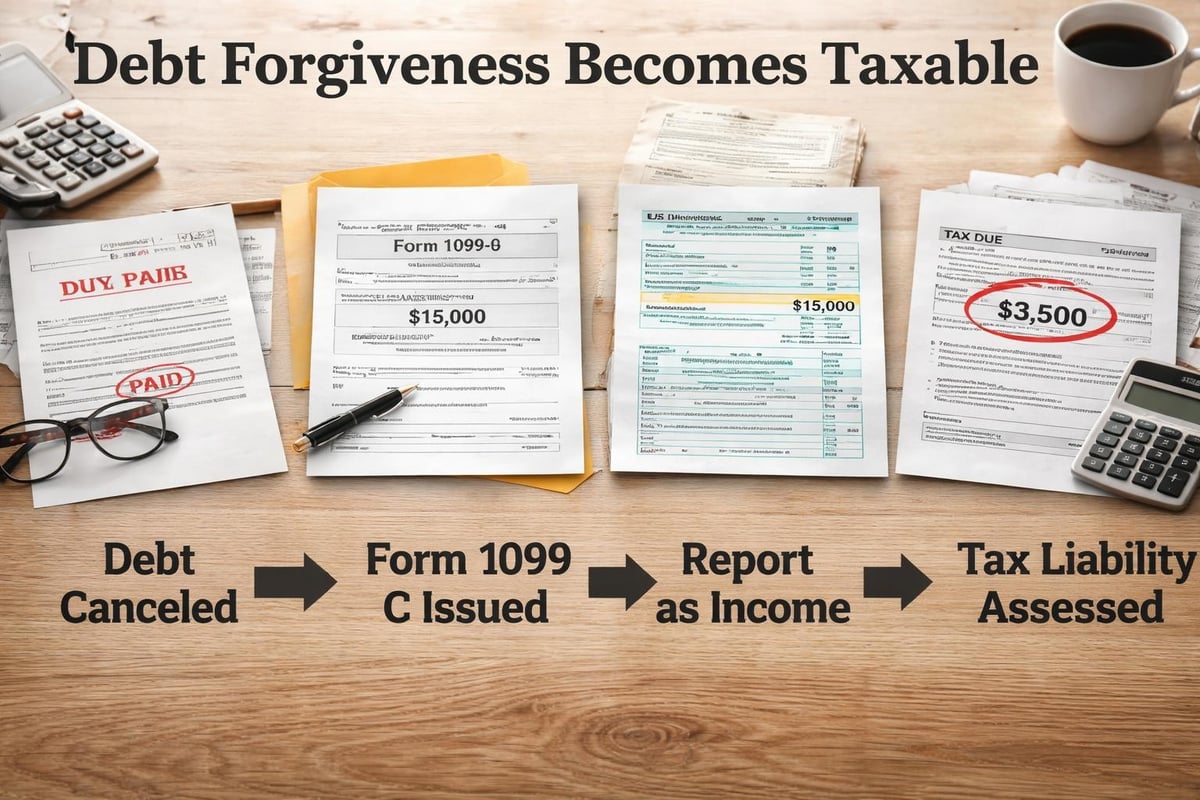

When a creditor forgives $600 or more of your debt, they're required to report it to the IRS using Form 1099-C, Cancellation of Debt. From the IRS's perspective, that forgiven amount represents income you received. Think about it this way: you borrowed money, used it for goods or services, and now you don't have to pay it back. The IRS sees that as a financial gain.

This tax treatment of canceled debt applies to various types of debts, including:

- Credit card balances

- Personal loans

- Auto loans

- Medical bills

- Second mortgages or home equity lines of credit

The debt relief tax typically kicks in during the year the debt is officially canceled or discharged. You'll receive that 1099-C form, and you're expected to report it as "other income" on your tax return. This can come as a shock to taxpayers who thought settling a debt meant walking away clean.

Why This Catches People Off Guard

Most people pursuing debt settlement are already in financial distress. The last thing they expect is a tax bill on money they never actually received in cash. But from a tax law perspective, the logic is straightforward: you had the use of that money, purchased things with it, and now you don't have to repay it. That's economically equivalent to earning income.

