IRS problems aren't as complicated as they look once you see the structure. I'm attorney Darrin Mish. I've represented taxpayers before the IRS for three decades — in Florida, Colorado, Texas, and internationally. Here's the plain-English breakdown.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

You opened your mailbox and found a CP2000 notice. The IRS says you underreported income-maybe a 1099 you forgot, maybe a W-2 discrepancy-and now they want additional tax. Fine. But they also tacked on penalties that push the bill into territory you didn't budget for. The good news: those penalties aren't set in stone. CP2000 penalty abatement exists, but only if you know which arguments the IRS actually accepts.

Most taxpayers freeze when they see the total. Don't. The CP2000 isn't a bill yet-it's a proposal. You have time, options, and leverage if you respond correctly.

What a CP2000 Notice Actually Means

The IRS matches your tax return against third-party reports: W-2s, 1099s, K-1s, broker statements. When the numbers don't align, they send a CP2000 notice proposing adjustments. It's not an audit. It's automated matching gone wrong-or right, depending on whether you actually forgot something.

The notice breaks down the discrepancy, recalculates your tax, and adds interest. Then come the penalties. Usually accuracy-related penalties under IRC Section 6662, sometimes failure-to-pay penalties under IRC Section 6651(a)(2). Those penalties compound the damage fast.

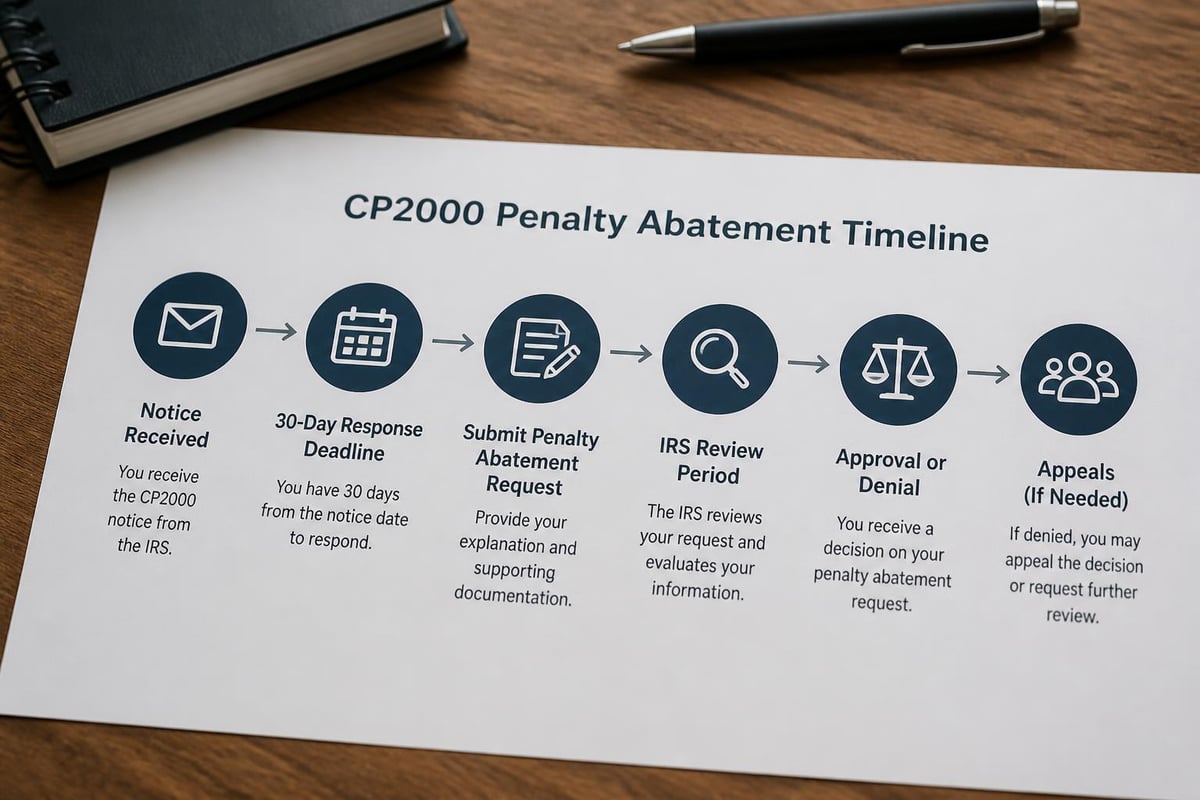

You have 30 days to respond. Miss that window and the IRS converts the proposal into an actual assessment. Once it's assessed, your options narrow.

