I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Trying to figure out how to pay my tax IRS obligations can feel overwhelming, especially when you're juggling deadlines, payment methods, and the fear of penalties. Whether you owe taxes from your 2025 return or need to make estimated payments for 2026, understanding your options is the first step toward staying compliant and avoiding unnecessary stress. The IRS offers multiple payment methods designed to accommodate different financial situations, but knowing which one works best for your circumstances requires a bit of guidance. Let's walk through everything you need to know about paying your federal taxes efficiently and strategically.

Understanding Your IRS Tax Payment Obligations

Before you can effectively pay my tax IRS balance, you need to understand what you actually owe. Your tax obligation comes from several potential sources: income tax on your wages or self-employment income, capital gains from investments, or even taxes on cryptocurrency transactions. The IRS calculates your liability based on your adjusted gross income, deductions, and credits.

When you file your tax return, you'll see whether you owe additional taxes beyond what was withheld from your paychecks throughout the year. Self-employed individuals and those with investment income often need to make quarterly estimated tax payments to avoid underpayment penalties. According to the Internal Revenue Code Section 6654, you may face penalties if you don't pay enough tax during the year through withholding or estimated payments.

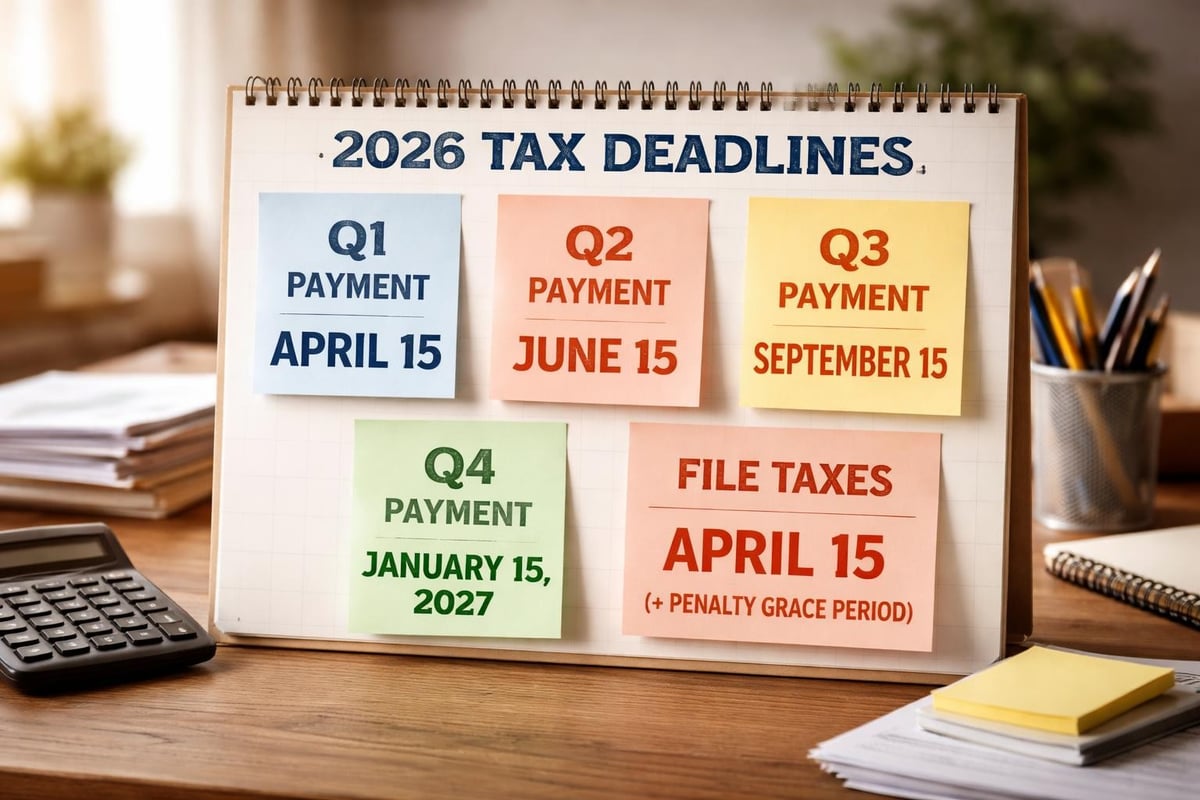

Key Tax Payment Deadlines for 2026

Timing matters when it comes to federal taxes. Missing deadlines triggers interest charges and penalties that compound your tax debt quickly. Here are the critical dates you need to mark on your calendar:

- April 15, 2026: Deadline for filing your 2025 tax return and paying any balance due

- April 15, 2026: First quarter 2026 estimated tax payment

- June 16, 2026: Second quarter 2026 estimated tax payment

- September 15, 2026: Third quarter 2026 estimated tax payment

- January 15, 2027: Fourth quarter 2026 estimated tax payment

If April 15 falls on a weekend or holiday, the deadline typically shifts to the next business day. You can find current tax filing and payment deadlines to ensure you're working with the most up-to-date information. For those who need more time to prepare their returns, understanding how tax extensions work is crucial, though remember that extensions give you more time to file, not more time to pay.

Electronic Payment Methods to Pay My Tax IRS Balance

The IRS strongly encourages electronic payments because they're faster, more secure, and provide immediate confirmation. When you're ready to pay my tax IRS debt, you have several digital options at your disposal.

IRS Direct Pay: The Free and Simple Choice

IRS Direct Pay is the most straightforward way to pay your taxes directly from your checking or savings account. There are no fees, no registration requirements, and you get instant confirmation. You can schedule payments up to 365 days in advance, which is perfect for planning around cash flow.

To use Direct Pay, you'll need your Social Security number or Individual Taxpayer Identification Number, your filing status, and the exact refund amount from your most recent tax return (if applicable). The system walks you through a verification process to confirm your identity, then you authorize the payment from your bank account.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is ideal if you make frequent tax payments or prefer having a dedicated account for managing your obligations. While it requires enrollment (which takes about a week for the PIN to arrive by mail), EFTPS offers robust scheduling features and a complete payment history.

Business owners paying payroll taxes often use EFTPS because it handles both individual and business tax payments. You can schedule payments up to 365 days in advance and receive email confirmations for every transaction.

Credit and Debit Card Payments

Paying by card offers convenience and the potential to earn rewards points, but you'll pay processing fees ranging from 1.85% to 1.98% of your payment amount. The IRS partners with several approved payment processors who charge these fees directly.

Here's how the payment processors compare:

| Processor | Debit Card Fee | Credit Card Fee | Convenience |

|---|---|---|---|

| PayUSAtax | $2.20 minimum | 1.85% | Online/Phone |

| Pay1040 | $2.50 minimum | 1.87% | Online/Phone |

| ACI Payments | $2.20 minimum | 1.98% | Online/Phone |

If you have a rewards credit card that earns more than 2% cash back, you might break even or come out slightly ahead, but this strategy only makes sense if you can pay off the balance immediately to avoid interest charges.

Traditional Payment Methods That Still Work

Not everyone wants to pay my tax IRS obligations electronically. Traditional payment methods remain available, though they take longer to process.

Paying by Check or Money Order

You can mail a check or money order to the IRS along with your tax return or with Form 1040-V (Payment Voucher). Make your payment out to "United States Treasury" and include your Social Security number, the tax year, and the form number on the memo line.

Important tips for check payments:

- Mail payments well before the deadline to account for processing time

- Use certified mail with return receipt if sending a large payment

- Keep copies of your check and any vouchers for your records

- Never send cash through the mail

The mailing address depends on where you live and whether you're including a payment with your return, so check the current IRS instructions for your specific situation.

In-Person Payment Options

You can pay cash at participating retail partners through the IRS's PayNearMe program. After registering online and receiving a confirmation code, you can pay up to $1,000 per day at locations like 7-Eleven, Family Dollar, and CVS Pharmacy. This option works well if you don't have a bank account or prefer cash transactions.

What to Do When You Can't Pay My Tax IRS Bill in Full

Owing more than you can pay right now doesn't mean you're out of options. The IRS offers several relief programs designed to help taxpayers manage their obligations without facing immediate collection action.

Setting Up an Installment Agreement

An installment agreement lets you pay your tax debt over time in monthly payments. If you owe $50,000 or less in combined tax, penalties, and interest, you can apply online for a streamlined installment agreement. You can learn more about setting up a payment plan with the IRS through a structured process that many taxpayers successfully navigate.