Common Scenarios That Trigger Debt Relief Tax

Understanding when the debt relief tax applies helps you plan ahead. Different situations create different tax consequences, and knowing the landscape can help you make informed decisions about settling IRS debt or negotiating with other creditors.

Credit Card Debt Settlement

Credit card debt settlement is one of the most common triggers. If you negotiate with your credit card company to pay $5,000 on a $10,000 balance, that remaining $5,000 becomes taxable income. According to CNBC’s analysis of forgiven debt taxes, this catches many consumers completely unprepared.

The timing matters too. The debt becomes taxable in the year it's officially discharged, not necessarily when you make your settlement payment. This can create budgeting challenges if you're already stretched thin financially.

Mortgage Foreclosure and Short Sales

Real estate debt forgiveness creates particularly complex tax situations. When a bank forecloses on your home or agrees to a short sale where the selling price doesn't cover the mortgage, the forgiven balance typically generates a 1099-C. The IRS provides specific guidance on home foreclosure and debt cancellation that can be both confusing and consequential.

| Type of Real Estate Debt | Taxable? | Key Consideration |

|---|---|---|

| Principal Residence (2007-2025) | Sometimes Exempt | Mortgage Forgiveness Debt Relief Act applied |

| Investment Property | Usually Taxable | Limited exceptions available |

| Second Home | Usually Taxable | Not covered by MFDRA |

| Home Equity Debt (non-qualifying) | Usually Taxable | Depends on use of funds |

Business Debt Cancellation

Business owners face unique debt relief tax challenges. If you close your business and creditors forgive business debts, that cancellation creates taxable income on your business tax return. The structure of your business matters significantly here. Sole proprietors report it on Schedule C, while corporations and partnerships have different reporting requirements.

