I’m Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn’t theory – it’s what I’ve actually watched work.

Dealing with tax debt can feel like you're carrying a boulder uphill every single day. The notices keep coming, the interest keeps piling up, and you might be wondering if there's any way out of this mess. Here's the good news: the IRS actually wants to work with you, and there are legitimate ways to irs settle tax debt without resorting to those questionable "pennies on the dollar" promises you see on late-night TV. Whether you owe $5,000 or $500,000, understanding your options is the first step toward getting your financial life back on track.

Understanding Your Tax Debt Situation

Before you can effectively irs settle tax debt, you need to know exactly what you're dealing with. Think of it like going to the doctor. You wouldn't start treatment without a diagnosis, right?

Getting the Full Picture

The IRS keeps detailed records of everything you owe, and you have every right to access that information. Your total tax debt includes:

- The original tax amount you didn't pay

- Penalties for late filing or late payment

- Interest that compounds daily on the unpaid balance

- Any additional fees from collection actions

You can request a complete account transcript from the IRS to see the breakdown. This document shows every transaction, payment, penalty, and interest charge on your account. It's essential reading if you're serious about resolving your IRS tax debt.

Here's something many taxpayers don't realize: interest on tax debt isn't fixed. It fluctuates quarterly based on the federal short-term rate plus 3%. In 2026, we're seeing rates that make carrying tax debt extremely expensive over time.

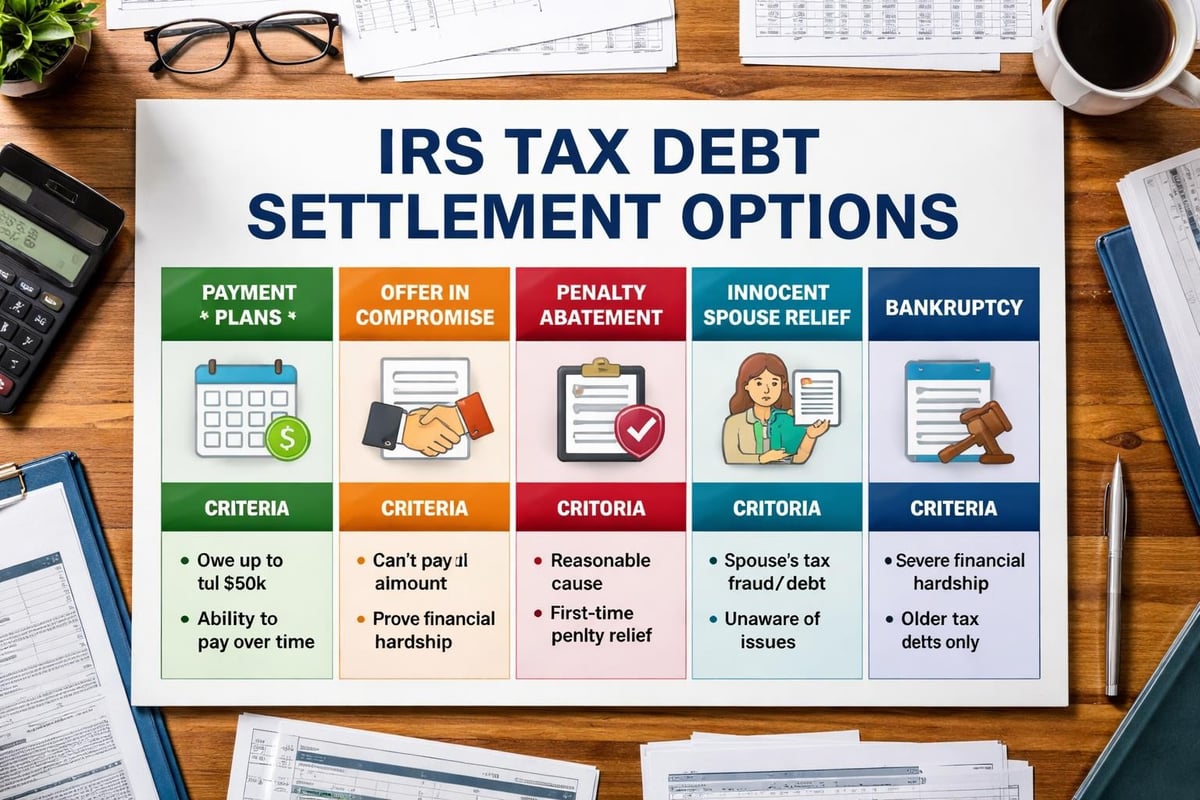

Payment Plans: The Most Common Path

Let's start with the most straightforward option. Sometimes you can't irs settle tax debt for less than you owe, but you can make it manageable through installment agreements.

