I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Have you ever opened your mailbox to find an IRS notice about unpaid taxes and felt your stomach drop? You're not alone. Millions of Americans face this situation every year, and the stress can feel overwhelming. But here's the thing: IRS unpaid taxes don't have to spiral into a financial nightmare if you understand your options and act quickly. Let's walk through everything you need to know about dealing with tax debt, the consequences of ignoring it, and the practical solutions available to get you back on solid ground.

What Exactly Are IRS Unpaid Taxes?

When we talk about IRS unpaid taxes, we're referring to any tax liability you owe to the federal government that hasn't been paid by the deadline. This could be from your annual tax return, quarterly estimated payments, or even penalties and interest that have accumulated over time.

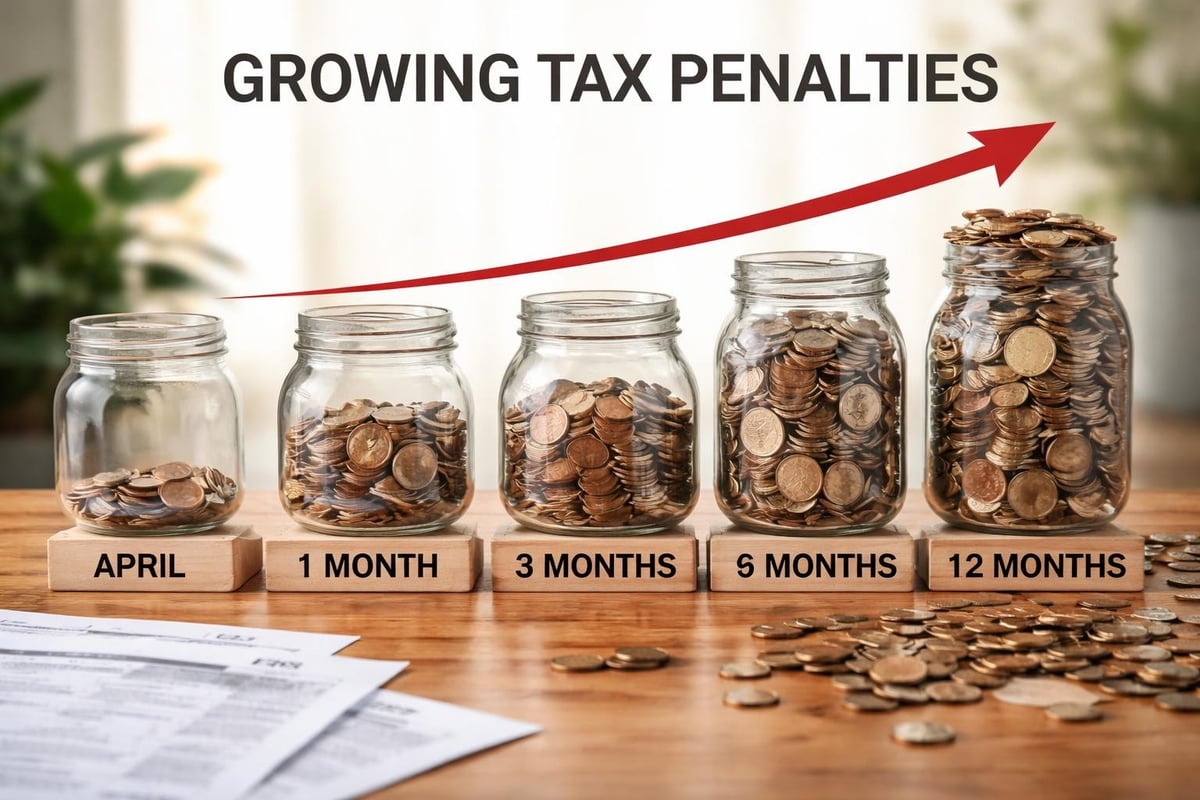

The IRS doesn't mess around when it comes to collecting what's owed. Once Tax Day passes (usually April 15th), any unpaid balance starts accumulating penalties and interest immediately. Think of it like a snowball rolling downhill, getting bigger as it goes.

The Two Types of Tax Penalties You Need to Know

Understanding how the IRS calculates what you owe is crucial. There are two main penalties that apply to unpaid taxes:

- Failure-to-file penalty: This hits you when you don't submit your tax return on time

- Failure-to-pay penalty: This applies when you file but don't pay the full amount owed

The failure-to-pay penalty typically runs 0.5% of your unpaid taxes per month, up to a maximum of 25%. That might not sound like much, but it adds up fast when combined with interest.

