I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Facing tax debt can feel overwhelming, especially when notices from the IRS start piling up in your mailbox. You're not alone-millions of Americans struggle with unpaid taxes each year, and the good news is that the IRS offers several pathways to resolve your debt. Understanding irs tax debt settlement options can make the difference between years of financial stress and a fresh start. Whether you owe thousands or hundreds of thousands, knowing your rights and available programs helps you take control of your situation and move forward with confidence.

What Is IRS Tax Debt Settlement?

IRS tax debt settlement refers to formal programs and arrangements that allow taxpayers to resolve their outstanding tax obligations for less than the full amount owed or through manageable payment structures. The IRS recognizes that not everyone can pay their full tax liability immediately, and they've established several legitimate pathways to help taxpayers satisfy their debts.

The most well-known form of irs tax debt settlement is the Offer in Compromise (OIC), but that's just one tool in your resolution toolkit. Settlement options also include installment agreements, penalty abatement, and currently not collectible status. Each serves different circumstances and financial situations.

Why the IRS Settles Tax Debt

You might wonder why the IRS would accept less than what you owe. The answer is practical: the agency would rather collect something than nothing. If you genuinely cannot pay your full debt, the IRS may agree to a settlement to close your account and move on. According to the IRS Internal Revenue Manual, the agency considers settlement offers when collection of the full amount would create economic hardship or when full payment is unlikely.

The IRS evaluates your reasonable collection potential (RCP), which includes your assets, income, and expenses. If your RCP is less than your total debt, you might qualify for a settlement. However, acceptance isn't guaranteed-the IRS maintains strict criteria to prevent abuse of these programs.

Understanding Your IRS Tax Debt Settlement Options

Let's break down the primary settlement options available to taxpayers in 2026. Each has specific requirements, advantages, and limitations that you need to understand before moving forward.