Short-Term Payment Plans

If you can pay your full tax debt within 180 days, the IRS offers short-term payment plans with minimal setup requirements. These work well if you're expecting a bonus, tax refund, or other lump sum payment.

| Feature | Short-Term Plan | Long-Term Plan |

|---|---|---|

| Duration | Up to 180 days | Up to 72 months |

| Setup Fee | $0 | $31-$225 |

| Financial Disclosure | Not required | May be required |

| Best For | Temporary cash flow issues | Extended financial hardship |

Long-Term Installment Agreements

When you need more time, installment agreements let you spread payments over several years. The IRS will generally approve these if you owe less than $50,000 and can pay off the debt within 72 months.

The beauty of installment agreements? They stop most collection actions immediately. No more threatening letters, no wage garnishments, no bank levies. You're buying yourself breathing room and peace of mind.

Offer in Compromise: Settling for Less

Now we're getting to what most people think of when they want to irs settle tax debt. An Offer in Compromise (OIC) is the IRS's way of saying, "Okay, we'll accept less than what you owe if that's truly all you can pay."

Who Actually Qualifies?

Here's where reality meets expectation. The IRS accepted only about 25% of OIC applications in recent years. Why? Because they have strict qualification criteria based on doubt as to collectibility, doubt as to liability, or effective tax administration.

The IRS looks at four main factors:

- Your income – What you currently earn and what you could reasonably earn

- Your expenses – But only "allowable" expenses by IRS standards

- Your assets – Everything you own that has value

- Your future earning ability – Your age, education, health, and work history matter

You might think you qualify because times are tough, but the IRS has a very specific formula. They calculate your reasonable collection potential (RCP) by analyzing your monthly disposable income multiplied by 12 or 24 months, plus your asset equity.

The Application Process

Submitting an OIC isn't like filling out a simple form. You're essentially proving to the IRS that you legitimately cannot pay your full tax debt, now or in the foreseeable future. According to the IRS’s guidance on settling tax debt, you need to be current with all filing and payment requirements before they'll even consider your offer.

Required documentation includes:

- Form 656 (Offer in Compromise)

- Form 433-A (OIC) or 433-B (OIC) for collection information

- Application fee ($205 as of 2026)

- Initial payment with your offer

- Five years of complete financial information

The process typically takes 6-12 months, sometimes longer. During this time, the statute of limitations on collection is suspended, which can work for or against you depending on your situation.

Currently Not Collectible Status

Sometimes the best way to irs settle tax debt is to prove you genuinely can't pay anything right now. The IRS has a classification called Currently Not Collectible (CNC) status that essentially puts your account on hold.

How CNC Status Works

When you're granted CNC status, the IRS temporarily stops all collection activities. They won't garnish your wages, levy your bank accounts, or send you threatening letters. But here's the catch: interest and penalties keep accumulating, and the IRS will periodically review your financial situation.

You might qualify for CNC if:

- Your monthly income barely covers basic living expenses

- You're facing temporary unemployment or medical hardship

- Collecting from you would create undue economic hardship

- Your only income is Social Security or disability benefits

This isn't really "settling" your debt, but it gives you breathing room. In some cases, taxpayers in CNC status hold this status until the 10-year collection statute expires, effectively eliminating the debt without payment.

Penalty Abatement: Reducing What You Owe

You can't always irs settle tax debt through an OIC, but you can often reduce it significantly by getting penalties removed. Penalties can represent 25% or more of your total debt.

First-Time Penalty Abatement

If you have a clean compliance history for the past three years, the IRS offers first-time penalty abatement almost automatically. This can remove failure-to-file and failure-to-pay penalties, though interest remains.

Reasonable Cause Abatement

Beyond first-time relief, you can request penalty abatement based on reasonable cause:

- Serious illness or death in the family

- Natural disasters or fires

- Incorrect advice from a tax professional

- Unavoidable absence

- System failures or lost records

The key is documentation. You need to prove your circumstances prevented you from meeting your tax obligations despite exercising ordinary business care and prudence.

Innocent Spouse Relief: When It Wasn't Your Debt

Sometimes the tax debt isn't really yours, even if your name is on the return. Innocent spouse relief can completely eliminate tax debt that resulted from your spouse's or ex-spouse's actions.

You might qualify if:

- You filed a joint return with understated tax

- The understatement is due to your spouse's erroneous items

- You didn't know and had no reason to know about the understatement

- It would be unfair to hold you liable considering all facts and circumstances

This relief can also apply to unpaid taxes, not just understatements, through separation of liability or equitable relief provisions.