Interest compounds daily based on the federal short-term rate plus 3%. In 2026, with fluctuating interest rates, this can significantly increase your total debt over time.

Why Do People End Up With IRS Unpaid Taxes?

Life happens, right? I've worked with countless clients over the years, and the reasons for unpaid taxes are as varied as the people themselves.

Common Scenarios Leading to Tax Debt

Sometimes it's a simple miscalculation. You thought you'd get a refund, but the numbers didn't work out that way. Other times, it's more complex:

- Job changes or income fluctuations that mess up your withholding

- Self-employment income where you didn't set aside enough for taxes

- Major life events like divorce, medical emergencies, or job loss

- Investment gains you didn't anticipate or plan for

- Missing deductions or credits you thought you qualified for

Whatever the reason, the IRS doesn't really care about why you owe. They just want their money. But understanding your situation helps determine the best path forward for dealing with IRS delinquent taxes.

The Real Consequences of Ignoring Unpaid Taxes

Let me be straight with you: ignoring IRS unpaid taxes is one of the worst financial decisions you can make. The consequences escalate quickly and can seriously impact your life.

What Happens When You Don't Pay

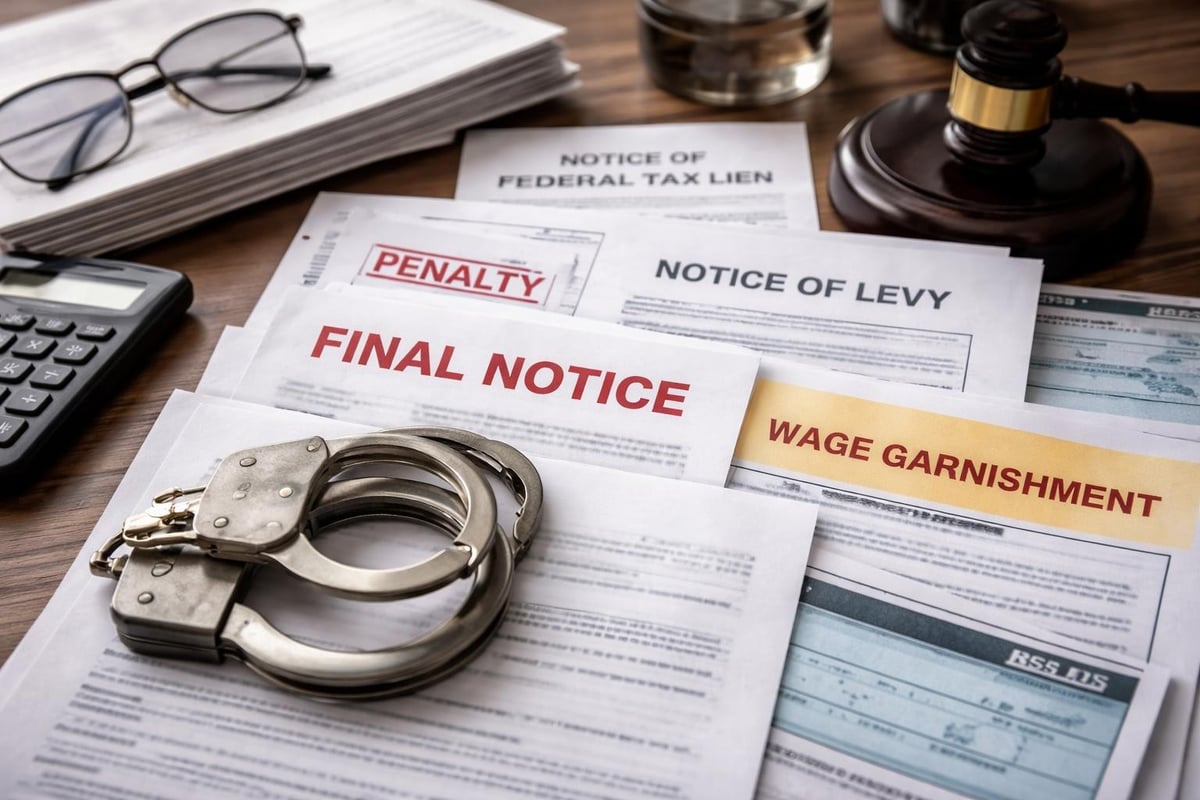

The IRS has extraordinary collection powers that most creditors can only dream about. Here's what they can do:

| Collection Action | Description | Timeline |

|---|---|---|

| Tax Lien | Public claim against your property | After 10 days of final notice |

| Wage Garnishment | Direct deduction from your paycheck | After multiple notices |

| Bank Levy | Seizure of funds from your accounts | After notice and demand |

| Asset Seizure | Taking physical property to sell | Final collection step |

A tax lien is particularly damaging because it becomes public record. This means it shows up on your credit report, making it nearly impossible to get a mortgage, car loan, or even some jobs. I've seen clients lose job opportunities because employers ran credit checks and saw tax liens.