Types of installment agreements:

- Short-term payment plan (up to 180 days): No setup fee if you owe less than $100,000

- Long-term payment plan (more than 180 days): Setup fees range from $31 to $225 depending on how you apply and pay

- Partial payment installment agreement: For those who can't pay the full amount within the collection statute of limitations

The IRS charges interest and penalties on unpaid balances even with an installment agreement in place, but it's far better than facing enforced collection actions like wage garnishments or bank levies.

Offer in Compromise: Settling for Less

An Offer in Compromise allows qualified taxpayers to settle their tax debt for less than the full amount owed. However, the IRS only accepts offers when it's unlikely they'll collect the full debt within the statutory period, or collecting the full amount would create economic hardship.

The application process is complex and requires detailed financial disclosure. You'll need to demonstrate that the amount you're offering represents the most the IRS can reasonably expect to collect. Understanding offer in compromise options and requirements can help you determine if this path makes sense for your situation.

Currently Not Collectible Status

If you're experiencing genuine financial hardship where paying anything toward your tax debt would prevent you from meeting basic living expenses, you may qualify for Currently Not Collectible (CNC) status. This temporarily suspends IRS collection activities, though interest and penalties continue accruing.

The IRS requires comprehensive financial documentation to prove hardship. They'll review your income, expenses, assets, and overall ability to pay. While in CNC status, the IRS may file a tax lien to protect its interest, but they won't actively pursue collection through levies or garnishments.

Avoiding Penalties and Interest When You Pay My Tax IRS Obligations

The IRS assesses penalties for various tax violations, but the most common ones relate to payment timing. Understanding these penalties helps you make strategic decisions about when and how to pay.

Failure to Pay Penalty

If you don't pay my tax IRS balance by the deadline, you'll face a failure-to-pay penalty of 0.5% of the unpaid taxes per month, up to a maximum of 25%. This penalty applies even if you file on time but don't pay the full amount owed.

However, if you request an installment agreement before the due date, the IRS reduces the penalty to 0.25% per month while the agreement is in effect. This is one reason why setting up a payment plan proactively makes financial sense.

Interest Charges Explained

Beyond penalties, the IRS charges interest on unpaid tax balances. The interest rate is the federal short-term rate plus 3%, and it compounds daily. As of the first quarter of 2026, the interest rate for individual underpayments is 8% annually, though this rate adjusts quarterly.

Interest charges aren't negotiable, but you can minimize them by paying as much as possible as early as possible. Even partial payments reduce the balance on which interest compounds.

Penalty Abatement Options

If you have a clean compliance history, you may qualify for first-time penalty abatement. This administrative waiver can remove failure-to-file and failure-to-pay penalties if you meet specific criteria. You can explore IRS penalty abatement strategies to understand whether you qualify for relief.

The IRS also grants penalty relief for reasonable cause, such as natural disasters, serious illness, or other circumstances beyond your control that prevented timely payment. You'll need to document your situation and explain why it was impossible to meet your tax obligations on time.

Smart Strategies for Managing Estimated Tax Payments

If you're self-employed, own a business, or have significant investment income, you need to make quarterly estimated payments. Knowing when estimated tax payments are due helps you avoid underpayment penalties and cash flow crunches.

Calculating How Much to Pay

Under the safe harbor rules, you'll avoid underpayment penalties if you pay either:

- At least 90% of the tax shown on your current year's return, or

- 100% of the tax shown on your prior year's return (110% if your adjusted gross income was over $150,000)

Many taxpayers use the prior year safe harbor because it's easier to calculate and provides certainty. If your income varies significantly throughout the year, you might benefit from the annualized income installment method, which adjusts each payment based on when you actually earned the income.

Using Direct Pay for Quarterly Payments

When you need to pay my tax IRS estimated taxes, Direct Pay offers the convenience of scheduling all four quarterly payments at once. Set up your payments in January, and you won't have to worry about missing deadlines throughout the year.

This approach works particularly well if you have consistent income and know your approximate tax liability. Just remember to adjust your scheduled payments if your income changes significantly during the year.