Bankruptcy: The Nuclear Option

Yes, some tax debt can be discharged in bankruptcy, though it's complicated. You can potentially settle IRS debt through bankruptcy if the tax debt meets specific criteria.

The tax debt must be:

| Requirement | Details |

|---|---|

| Income tax | Payroll taxes and fraud penalties can't be discharged |

| At least 3 years old | From the original due date of the return |

| Filed at least 2 years ago | You must have filed the return, not the IRS |

| Assessed 240+ days ago | The IRS must have assessed the tax at least 240 days before filing |

| No fraud or evasion | You can't have committed fraud or willful evasion |

Even if your tax debt qualifies, bankruptcy has serious long-term consequences for your credit and financial future. It's truly a last resort when you've exhausted all other options to irs settle tax debt.

When to Hire Professional Help

Look, I get it. You're trying to save money, and hiring a tax attorney seems like just another expense you can't afford. But here's the reality: navigating IRS procedures, understanding your options, and presenting your case effectively requires specialized knowledge.

What a Tax Attorney Brings to the Table

Professional representation isn't about filling out forms. It's about strategy, negotiation, and knowing exactly how the IRS operates. Finding the right Tampa tax attorney means getting someone who's been through thousands of cases and knows which approach works best for your specific situation.

Benefits include:

- Direct communication with the IRS on your behalf

- Strategic advice on timing and approach

- Protection from saying something that hurts your case

- Knowledge of options you didn't know existed

- Experience with appeals and negotiations

Someone with over three decades of experience has seen scenarios like yours hundreds of times. They know the shortcuts, the pitfalls, and the strategies that actually work in 2026.

Common Mistakes That Cost You Money

When you're trying to irs settle tax debt, certain mistakes can derail your efforts or cost you thousands. Let's talk about what to avoid.

Ignoring the Problem

Every day you ignore tax debt, it grows. Penalties and interest compound daily. The IRS's collection powers increase. What started as a $10,000 problem can balloon to $15,000 or $20,000 before you know it.

Falling for Tax Relief Scams

Those companies promising to settle tax debt for pennies on the dollar? Many charge huge upfront fees and deliver nothing. The IRS warns specifically about these scams in their guidance on resolving tax debt.

Red flags include:

- Guarantees without reviewing your finances

- Pressure to pay large upfront fees

- Claims they have special relationships with the IRS

- Advising you not to contact the IRS directly

- Promises that sound too good to be true

Not Filing Returns

Here's something critical: you can't irs settle tax debt if you have unfiled tax returns. The IRS requires full compliance before they'll work with you on any settlement option. File those returns, even if you can't pay. The failure-to-file penalty is much steeper than the failure-to-pay penalty.

Statute of Limitations: Time Can Be Your Friend

The IRS has 10 years from the date of assessment to collect tax debt. This is called the Collection Statute Expiration Date (CSED). After this date expires, the debt is legally uncollectible.

Actions That Extend the Statute

Certain actions pause or extend the collection statute:

- Filing an Offer in Compromise (plus 30 days)

- Requesting a Collection Due Process hearing

- Filing bankruptcy

- Living outside the United States for six months or more

- Requesting innocent spouse relief

- Signing a waiver extending the statute

Understanding how these timelines work is crucial when planning your strategy to irs settle tax debt. Sometimes the smart move is to wait and maintain compliance while the clock runs out.

Moving Forward in 2026

Tax laws change, IRS policies evolve, and what worked five years ago might not be your best option today. The IRS’s current approach to helping taxpayers emphasizes working with people who genuinely want to resolve their obligations.

Your action plan should include:

- Determining exactly what you owe and why

- Gathering complete financial documentation

- Evaluating which resolution option fits your situation

- Acting quickly before collection actions intensify

- Staying compliant with current year obligations

Remember, the IRS isn't going away, and neither is your tax debt unless you take action. Whether you pursue an installment agreement, an Offer in Compromise, or another resolution method, the key is getting started today.

The good news? You have more options than you think to irs settle tax debt, and with the right approach and guidance, you can find a resolution that lets you sleep at night again. The process might feel overwhelming now, but thousands of taxpayers work through this successfully every year. You can too.

Resolving tax debt isn't something you should tackle alone, especially with the complex rules and procedures the IRS follows in 2026. Whether you're facing wage garnishment, bank levies, or simply drowning in notices, professional guidance makes all the difference between a solution that works and years of financial stress. The Law Offices of Darrin T. Mish, P.A. has spent over 32 years helping taxpayers across the globe navigate IRS problems, from payment plans to complex offers in compromise. With a free consultation, you can understand your options and start building a strategy that actually fits your financial reality, not just a one-size-fits-all approach.