There's the version of tax resolution the late-night commercials sell you. Then there's how it actually works. I'm Darrin Mish, a Tampa tax attorney. I've spent 32 years on the inside of these cases. Here's the real version.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

You check the mail and there it is. A tax letter from the IRS. Envelope looks official. Your stomach drops.

That reaction is normal, but panic doesn't help. The IRS sends out roughly 150 million letters every year. Most don't signal catastrophe – they signal something specific the agency needs from you, usually something you can handle if you move quickly.

The problem is that most people don't move quickly. They freeze. They shove the letter in a drawer and hope it disappears. It won't.

What a Tax Letter Actually Means

The IRS doesn't call you. They don't email. They send paper.

That's their protocol, and it's been that way for decades. When the IRS sends you a letter or notice, they're following a bureaucratic process, not making a personal judgment about you.

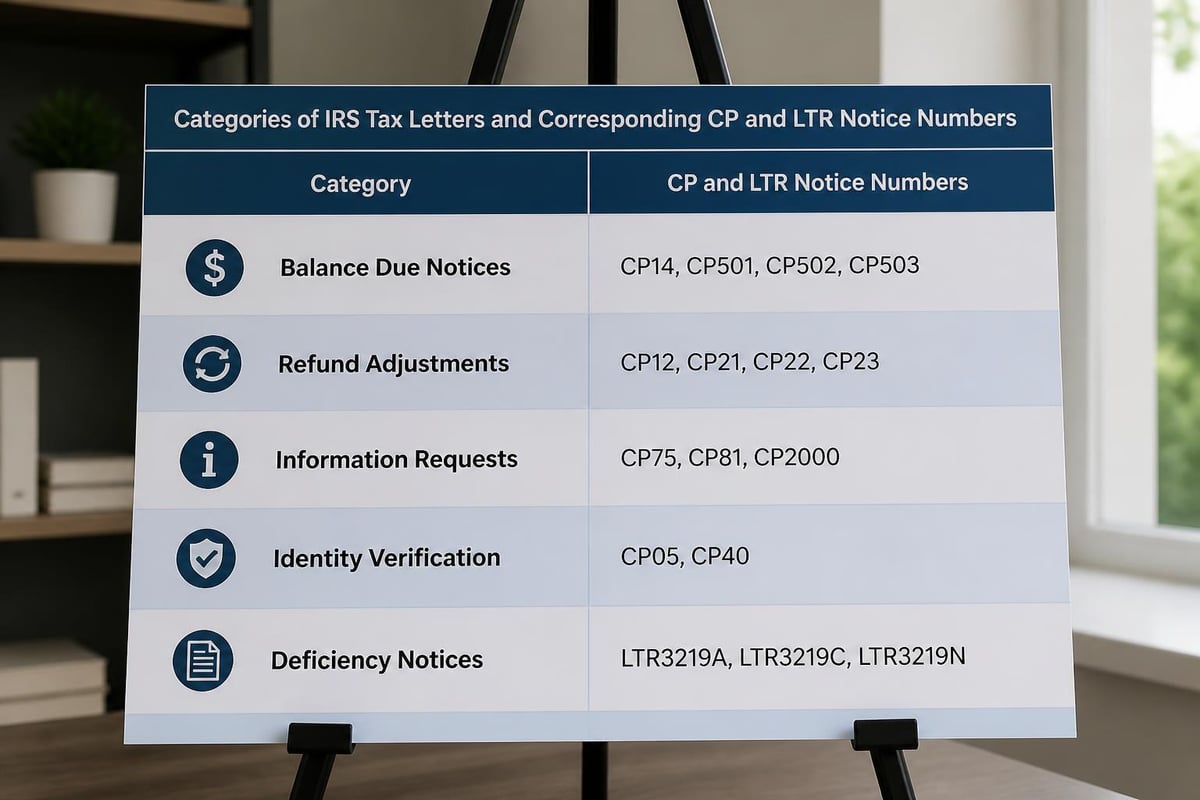

Most tax letters fall into a few categories:

- Balance due notices – You owe money and they want payment

- Refund adjustments – They changed your refund amount

- Information requests – They need documentation or clarification

- Identity verification – They're checking if the return is really yours

- Notice of deficiency – They're proposing changes to your tax liability

The letter will always have a notice number in the upper right corner. That number tells you exactly what type of correspondence it is and what the IRS expects from you.