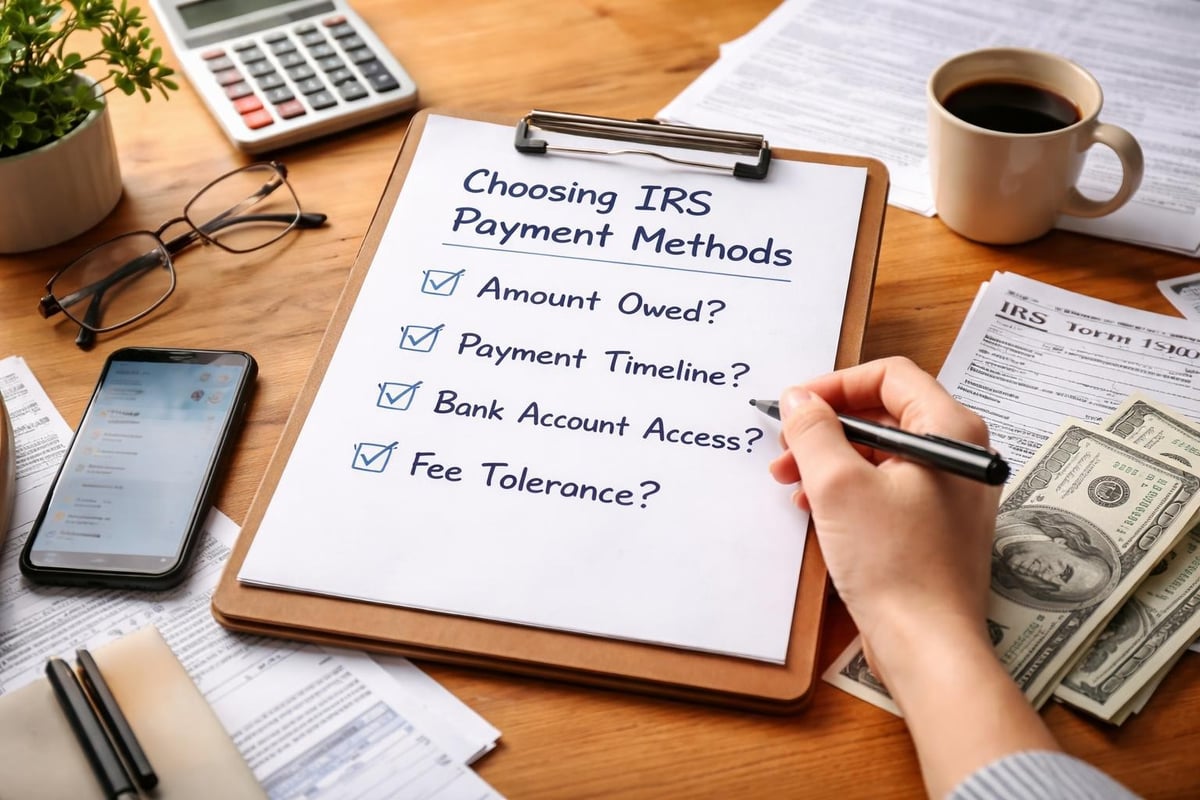

Exploring All Your IRS Payment Options

The IRS provides comprehensive information about payment options that covers both electronic and traditional methods. For a detailed comparison of different payment methods including fees and processing times, the IRS payment options overview breaks down each choice clearly.

When evaluating which method to use when you pay my tax IRS balance, consider these factors:

| Factor | Best Option | Why |

|---|---|---|

| No fees | Direct Pay / EFTPS | Completely free electronic transfers |

| Speed | Direct Pay | Same-day processing if submitted early |

| Rewards points | Credit card | Earn rewards (if fee is less than rewards value) |

| No bank account | PayNearMe cash | Pay at retail locations |

| Schedule ahead | EFTPS / Direct Pay | Schedule up to 365 days in advance |

| Payment tracking | EFTPS | Comprehensive payment history and confirmations |

For ongoing tax obligations, establishing a relationship with a qualified tax professional can help you navigate complex situations. The Law Offices of Darrin T. Mish, P.A. specializes in helping taxpayers understand their payment options and negotiate with the IRS when standard payment arrangements don't fit their circumstances.