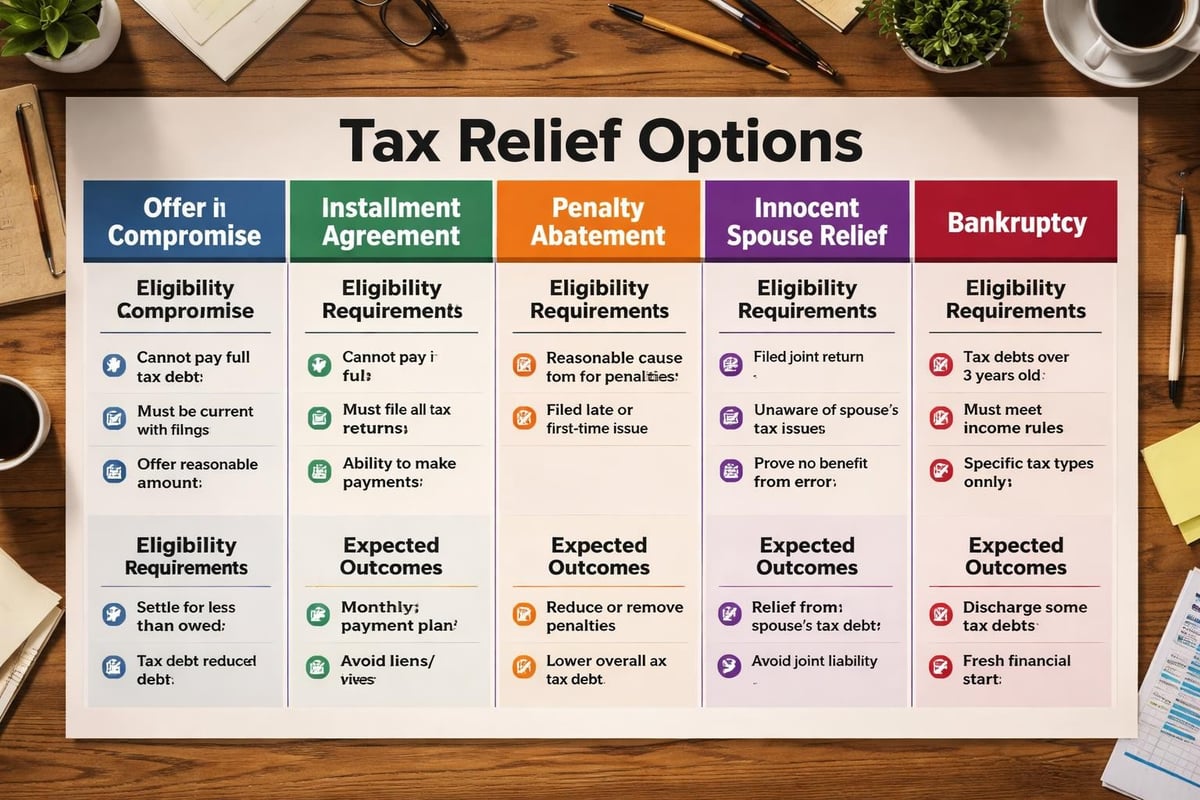

Offer in Compromise: Settling for Less

An Offer in Compromise allows you to settle your tax debt for less than the full amount owed. It's the most dramatic form of irs tax debt settlement, but it's also the most difficult to obtain. Data shows that the IRS has maintained an approval rate around 21% for these offers, meaning most applications are rejected.

To qualify, you must demonstrate one of three conditions:

- Doubt as to collectibility: You can't pay the full amount before the collection statute expires

- Doubt as to liability: There's legitimate uncertainty about whether you owe the tax

- Effective tax administration: Collecting the full amount would create economic hardship or be unfair

The application requires detailed financial disclosure through Form 656 and Form 433-A (for individuals) or Form 433-B (for businesses). You'll need to document your income, expenses, assets, and liabilities thoroughly.

| OIC Type | Best For | Success Rate | Processing Time |

|---|---|---|---|

| Doubt as to Collectibility | Limited assets/income | Moderate | 6-12 months |

| Doubt as to Liability | Disputed tax assessments | Low | 3-9 months |

| Effective Tax Administration | Hardship cases | Moderate | 6-12 months |

Installment Agreements: Paying Over Time

If you can pay your full debt but need more time, an installment agreement might be your best option. This isn't technically a settlement since you pay the full amount, but it provides crucial breathing room. The IRS offers several types of payment plans, and understanding your installment agreement options can help you choose the right one.

Streamlined installment agreements are available for debts under $50,000 (increased from $25,000 in recent years) and require minimal financial disclosure. You can set up these agreements online through the IRS website, and they're typically approved quickly.

For larger debts, you'll need a more comprehensive agreement requiring full financial disclosure. These take longer to process but can extend payment terms up to 72 months.

Currently Not Collectible Status

Sometimes you can't pay anything toward your tax debt right now. In these situations, the IRS may declare your account Currently Not Collectible (CNC). This temporarily halts collection activities, though interest and penalties continue accruing. Getting CNC status requires proving that paying any amount would prevent you from meeting basic living expenses.

CNC status isn't permanent. The IRS periodically reviews your financial situation, and if your circumstances improve, they'll resume collection efforts. However, it provides valuable relief when you're facing genuine financial hardship.