You have deadlines. Those deadlines aren't suggestions.

The Most Common Tax Letter You'll Get

The CP2000 is the one I see most often. It's not technically a bill – it's a "proposed assessment."

The IRS received income information from third parties (employers, banks, investment firms) that doesn't match what you reported on your return. They're asking you to explain the difference or agree to pay what they think you owe.

Here's what makes CP2000 letters tricky: they’re wrong more often than you’d think. The IRS matching system is automated. It doesn't understand context.

Maybe you reported self-employment income on Schedule C, but the 1099 looks like unreported income to their computer. Maybe you sold stock and reported the correct gain, but the IRS only sees the gross proceeds and thinks you didn't report it at all.

You have 30 days to respond. Use them.

How to Respond to a CP2000

Don't agree to pay unless you actually owe. That sounds obvious, but people do it all the time out of fear or confusion.

- Read the entire letter – including the fine print and attachments

- Compare it to your actual return – line by line if necessary

- Gather your documentation – W-2s, 1099s, receipts, bank statements

- Determine if the IRS is correct – partially, fully, or not at all

- Respond in writing – using the response form included with the letter

If the IRS is right, you can agree and arrange payment. If they're wrong, you'll need to explain why and provide proof. If they're partially right, you can agree to part and dispute the rest.

The worst thing you can do is nothing. Silence equals agreement in the IRS's eyes.