Protecting Yourself from IRS Collection Actions

When you can't immediately pay my tax IRS debt, the agency has powerful collection tools at its disposal. Understanding these mechanisms helps you avoid them through proactive communication and payment arrangements.

Wage Garnishment and Bank Levies

If you ignore tax debt, the IRS can garnish your wages, taking a significant portion of each paycheck until your debt is satisfied. They can also levy your bank accounts, freezing funds and seizing them to apply toward your balance. These wage garnishment actions are legally enforceable without a court judgment, making them particularly powerful collection tools.

The good news? The IRS must follow specific procedures before implementing these actions. You'll receive multiple notices giving you opportunities to pay my tax IRS balance or arrange alternatives. If you receive a Final Notice of Intent to Levy, you have 30 days to respond before the levy takes effect.

Tax Liens and Their Long-Term Impact

A federal tax lien is the government's legal claim against your property when you neglect or fail to pay a tax debt. The lien attaches to all your current and future assets, including real estate, vehicles, and financial accounts. Unlike a levy, which seizes property, a lien simply establishes the IRS's interest.

Tax liens severely damage your credit and make it difficult to sell assets or obtain financing. While the IRS generally files liens when you owe $10,000 or more, they have discretion to file for smaller amounts in certain circumstances. Understanding how tax liens work can help you take action before one is filed against you.

Working with Tax Professionals on Payment Issues

Complex tax situations often benefit from professional guidance. When you owe substantial amounts or face collection actions, a tax attorney can negotiate on your behalf and protect your rights throughout the process.

When to Seek Professional Help

Consider consulting a tax professional if you:

- Owe more than $25,000 in back taxes

- Face wage garnishment or bank levies

- Received multiple IRS notices you don't understand

- Need to negotiate an offer in compromise

- Have unfiled tax returns complicating your payment situation

- Experience financial hardship affecting your ability to pay

Tax attorneys understand the intricacies of IRS procedures and can often achieve better outcomes than taxpayers negotiating alone. They can also handle all communications with the IRS, reducing your stress and ensuring nothing falls through the cracks.

Understanding Your Rights as a Taxpayer

The Taxpayer Bill of Rights guarantees your right to be informed, to quality service, to pay no more than the correct amount of tax, to challenge the IRS's position, and to a fair and just tax system. When working to pay my tax IRS obligations, you have the right to representation and to appeal IRS decisions.

If you disagree with a payment demand or believe the IRS made an error in calculating your liability, you can request an appeals conference. For issues involving collection actions, you may request a Collection Due Process hearing, which temporarily suspends collection while your case is reviewed.

Staying Current After Resolving Tax Debt

Once you've addressed your outstanding balance, staying compliant prevents future problems. This means adjusting your withholding if you're an employee or making accurate estimated payments if you're self-employed.

Adjusting Your Tax Withholding

If you owed significantly when you filed, your withholding likely isn't keeping pace with your actual tax liability. Submit a new Form W-4 to your employer to increase withholding from each paycheck. The IRS provides a tax withholding estimator tool that helps you calculate the right amount based on your specific situation.

For those with multiple income sources, including gig economy work or investment income, you might need both withholding adjustments and estimated payments to stay current.

Building a Tax Payment Strategy

Create a systematic approach to managing your tax obligations:

- Track your income monthly to estimate your annual tax liability

- Set aside money regularly in a dedicated tax savings account

- Review your situation quarterly to ensure you're on track

- Make estimated payments on time using scheduled electronic payments

- File accurately and on time even if you can't pay the full balance

This proactive approach prevents the stress and financial strain of owing large amounts unexpectedly. Many taxpayers find that automating tax savings-treating it like any other monthly bill-makes compliance easier and less painful.

Understanding how to pay my tax IRS obligations efficiently protects you from penalties, interest, and collection actions while maintaining your financial stability. Whether you choose electronic payments for convenience, set up an installment agreement to manage cash flow, or explore relief options during hardship, taking action is always better than ignoring the problem. If you're facing complex tax debt situations or need guidance navigating IRS payment options, the Law Offices of Darrin T. Mish, P.A. offers over 32 years of experience helping taxpayers worldwide resolve their IRS challenges with personalized legal solutions and free consultations to get you started on the path to resolution.