Critical Exceptions That Can Save You

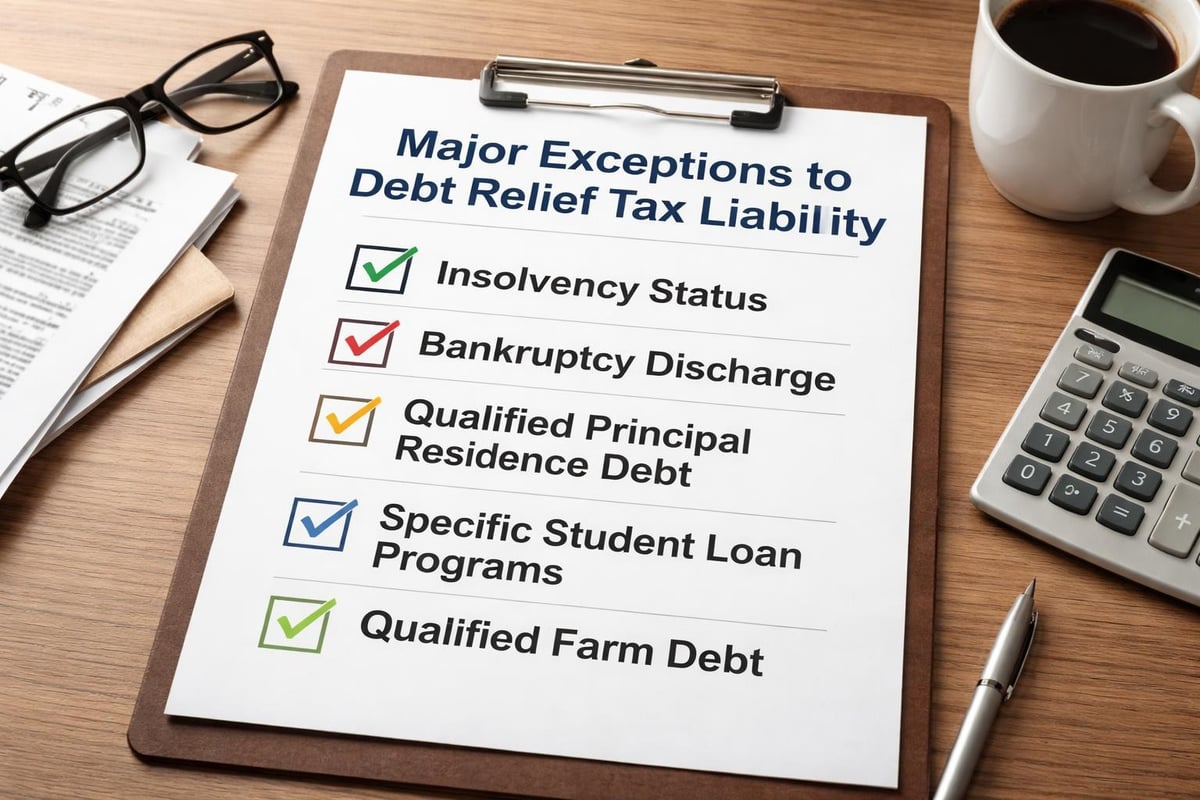

Here's the good news: not all forgiven debt is taxable. The tax code includes several important exceptions that might shield you from the debt relief tax entirely. Understanding these exceptions is crucial before you panic about a 1099-C in your mailbox.

The Insolvency Exception

The insolvency exception is the most commonly used escape route from debt relief tax. If you were insolvent immediately before the debt was canceled, you can exclude some or all of the forgiven debt from your income. But what does "insolvent" actually mean?

You're insolvent when your total liabilities exceed your total assets. The IRS requires you to calculate this carefully using Form 982, Reduction of Tax Attributes. You'll list everything you own (house, car, retirement accounts, checking accounts) and everything you owe (mortgages, credit cards, medical bills, personal loans).

Let's say your debts total $80,000 and your assets total $50,000. You're insolvent by $30,000. If a creditor forgives $15,000 of debt, you can exclude the entire amount because your insolvency ($30,000) exceeds the forgiven debt ($15,000). This exception provides significant relief for people in genuine financial hardship.

Bankruptcy Discharge

Debts discharged in bankruptcy are not taxable. This is one of the few absolute rules in the debt relief tax arena. Whether you file Chapter 7, Chapter 11, or Chapter 13 bankruptcy, debts eliminated through the bankruptcy process don't create tax liability. This makes bankruptcy potentially more attractive from a tax perspective compared to debt settlement outside of bankruptcy.

Qualified Principal Residence Indebtedness

The Mortgage Forgiveness Debt Relief Act of 2007 created a special exception for mortgage debt on your principal residence. Originally set to expire after 2012, Congress extended this provision multiple times. For debts discharged through 2025, you could exclude up to $2 million ($1 million if married filing separately) of forgiven mortgage debt on your main home.

However, as of 2026, this provision has expired unless Congress extends it again. This makes the timing of any mortgage debt forgiveness critical for tax planning purposes. Always check current law before assuming this exclusion applies.

Student Loan Forgiveness Programs

Certain student loan forgiveness programs don't trigger the debt relief tax. Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and loans forgiven due to death or total disability fall into this category. However, income-driven repayment plans that forgive remaining balances after 20-25 years of payments did create taxable income before recent law changes.

The American Rescue Plan Act of 2021 made student loan forgiveness tax-free through 2025, but this provision has also expired in 2026 unless extended. If you're in an income-driven repayment plan, this is something to monitor closely.

How to Calculate Your Debt Relief Tax Liability

Once you determine that forgiven debt is taxable, you need to calculate your actual tax liability. This isn't as simple as applying a flat percentage to the forgiven amount. The debt relief tax depends on your overall tax situation.

Understanding Marginal Tax Rates

The forgiven debt gets added to your other income for the year. Your tax liability depends on which tax bracket that additional income falls into. Federal income tax rates for 2026 range from 10% to 37%, depending on your filing status and total income.

For example, if you're single and your regular income is $60,000, and you have $10,000 of forgiven debt reported on a 1099-C, your total income becomes $70,000. That $10,000 gets taxed at your marginal rate, which could be 22% at those income levels, creating about $2,200 in additional federal tax.

State Tax Considerations

Don't forget about state income taxes. Most states follow federal tax treatment of canceled debt, meaning if it's taxable federally, it's taxable at the state level too. Florida residents have an advantage here since Florida has no state income tax, but residents of California, New York, or other high-tax states could face significant combined tax bills.

Filing Form 982

If you qualify for any exceptions, you must file Form 982 with your tax return. This form allows you to exclude canceled debt from income based on insolvency, bankruptcy, or other qualifying circumstances. Many taxpayers miss this step and end up paying taxes on debt they could have legally excluded.