Wage garnishments can take up to 25% of your disposable income, leaving you scrambling to pay basic bills. And unlike most creditors, the IRS doesn't need to sue you first. They have the legal authority to take your wages with administrative action alone.

The Emotional Toll Nobody Talks About

Beyond the financial impact, the stress of dealing with IRS unpaid taxes takes a real emotional toll. The constant worry, the unopened mail piling up, the fear of what might happen next-it affects your sleep, your relationships, and your overall wellbeing.

But here's the good news: you have more options than you think.

Your Payment Options for Resolving Tax Debt

The IRS actually wants to work with you. Seriously. They'd rather collect something than nothing, which is why they've created various programs to help taxpayers manage their debt.

Immediate Payment Methods

If you can pay your full tax bill right now, that's always your best option. You'll stop the interest and penalties from growing, and you'll be done with the whole mess. The IRS accepts several payment methods:

- Direct Pay from your bank account (free)

- Debit or credit card (convenience fees apply)

- Check or money order by mail

- Wire transfer for large amounts

- Same-day payment through your tax professional

But what if you can't pay everything at once? That's where things get interesting.

Installment Agreements: Breaking It Down

An installment agreement lets you pay your IRS unpaid taxes over time. Think of it like a payment plan for your tax debt. There are different types depending on how much you owe:

Short-term payment plans (up to 180 days) don't have a setup fee. You just need to pay the full balance within six months. This works great if you're expecting a bonus, commission, or other lump sum that's coming soon.

Long-term payment plans spread payments over more time, potentially up to 72 months. These do have setup fees, though they're waived or reduced if you set up automatic payments from your bank account. For balances under $50,000, you can often get approved online through the IRS website without extensive financial documentation.

The beauty of installment agreements is that they stop most collection actions. Once you're in an approved plan and making payments, the IRS generally won't levy your wages or bank accounts. That peace of mind alone is worth the effort of setting one up.

Offer in Compromise: Settling for Less

Here's where it gets really interesting. An Offer in Compromise lets you settle your tax debt for less than you owe. Sounds too good to be true, right?

It's legitimate, but it's also highly selective. The IRS only accepts offers when they believe they'll collect more this way than through other enforcement actions. You need to prove that paying the full amount would create genuine financial hardship.

The IRS looks at your:

- Reasonable Collection Potential (RCP)-what you could realistically pay

- Current and future income

- Assets and equity

- Monthly expenses (only those they deem necessary)

Most people who apply don't qualify, which is why working with an experienced tax professional is crucial when exploring this option. But for those who do qualify, it can literally save tens of thousands of dollars.

Currently Not Collectible Status: A Temporary Breather

Sometimes you genuinely cannot pay anything toward your IRS unpaid taxes without creating serious financial hardship. Maybe you've lost your job, you're facing medical issues, or you're barely scraping by on Social Security.

The IRS has a status called Currently Not Collectible (CNC) for situations like these. When you're granted CNC status, the IRS temporarily stops all collection activities. They won't garnish your wages, levy your bank account, or seize your assets.

How CNC Status Works

You'll need to prove your financial hardship with detailed documentation:

- Bank statements from the past three months

- Proof of income (or lack thereof)

- Monthly expense documentation

- Asset information

The IRS will verify that paying your tax debt would leave you unable to meet basic living expenses. If approved, they'll essentially pause collections. Your debt doesn't go away, and interest keeps accruing, but you get breathing room to get back on your feet.

There's an important consideration here: the IRS reviews CNC status periodically. If your financial situation improves, they'll restart collection efforts. Also, they might file a tax lien even while you're in CNC status to protect their interest in any future assets.