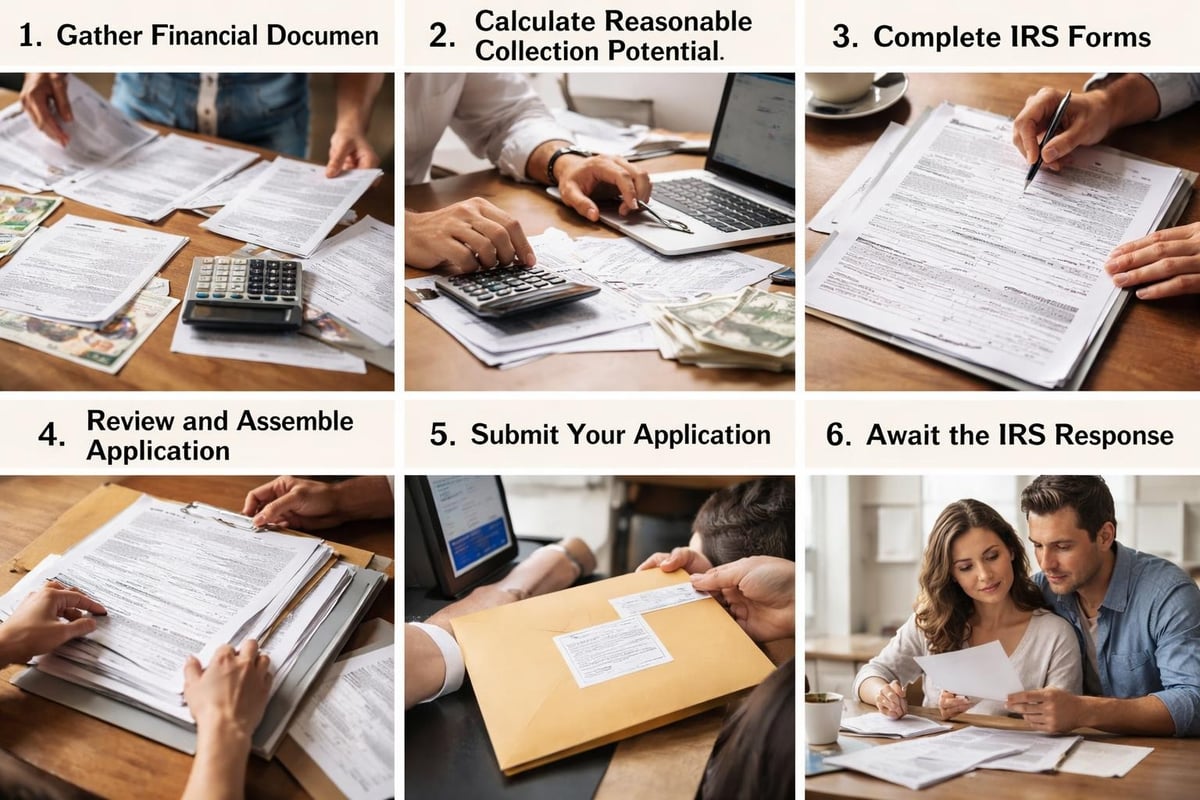

The Application Process for IRS Tax Debt Settlement

Navigating the settlement process requires careful preparation and attention to detail. Making mistakes on your application can result in automatic rejection, so understanding each step is critical.

Step 1: Gather Your Financial Documentation

Before you apply for any irs tax debt settlement program, compile complete financial records. You'll need:

- Recent pay stubs or proof of income

- Bank statements from the past three months

- Documentation of monthly expenses (utilities, rent, insurance)

- Asset valuations (home, vehicles, investments)

- Retirement account statements

- Proof of other debts and obligations

The IRS will scrutinize these documents, so accuracy matters. Underreporting income or overstating expenses can lead to rejection and potential fraud allegations.

Step 2: Calculate Your Reasonable Collection Potential

Your RCP determines whether the IRS will accept your offer. The formula considers:

- Asset equity: Fair market value minus amounts owed on those assets

- Future income: Monthly income minus allowable expenses, multiplied by a specific number of months

- Special circumstances: Exceptional expenses like serious medical conditions

The IRS uses national and local expense standards to determine allowable expenses. You can't claim unlimited spending-the agency caps expenses like food, clothing, and transportation based on family size and location.

Step 3: Submit Your Application

Once you've prepared your financial information, complete the appropriate forms. For an Offer in Compromise, you'll submit Form 656 along with the financial statement forms. Include a non-refundable application fee ($205 as of 2026) unless you qualify for the low-income exception.