Form 982 requires detailed calculations of your assets and liabilities. Getting help from a tax attorney specializing in IRS debt can ensure you complete this form correctly and claim all available exceptions.

Dealing With Multiple 1099-C Forms

Receiving multiple 1099-C forms in a single year compounds the debt relief tax problem. If you settled several debts as part of a comprehensive debt relief strategy, each forgiveness over $600 generates its own 1099-C, and they all stack up as additional income.

Here's how to approach multiple forms:

- Gather all your 1099-C forms as soon as they arrive (creditors must send them by January 31)

- Calculate your total canceled debt across all forms

- Determine your insolvency status on the date each debt was canceled

- Complete a separate Form 982 if needed, showing calculations for each cancellation

- Report everything accurately on your tax return, even if you're excluding it from income

The debt settlement tax implications can become quite complex when multiple debts are involved, especially if the cancellations occurred on different dates throughout the year.

The IRS Debt Relief Tax Trap

Here's an ironic situation that traps many taxpayers: what happens when the IRS itself forgives your tax debt? Yes, even forgiven tax debt can create new tax liability, though the rules work differently than with regular creditor debt.

Offer in Compromise Considerations

When you settle tax debt through an Offer in Compromise, you might assume the forgiven portion doesn't create new tax debt. In most cases, you'd be right, but not for the reasons you might think. The IRS typically accepts offers only when you demonstrate inability to pay, which usually means you're insolvent. The insolvency exception then applies to exclude the forgiven tax debt from income.

However, if your financial situation improves significantly before the offer is formally accepted, you could theoretically face taxable income from forgiven tax debt. This is rare but worth understanding.

Penalty Abatement Doesn't Create Income

Good news here: when the IRS grants penalty abatement, the forgiven penalties don't create taxable income. Penalties aren't considered debt principal for tax purposes. The same applies to forgiven interest in most circumstances. This makes pursuing penalty relief a tax-efficient strategy for reducing what you owe.

Planning Ahead to Minimize Debt Relief Tax

Strategic planning can significantly reduce or eliminate the debt relief tax burden. If you're considering debt settlement, foreclosure, or other actions that might trigger canceled debt, advance planning makes all the difference.

Timing Debt Settlement

If possible, time your debt settlements for years when your income is lowest. Since the debt relief tax depends on your marginal tax rate, settling debt when you're unemployed or have unusually low income can reduce the tax impact. This requires coordinating with creditors, which isn't always possible, but it's worth attempting.

Documenting Insolvency

If you believe you're insolvent, document your financial situation meticulously. Create a detailed balance sheet showing all assets and liabilities on the date each debt is canceled. Keep:

- Bank statements

- Property valuations

- Vehicle blue book values

- Retirement account statements

- Credit card statements

- Loan documents

- Medical bills

This documentation proves insolvency if the IRS questions your Form 982 exclusion. Without solid documentation, the IRS might disallow your exclusion and assess additional taxes, penalties, and interest.

Considering Bankruptcy vs. Settlement

From a pure tax perspective, bankruptcy often beats debt settlement because bankruptcy-discharged debts never create taxable income. However, bankruptcy has other consequences for your credit and financial life. Understanding how taxes interact with debt forgiveness helps you make informed decisions about which debt relief path makes sense for your situation.

What to Do When You Receive a 1099-C

Don't ignore a 1099-C. The IRS receives a copy too, and their computers will flag your return if you don't report it. Even if you believe the canceled debt isn't taxable, you must address it on your tax return.

Verify the Information

First, check whether the 1099-C is accurate. Creditors sometimes issue these forms in error or for debts that were actually paid. If you believe the form is incorrect, contact the creditor immediately and request a corrected form. If they refuse, you'll need to report the issue to the IRS with supporting documentation.

Report It Properly

Even if the debt is excludable, you typically need to report the 1099-C on your return. You'll show the canceled debt as income, then subtract it out using Form 982 if you qualify for an exclusion. This shows the IRS you received the form and handled it properly rather than simply ignoring it.

Get Professional Help

The debt relief tax rules are complex, and mistakes can be costly. Working with a qualified tax professional who understands IRS tax debt relief programs ensures you claim all available exceptions and avoid triggering audits or additional tax assessments.