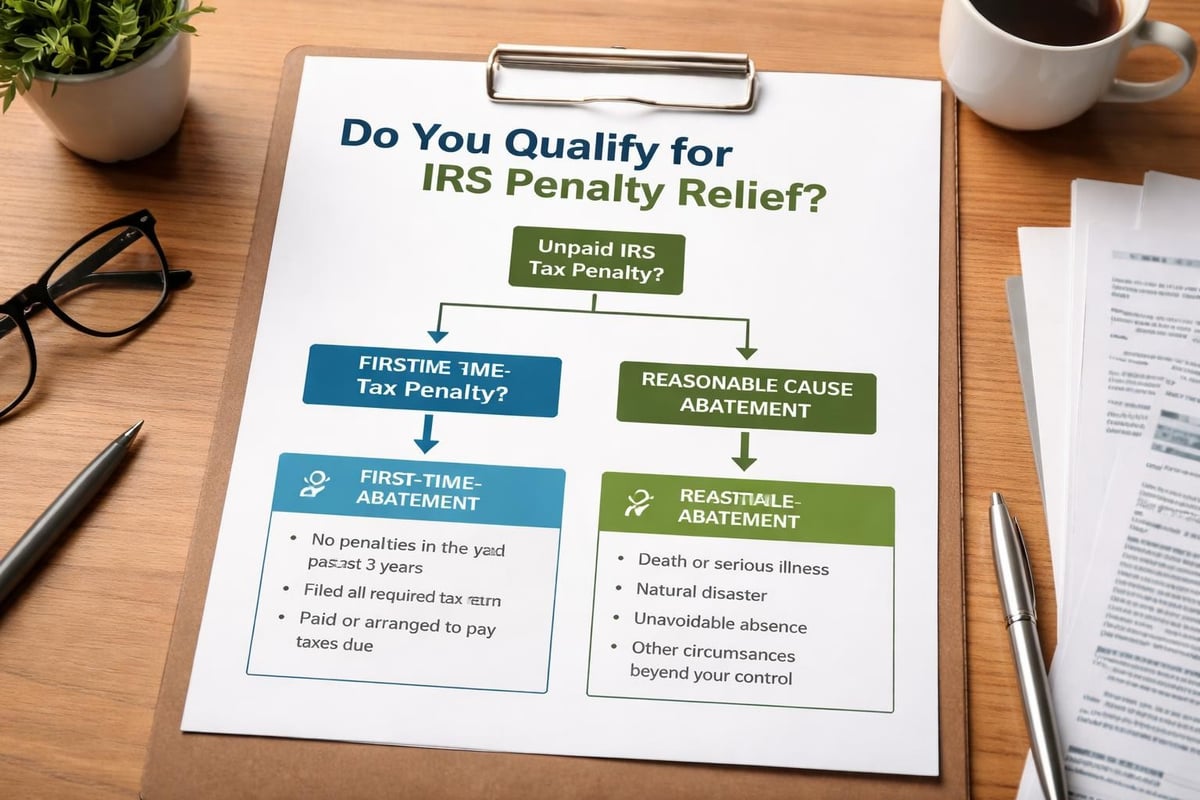

Penalty Abatement: Reducing What You Owe

Did you know you might be able to get penalties removed from your tax bill? Penalty abatement can significantly reduce your IRS unpaid taxes, sometimes by thousands of dollars.

First-Time Penalty Abatement

If you have a clean tax history for the past three years, you might qualify for first-time penalty abatement. This removes failure-to-file and failure-to-pay penalties for a single tax year. You still owe the underlying tax and interest, but eliminating penalties can cut your bill substantially.

The requirements are straightforward:

- You filed (or filed an extension for) all required returns

- You paid or arranged to pay any tax due

- You haven't had penalties in the prior three years

Reasonable Cause Abatement

Even if you don't qualify for first-time abatement, you might get penalties removed based on reasonable cause. This applies when circumstances beyond your control prevented you from meeting your tax obligations.

Examples include:

- Serious illness or death in the family

- Natural disasters

- Inability to obtain records

- Incorrect advice from a tax professional or the IRS itself

You'll need documentation supporting your reasonable cause claim. Medical records, death certificates, insurance claims, and written correspondence can all help your case.

What to Do Right Now If You Owe Unpaid Taxes

Okay, so you have unpaid taxes. What's your first move? Here's a step-by-step approach that works:

Step 1: File Your Return (Even If You Can't Pay)

This is crucial. Filing on time even when you can't pay saves you from the hefty failure-to-file penalty, which is 10 times worse than the failure-to-pay penalty. Get that return submitted by the deadline, or file an extension if you need more time to prepare it properly.

Step 2: Assess Your Full Tax Situation

Pull together all the information you have. How much do you owe? What tax years are involved? Have you received any IRS notices? Understanding the complete picture helps you choose the right solution.