You must also include an initial payment with your offer. The IRS offers two payment options:

- Lump sum: 20% of the total offer amount, with the remainder due within five months of acceptance

- Periodic payment: First payment with the application, followed by monthly payments during the evaluation period

According to resources like Debt.org’s guide to settling tax debt, choosing the right payment option depends on your cash flow and ability to access funds quickly.

Step 4: Wait for IRS Review

The IRS takes time to evaluate settlement applications-often six months or longer. During this period, the collection statute of limitations is suspended, giving the IRS additional time to collect. The agency may request additional documentation or clarification, and you must respond promptly to avoid rejection.

Common Mistakes That Derail Settlement Attempts

Even well-intentioned taxpayers make errors that sabotage their settlement applications. Avoiding these pitfalls increases your chances of success significantly.

Underestimating Your Assets or Income

The IRS has sophisticated tools to verify your financial information. They cross-reference your application with tax returns, third-party income reports, and property records. If you omit assets or underreport income-even accidentally-your application will be rejected. Worse, intentional misrepresentation can lead to criminal charges.

Failing to Stay Current

While your settlement application is pending, you must remain current on all filing and payment obligations. If you owe estimated taxes, you need to make those payments. If you haven't filed all required returns, addressing unfiled tax returns becomes a prerequisite before the IRS will consider your settlement offer.

Missing a filing deadline or falling behind on current-year taxes will result in automatic rejection of your application. This requirement catches many taxpayers off guard.

Choosing the Wrong Settlement Option

Not every taxpayer needs an Offer in Compromise. Sometimes an installment agreement or penalty abatement better fits your situation. Pursuing an OIC when you don't qualify wastes time and money. Understanding which program matches your circumstances requires analyzing your complete financial picture.

Alternative Strategies Beyond Traditional Settlement

IRS tax debt settlement isn't limited to formal programs. Several additional strategies can reduce your tax burden or make it more manageable.

Penalty Abatement

The IRS assesses penalties for late filing, late payment, and accuracy-related issues. These penalties can add 25% or more to your tax bill. You may qualify for penalty relief through first-time abatement (if you have a clean compliance history) or reasonable cause abatement (if circumstances beyond your control caused the violation).

Removing penalties doesn't eliminate your tax debt, but it significantly reduces the total amount you owe. This strategy works particularly well when combined with an installment agreement.

Innocent Spouse Relief

When you file a joint return, both spouses are jointly liable for the full tax debt. However, if your spouse understated income or claimed improper deductions without your knowledge, you might qualify for innocent spouse relief. This program can eliminate or reduce your portion of the joint liability.

Three types of relief exist:

- Traditional innocent spouse relief

- Separation of liability relief

- Equitable relief

Each has specific requirements, and you must request relief within two years of the IRS beginning collection activities (with some exceptions).

Bankruptcy Considerations

In limited circumstances, bankruptcy can discharge tax debt. Generally, income tax debt can be discharged if:

- The tax is income tax (not trust fund or other types)

- You filed a legitimate tax return for that year

- The tax debt is at least three years old

- The IRS assessed the tax at least 240 days before bankruptcy

- You didn't commit fraud or willful evasion

Bankruptcy has serious long-term consequences, but it might be appropriate if you have substantial non-tax debt along with your IRS obligation. Discussing options with professionals who understand both bankruptcy and tax law is essential.

Working with Tax Professionals on Settlement

While you can pursue irs tax debt settlement on your own, professional representation often increases your success rate. Tax attorneys, CPAs, and enrolled agents understand IRS procedures and can navigate complex situations more effectively than most taxpayers.

When Professional Help Makes Sense

Consider professional representation if:

- Your tax debt exceeds $10,000

- You have complicated financial circumstances

- The IRS has initiated enforcement actions like wage garnishment or tax liens

- You've already had an application rejected

- You're uncertain which settlement option fits your situation

Tax attorneys provide additional benefits through attorney-client privilege, which protects your communications. This becomes important if your situation involves potential criminal issues or aggressive IRS collection activities.