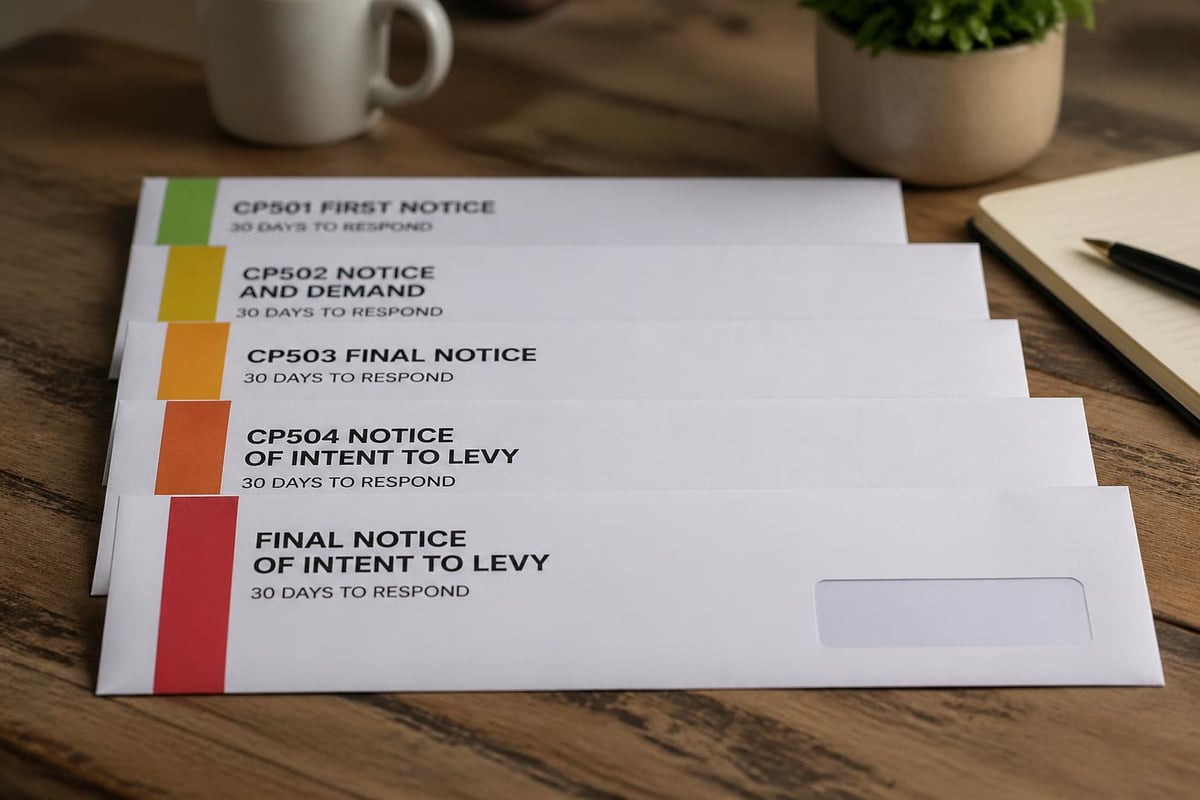

Tax Letters About Money You Owe

If you already know you owe and haven't paid, the IRS will send a sequence of letters with escalating urgency.

| Notice Type | What It Means | Deadline |

|---|---|---|

| CP501 | First reminder of balance due | 21 days |

| CP503 | Second reminder, more urgent | 21 days |

| CP504 | Final notice before levy action | 30 days |

| LTR1058 | Intent to levy specific assets | 30 days |

| Letter 11 | Final notice of intent to levy | 30 days |

Each tax letter gives you a window to act. Once that window closes, the IRS moves to enforcement.

Enforcement means tax liens on your property, wage garnishments, and bank levies. Those aren't threats – they're standard collection tools the IRS uses daily.

Your Options When You Owe

You don't have to pay in full immediately. The IRS has programs specifically for people who can't.

Installment agreements let you pay over time. If you owe less than $50,000, you can often set one up online without talking to anyone.

Offer in compromise lets you settle for less than you owe, but only if you genuinely can't pay the full amount from your assets and income.

Currently not collectible status pauses collection if you literally can't afford both basic living expenses and any tax payment. It's temporary, but it's real relief.

Penalty abatement can eliminate penalties (not the underlying tax) if you have reasonable cause or qualify for first-time abatement.

The key is responding to the tax letter before the IRS decides for you. Once they file a lien or levy your bank account, your options shrink and your costs go up.

When the IRS Questions Your Return

Sometimes the tax letter isn't about money you owe. It's about information the IRS wants to verify.

They might ask for proof of income, documentation for deductions, or clarification about credits you claimed. This often happens with:

- Earned Income Tax Credit – requires proof of qualifying children and income

- Education credits – requires Form 1098-T and proof of expenses

- Business expenses – requires receipts, mileage logs, and contemporaneous records

- Charitable contributions – requires acknowledgment letters for donations over $250

The IRS isn't accusing you of fraud. They're verifying. But if you don't respond with adequate documentation within the deadline, they'll disallow whatever they questioned and send you a bill.

What "Adequate Documentation" Actually Means

The IRS has specific rules about what counts as proof. Your word isn't enough.

For business expenses, they want receipts showing the amount, date, vendor, and business purpose. A credit card statement alone won't cut it for most expenses.

For charitable deductions over $250, you need a written acknowledgment from the charity. Your bank statement showing the donation isn't sufficient under tax law.

For education credits, the Form 1098-T from the school is just the starting point. You also need proof you actually paid the expenses and that they qualify.

If you don't have the documentation, don't make it up. That's fraud. Instead, respond honestly and be prepared for the deduction or credit to be disallowed.

The Tax Letters That Signal Serious Problems

Some letters mean you're past the "friendly reminder" stage and into legal territory.