Step 3: Calculate What You Can Realistically Pay

Be honest with yourself here. Look at your monthly income and necessary expenses. What can you afford to pay toward your tax debt? This determines which payment option makes sense for your situation.

Step 4: Contact the IRS or Get Professional Help

You have two paths: handle it yourself or work with a tax professional. For straightforward situations with smaller balances, you might manage on your own using the IRS’s payment assistance programs.

For complex situations-multiple years of unpaid taxes, large balances, existing liens or levies, or if you're considering an Offer in Compromise-professional help becomes invaluable. Tax attorneys understand the nuances of tax law and can negotiate effectively with the IRS on your behalf.

Common Mistakes That Make Things Worse

I've seen people make the same mistakes over and over when dealing with IRS unpaid taxes. Let's make sure you avoid these pitfalls:

Mistake #1: Ignoring IRS Notices

Those letters don't go away if you ignore them. In fact, each notice represents an escalation in the collection process. Open them, read them carefully, and respond by the deadline. Missing response deadlines limits your options and speeds up enforcement actions.

Mistake #2: Using Credit Cards or Retirement Funds

Paying your tax debt with a credit card might seem convenient, but the interest rates are brutal. You're just trading one debt for another, often at a higher rate.

Raiding your 401(k) or IRA is even worse. You'll pay income tax on the withdrawal plus a 10% early withdrawal penalty if you're under 59½. You could end up owing more in taxes than you originally owed!

Mistake #3: Believing Tax Relief Scams

Be incredibly skeptical of companies promising to settle your tax debt for "pennies on the dollar" or guaranteeing specific outcomes. These tax relief mills charge huge upfront fees and often deliver little value. The IRS has specific requirements for Offers in Compromise and other relief programs. No one can guarantee acceptance.

Mistake #4: Not Keeping Current

If you work out a payment plan for past taxes, you absolutely must stay current on your current year taxes. Falling behind again while you're in an installment agreement can void the agreement and restart aggressive collection actions.

How Tax Laws Protect You (Yes, Really)

Under the Internal Revenue Code, you have specific rights when dealing with the IRS. The Taxpayer Bill of Rights includes important protections:

The right to be informed means the IRS must explain what you owe and why. The right to quality service requires professional, courteous treatment. The right to pay no more than the correct amount ensures you're only charged what you legally owe.

These aren't just nice ideas-they're enforceable rights. If the IRS violates them, you can challenge their actions through the Taxpayer Advocate Service or in Tax Court.

The statute of limitations also works in your favor. The IRS generally has 10 years from the assessment date to collect unpaid taxes. After that, the debt expires. However, certain actions like filing for bankruptcy or submitting an Offer in Compromise can pause or extend this timeline, so don't count on it as a strategy.

Understanding Collection Due Process Rights

When the IRS plans to take collection action, you have the right to a Collection Due Process (CDP) hearing. This is huge. You can request a CDP hearing within 30 days of receiving certain notices, including:

- Notice of Federal Tax Lien Filing

- Final Notice of Intent to Levy

- Notice of Jeopardy Levy

During the CDP hearing, you can propose collection alternatives like installment agreements or an Offer in Compromise. You can also challenge whether you actually owe the tax. An independent IRS Appeals Officer reviews your case, and their decision can prevent or reverse collection actions.

This is one area where having professional representation really matters. Tax attorneys know how to present your case effectively and what documentation Appeals Officers need to see.

Moving Forward With Confidence

Dealing with IRS unpaid taxes isn't fun, but it's also not insurmountable. Thousands of taxpayers successfully resolve their tax debt every year using the programs and options we've discussed.

The key is taking action rather than hiding from the problem. Whether that means setting up a payment plan, requesting penalty abatement, or exploring settlement options, you have paths forward. You don't have to figure this out alone, and you don't have to live with the constant stress of unresolved tax debt.

Remember that the IRS collection machine keeps moving whether you engage with it or not. The earlier you address your unpaid taxes, the more options you'll have and the less you'll ultimately pay in penalties and interest. That notice sitting in your drawer isn't going to resolve itself, but with the right approach and possibly the right help, you can get past this and move on with your financial life.

Facing IRS unpaid taxes can feel overwhelming, but you don't have to navigate this challenge alone. With the right guidance and strategy, you can resolve your tax debt and regain financial peace of mind. The Law Offices of Darrin T. Mish, P.A. has helped taxpayers across the globe tackle their IRS problems for over 32 years, offering personalized legal solutions backed by deep expertise in tax law. If you're ready to take control of your tax situation, schedule a free consultation today and discover how we can help you find the best resolution for your specific circumstances.