What to Expect from Professional Representation

A qualified tax professional will analyze your financial situation, review your tax history, and recommend the most appropriate resolution strategy. They'll handle IRS communications, prepare required documentation, and negotiate on your behalf. According to insights from SmartAsset’s tax debt settlement guide, professional representation can significantly improve your chances of achieving favorable terms.

However, be cautious of companies making unrealistic promises. No one can guarantee the IRS will accept your settlement offer. Legitimate professionals provide honest assessments based on your specific circumstances, not blanket assurances.

The Tax Consequences of Debt Settlement

One aspect many taxpayers overlook is that forgiven debt can create additional tax liability. If the IRS accepts your Offer in Compromise and forgives part of your debt, you might owe taxes on the forgiven amount. As explained by InCharge Debt Solutions, cancelled debt is generally taxable income.

However, exceptions exist. If you were insolvent (your liabilities exceeded your assets) when the debt was forgiven, you may exclude some or all of the cancelled debt from income. This requires filing Form 982 with your tax return and carefully documenting your insolvency.

Understanding taxes and debt forgiveness helps you avoid surprise tax bills after successfully settling your original debt. This is another area where professional guidance proves valuable.

Recent Changes to IRS Settlement Programs

The IRS has made several taxpayer-friendly changes to settlement programs in recent years. Understanding these updates helps you take advantage of more flexible options available in 2026.

Increased Thresholds and Streamlined Processes

The threshold for streamlined installment agreements increased from $25,000 to $50,000, making it easier for more taxpayers to establish payment plans without extensive financial disclosure. Similarly, the IRS has relaxed some rules for tax debt settlement to help taxpayers struggling with financial hardship.

The agency also expanded its Fresh Start initiative, which modified lien filing thresholds and created more flexible payment agreements. These changes reflect the IRS's recognition that rigid collection practices often yield worse outcomes than cooperative resolution approaches.

Online Tools and Self-Service Options

The IRS has invested in digital tools that make settlement applications more accessible. You can now submit certain applications online, check the status of your case, and set up payment agreements without speaking to an agent. While complex cases still benefit from professional representation, straightforward situations can often be handled through these self-service platforms.

Making the Right Decision for Your Situation

Choosing the right irs tax debt settlement approach requires honest assessment of your financial reality. Can you pay your debt in full if given enough time? Then an installment agreement makes sense. Are you genuinely unable to pay the full amount before the collection statute expires? An Offer in Compromise might be appropriate.

Ask yourself these questions:

- What are my total monthly income and necessary expenses?

- What assets do I own, and what's their current value?

- How much equity do I have after subtracting what I owe on those assets?

- Am I current on all tax filings and current-year payments?

- Do I have the documentation to support my financial claims?

Your answers determine which settlement path offers the best combination of relief and realistic approval chances. Remember that the IRS would rather work with you than against you, but you need to demonstrate genuine financial need and good faith effort.

If you're looking for comprehensive strategies for settling IRS debt, consider all available options before committing to a specific approach. Sometimes combining strategies-like penalty abatement with an installment agreement-yields better results than pursuing a single solution.

IRS tax debt settlement provides real solutions for taxpayers facing overwhelming obligations, but success requires understanding your options and presenting your case effectively. Whether you pursue an Offer in Compromise, installment agreement, or another resolution strategy, taking action now prevents more serious enforcement actions down the road. The Law Offices of Darrin T. Mish, P.A. has helped clients resolve complex tax situations for over three decades, offering the experience and personalized attention needed to navigate IRS settlement programs successfully. If you're ready to address your tax debt and explore your settlement options, Law Offices of Darrin T. Mish, P.A. offers free consultations to evaluate your situation and develop a resolution strategy tailored to your needs.