A Notice of Deficiency (also called a 90-day letter) is a formal proposal to assess additional tax. You have 90 days to petition the U.S. Tax Court if you disagree. Miss that deadline and the assessment becomes final – no appeal, no second chance.

A Notice of Federal Tax Lien means the IRS has already filed a public claim against your property. It's not a seizure, but it wrecks your credit and makes selling or refinancing property nearly impossible until you resolve the underlying tax debt.

A Notice of Levy means the IRS is about to (or already has) seized specific assets. Bank accounts, wages, Social Security benefits, contractor payments – all fair game.

If you get any of these, you're well past the DIY stage. These require immediate professional response.

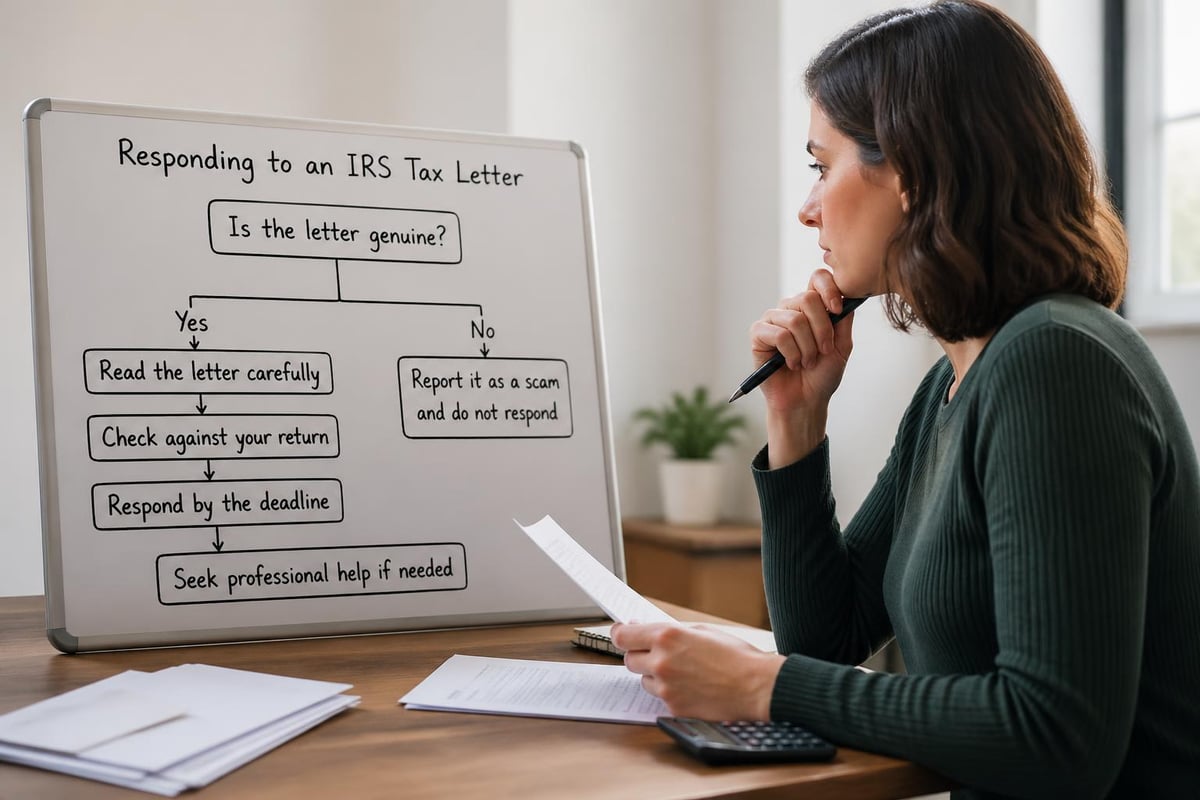

The Do's and Don'ts When You Get a Tax Letter

The IRS publishes guidance on how to handle their correspondence. Most people don't follow it.