Common Mistakes That Cost Taxpayers

Through decades of practice, certain patterns emerge in how taxpayers mishandle the debt relief tax. Avoiding these common mistakes can save you significant money and stress.

Assuming All Forgiven Debt Is Tax-Free

The biggest mistake is assuming debt forgiveness never creates tax liability. While exceptions exist, the default rule is that canceled debt equals taxable income. Always verify your situation against the specific exceptions rather than making assumptions.

Failing to File Form 982

Many taxpayers qualify for insolvency or other exceptions but fail to file the required Form 982. Without this form, the IRS has no way to know you're claiming an exception. They'll assess tax on the full amount reported on the 1099-C, plus penalties and interest when you don't pay.

Miscalculating Insolvency

Calculating insolvency seems straightforward, but it's easy to make mistakes. Common errors include:

- Overvaluing assets (using purchase price instead of current market value)

- Forgetting debts (overlooking medical bills, personal loans from family, or other obligations)

- Using the wrong date (insolvency must be measured immediately before debt cancellation, not weeks or months earlier)

- Including exempt assets (retirement accounts sometimes receive different treatment)

These calculation errors can mean the difference between owing thousands in taxes or owing nothing.

Ignoring State Tax Consequences

Even if you exclude canceled debt from federal income, check your state's rules. Some states don't conform to all federal exclusions, meaning debt that's tax-free federally might still be taxable at the state level. This varies significantly by state.

The Interaction Between Debt Relief Tax and Other IRS Issues

The debt relief tax doesn't exist in isolation. It interacts with other tax obligations and IRS procedures in ways that can create additional complications.

Impact on Tax Refunds

If you owe back taxes and also have cancellation of debt income, the IRS might keep any refund you're expecting. They'll apply it against your existing tax debt. This can be frustrating if you were counting on that refund to pay your current year's taxes on the forgiven debt.

Liens and Levies

Outstanding IRS liens don't prevent creditors from forgiving debt or issuing 1099-C forms. However, if forgiven debt creates new tax liability that you can't pay, the IRS might file new liens against any property you own. This creates a frustrating cycle where resolving one debt problem creates another.

Payment Plans for New Tax Debt

If the debt relief tax creates a tax bill you can't immediately pay, you'll need to address it with the IRS. Options include:

| Solution | Best For | Key Requirements |

|---|---|---|

| Installment Agreement | Those who can pay over time | Steady income, filed returns |

| Currently Not Collectible | Those with no ability to pay | Financial hardship documentation |

| Offer in Compromise | Those qualifying for settlement | Insolvency or special circumstances |

| Penalty Abatement | Those with reasonable cause | First-time penalty or documented hardship |

Understanding your IRS tax relief options helps you address new tax debt from canceled obligations without falling further behind.

How Tax Reform Affects Debt Relief Tax

Tax laws constantly evolve, and recent changes have significantly impacted how the debt relief tax works. Staying current on these changes is essential for proper planning.

Temporary Relief Provisions

Congress periodically extends or modifies debt relief tax rules, often in response to economic crises. The 2020 pandemic led to various temporary expansions of relief provisions. Some of these have expired while others continue. The mortgage debt forgiveness exclusion, for instance, has been repeatedly extended and allowed to expire throughout the past decade.

The Build Back Better Act and Student Loans

Recent legislation made student loan forgiveness temporarily tax-free through 2025. As of 2026, unless Congress acts, student loan forgiveness under income-driven repayment plans will again create taxable income. This could create substantial tax bills for borrowers who have been in repayment for 20-25 years and are approaching forgiveness.

Navigating the debt relief tax landscape requires understanding complex IRS rules, knowing which exceptions apply to your situation, and proper documentation of your financial circumstances. While forgiven debt can create unexpected tax liability, numerous exceptions exist that might eliminate or reduce what you owe. If you're facing canceled debt or considering debt settlement strategies, don't wait until you receive a 1099-C to start planning. The Law Offices of Darrin T. Mish, P.A. has helped countless clients understand their tax obligations related to debt forgiveness, claim all available exceptions, and resolve unexpected tax bills resulting from canceled debts. With over 32 years of experience in tax law, we offer free consultations to help you navigate these challenging situations and find the best path forward.