The Penalties That Show Up on CP2000 Notices

The accuracy-related penalty under IRC Section 6662 hits at 20% of the underpayment. The IRS applies this when they believe you substantially understated income or were negligent. The accuracy-related penalty doesn't require intent-just a discrepancy they think you should've caught.

Failure-to-pay penalties under IRC Section 6651(a)(2) accrue at 0.5% per month on unpaid tax, capping at 25%. If the CP2000 shows tax due from a prior year that you didn't pay, this penalty stacks on top.

Interest isn't a penalty-it's statutory under IRC Section 6601. You can't abate interest except in rare IRS error situations. But penalties? Those are negotiable.

How CP2000 Penalty Abatement Works

CP2000 penalty abatement follows the same rules as any other penalty relief, with one wrinkle: you're dealing with a proposed assessment, not a finalized one. That means you can dispute the penalties before they hit your account. Easier to stop a penalty than remove it later.

The IRS recognizes three main abatement paths:

- First-Time Penalty Abatement (FTA): Administrative relief for taxpayers with clean compliance history

- Reasonable Cause: Fact-specific arguments under IRC Section 6664(c) and Treasury Regulation 1.6664-4

- Statutory Exception: Narrow situations like reliance on written IRS advice

First-Time Penalty Abatement is your fastest route if you qualify. It's policy-based, not law-based, but the IRS honors it consistently. You need three clean years-no penalties assessed in the prior three tax years-and current compliance (all returns filed, all current taxes paid or on a payment plan).

Reasonable cause requires proof. The IRS looks at whether you exercised ordinary business care and prudence but still couldn't comply. Death, serious illness, natural disaster, unavoidable absence, reliance on a tax professional-these work if documented properly.

The First-Time Penalty Abatement Strategy

FTA is administrative relief under IRS penalty relief guidelines. If you haven't had penalties in the prior three years and you're current on filings and payments, you qualify. The IRS grants this automatically if you ask correctly.

Here's the process:

- Confirm you have three clean years (2023, 2024, 2025 for a 2026 CP2000)

- Verify you're current on all filings and payments

- Request FTA in your CP2000 response or by calling the number on the notice

- Reference First-Time Penalty Abatement by name

The IRS doesn't advertise FTA. You have to claim it. Many taxpayers pay penalties they could've wiped with one phone call.

FTA applies to failure-to-file, failure-to-pay, and failure-to-deposit penalties. It doesn't cover accuracy-related penalties automatically, but sometimes the IRS will abate those too if you're disputing the underlying tax adjustment. That's judgment-call territory.

Reasonable Cause Arguments That Actually Work

Reasonable cause under IRC Section 6664(c) requires proving you acted with ordinary business care and prudence. The standard is objective: would a reasonable person in your situation have made the same mistake?

| Argument | What the IRS Needs | Strength |

|---|---|---|

| Tax professional error | Engagement letter, evidence you provided complete info | Strong if documented |

| Serious illness | Medical records showing incapacity during filing period | Strong |

| Death in family | Death certificate, timeline showing impact on filing ability | Moderate |

| Reliance on IRS publication | Specific citation, explanation of how you followed it | Moderate |

| Natural disaster | FEMA declaration, proof of impact on records/ability to file | Strong |

| Missing documents | Evidence you requested them timely, proof of third-party delay | Weak unless compelling |

Tax professional reliance is common but tricky. You need to show:

- You hired a competent professional

- You gave them complete and accurate information

- The professional made an error despite your cooperation

Hiring your cousin who does taxes on weekends won't cut it. The IRS wants evidence of actual competence-credentials, experience, engagement terms.