Do:

- Open the letter immediately

- Read every word, including the back pages and fine print

- Note the deadline and respond before it expires

- Keep the original letter and all documentation

- Compare the letter's information to your actual tax return

- Respond in writing if you disagree

- Call the IRS only if the letter specifically instructs you to

Don't:

- Ignore the letter or assume it will go away

- Panic and agree to pay without verifying the IRS is correct

- Call a phone number you found online instead of the one on the letter

- Respond to emails or text messages claiming to be from the IRS (they're scams)

- Miss the deadline thinking you can explain later

- Throw away the letter before making a copy

The IRS gives you a specific response window for a reason. They process millions of cases. If you don't respond on time, their system moves forward without you.

When You Should Get Professional Help

Not every tax letter requires a lawyer. But some do, and waiting too long can cost you.

You should get help when:

- The amount in dispute is more than $10,000

- You received a Notice of Deficiency or statutory notice

- The IRS is proposing fraud penalties

- You're facing criminal investigation

- You've already missed deadlines and received multiple letters

- You have unfiled tax returns from previous years

- The IRS is threatening or has already started collection action

Tax attorneys can do things you can't. We can negotiate directly with IRS revenue officers, file for penalty abatement with legal arguments, represent you in Tax Court, and structure settlements through offers in compromise.

We also know when the IRS is bluffing and when they're serious. That judgment comes from handling hundreds of these cases.

If you're reading the tax letter and you don't understand what they're asking or why they're asking it, that's a sign you need help. The IRS writes these letters in bureaucratic code. Responding incorrectly can make things worse.

What Happens If You Don't Respond

The IRS doesn't forget. They don't get bored and move on to someone else.

If you don't respond to a tax letter, here's the typical progression:

- They send another letter – usually more urgent

- They assess the tax or penalty – it becomes an official debt

- They file a Notice of Federal Tax Lien – public record, damages credit

- They send a Final Notice of Intent to Levy – last warning before seizure

- They levy your assets – bank accounts, wages, Social Security, property

This process can take months or years depending on the type of tax letter and how much you owe. But it's not a question of if – it's when.

The IRS has a 10-year statute of limitations to collect, but that clock pauses every time you enter a payment plan, request a collection due process hearing, or file for bankruptcy. In practice, they have longer than 10 years.

Scam Letters Versus Real IRS Correspondence

Real IRS letters arrive by U.S. Mail. They have official letterhead. They reference your specific tax year and notice number. They explain what they want and give you a deadline.

Scam letters often:

- Demand immediate payment by wire transfer, gift card, or cryptocurrency

- Threaten arrest or deportation

- Use aggressive or threatening language

- Contain spelling or grammatical errors

- Arrive via email or text message (the IRS doesn't initiate contact this way)

If you're not sure whether a tax letter is legitimate, call the IRS directly using the phone number from their official website – not the number on the letter you received. They can verify whether they actually sent it.

Scammers have gotten sophisticated. They copy IRS formatting, use official-sounding language, and spoof caller ID. When in doubt, verify independently.

Understanding Your Rights as a Taxpayer

Every tax letter should include a section about your rights. Most people skip it.

You have the right to:

- Professional and courteous treatment

- Privacy and confidentiality

- Understand why the IRS is asking for information or payment

- Representation by an attorney, CPA, or enrolled agent

- Appeal IRS decisions to an independent office

- Challenge the IRS position in Tax Court

- Relief from certain penalties under specific circumstances

- Understanding the notices you receive

These aren't theoretical. You can actually exercise these rights, but you have to know they exist and act within the deadlines the tax letter provides.

The IRS doesn't make this easy. Their letters are dense, legalistic, and often unclear. That's by design – it's a bureaucracy built for processing millions of cases efficiently, not for customer service.

What the Notice Number Tells You

Every tax letter has a notice number in the upper right corner, usually starting with "CP" or "LTR."

Here's what some common ones mean:

| Notice Number | Purpose | Urgency Level |

|---|---|---|

| CP14 | First notice of balance due | Low |

| CP501 | Reminder notice | Medium |

| CP504 | Final notice before levy | High |

| CP2000 | Proposed assessment based on information mismatch | Medium |

| CP3219A | Notice of Deficiency (90-day letter) | Critical |

| LTR1058 | Intent to levy state tax refund | High |

| LTR11 | Final notice of intent to levy | Critical |

The IRS sends different letters for different purposes. Understanding which one you received tells you how quickly you need to act and what options you have.

Some letters are informational only. Others start a clock that ends with enforced collection if you don't respond.

How to Prevent Future Tax Letters

The IRS sends letters when something doesn't match their records or when you owe money. You can reduce the chances of getting them by:

- Filing your returns on time every year (even if you can't pay)

- Reporting all income that appears on information returns (W-2s, 1099s)

- Keeping detailed records of deductions and credits

- Making estimated tax payments if you're self-employed

- Responding to any IRS letter immediately, even if just to acknowledge receipt

- Setting up a payment plan if you can't pay in full

The people who get the most IRS letters are the ones who don't file, don't report income, or ignore previous correspondence. The system is designed to escalate until you engage.

If you file accurately and pay what you owe (or set up a payment plan when you can't), the tax letters stop.

When the Letter Is About Someone Else's Tax Debt

Sometimes you'll receive a tax letter about a spouse's debt, a business partner's liability, or even a deceased person's taxes.

Innocent spouse relief applies when your spouse or former spouse understated tax on a joint return and you didn't know about it. The IRS can't automatically collect from you, but you have to request relief within specific timeframes.

Trust fund recovery penalty letters target business owners and officers personally for unpaid payroll taxes. If your business failed to pay employee withholding to the IRS, they can come after you individually.

Estate tax letters go to executors and personal representatives. If you're handling someone's estate and the IRS sends correspondence, you need to respond even if you're not personally liable for the debt.

These situations are complex. The tax letter will reference specific Internal Revenue Code sections and often requires legal analysis to determine your actual liability versus what the IRS claims.

What Happens After You Respond

You send your response. Then what?

The IRS will acknowledge receipt, usually within a few weeks. Then they'll review your response and either:

- Agree with you – they'll send a closure letter or adjust your account

- Partially agree – they'll revise the proposed assessment and send an updated notice

- Disagree – they'll send another letter explaining why and what happens next

If they disagree, you usually have appeal rights. The tax letter will explain how to request an appeal and what deadline applies.

Appeals go to the IRS Independent Office of Appeals, a separate division that's supposed to be neutral. They'll review your case, consider the facts and law, and make a determination.

If you disagree with Appeals, your next step is usually Tax Court. That requires filing a petition within specific deadlines and following formal procedures.

The process can take months or even years depending on complexity and how backed up the IRS is. During that time, interest continues to accrue on any unpaid tax.

The Bottom Line on Tax Letters

A tax letter isn't a catastrophe. It's information.

The IRS is telling you what they think is wrong and giving you a chance to respond. Most problems can be resolved if you act within the deadlines and respond appropriately.

What turns a routine tax letter into a serious problem is ignoring it, missing deadlines, or responding incorrectly. The IRS assumes silence means agreement. They move forward whether you participate or not.

If the letter is simple and the amount small, handle it yourself. If it's complex, involves large amounts, or threatens collection action, get professional help. The cost of hiring someone now is almost always less than the cost of fixing mistakes later.

The key to handling any tax letter is understanding what it's asking and responding before the deadline expires. The IRS sends millions of these letters annually, but they all follow predictable patterns once you know what to look for. If you've received IRS correspondence that you don't understand or don't know how to handle, the Law Offices of Darrin T. Mish, P.A. offers free consultations to review your situation and explain your options. We've been resolving IRS problems for over three decades, and we can help you determine whether you need representation or can handle the response yourself.