Disputing the Underlying Tax Before Arguing Penalties

Sometimes the best penalty abatement strategy is proving the IRS got the tax wrong. If the proposed adjustment disappears, so do the penalties.

Review every line of the CP2000. The IRS makes mistakes-frequently. Common errors:

- Income reported twice (once on your return, once on a 1099 the IRS thinks you missed)

- Income attributed to you that belongs to someone else (wrong SSN on a 1099)

- Failure to account for basis on stock sales or crypto transactions

- Missing deductions or credits that offset the income

Before responding to a CP2000, pull your tax return, gather all third-party documents, and compare line by line. If you can prove the income was reported or doesn't belong to you, the penalty issue evaporates.

If the tax is correct but you have reasonable cause for missing it, that's your penalty abatement play. But always challenge the tax first if you've got an argument.

Responding to the CP2000 to Preserve Abatement Rights

The CP2000 response form has three options:

- Agree with the changes

- Agree with some changes, disagree with others

- Disagree with all changes

Your response sets the tone for penalty abatement. If you check "agree" without mentioning penalties, you're accepting them. The IRS won't raise abatement on its own.

If you're requesting cp2000 penalty abatement, state it explicitly in your response letter. Include:

- Your name, SSN, tax year, and CP2000 notice number

- Explanation of which penalties you're requesting abatement for

- Your abatement argument (FTA or reasonable cause)

- Supporting documents

Send the response by certified mail, return receipt requested. The IRS loses things. Proof of mailing matters.

What Happens After You Request Abatement

The IRS will either accept your abatement request, deny it, or partially approve it. If denied, you'll receive a letter explaining why. That's not the end-you can appeal.

Appeals are handled through the IRS Independent Office of Appeals. You file Form 12203 (Request for Appeals Review) within 30 days of the denial letter. Appeals officers have more discretion than the initial reviewer. They can consider arguments the first reviewer ignored.

If Appeals denies abatement, you can challenge the penalties in Tax Court-but only after the IRS formally assesses them. That's post-CP2000 territory. You can't petition Tax Court over a proposed assessment.

Timing Matters More Than You Think

The 30-day response window on a CP2000 is real. The IRS will send a statutory notice of deficiency if you don't respond. That triggers a 90-day window to petition Tax Court. Miss that and the tax and penalties become final.

Even if you need more time to gather documents, respond within 30 days. Request an extension in writing. The IRS often grants 30 additional days, sometimes more if you explain why.

If you already missed the 30 days, check the notice date. The IRS sometimes grants late responses if you're close to the deadline. But don't count on it.

Combining Abatement with Payment Options

Penalty abatement doesn't erase the underlying tax. If the IRS is right about the discrepancy, you owe the tax plus interest. But removing penalties can make the bill manageable.

You can request abatement and simultaneously propose a payment plan. Installment agreements spread the balance over months or years. If the balance after abatement is under $50,000, you can set up a streamlined agreement online without financial statements.

For larger balances, the IRS requires Collection Information Statements (Forms 433-A or 433-F). If you can't pay the remaining balance in full, consider combining abatement with an Offer in Compromise-settling for less than the full amount if you qualify.

Penalties count toward your total balance when calculating offers. Abate the penalties first, reduce the balance, improve your settlement leverage.

Common CP2000 Penalty Abatement Mistakes

Ignoring the notice. The IRS doesn't forget. Silence converts the proposal into an assessment, and then you're fighting collection actions instead of penalties.

Accepting penalties without asking for relief. The IRS won't volunteer abatement. You have to request it.

Requesting abatement without documentation. Reasonable cause claims need proof. "I was busy" doesn't work. Medical records, professional correspondence, contemporaneous notes-those work.

Confusing First-Time Abatement with first-time filing. FTA requires three clean penalty years, not three years of filing returns. If you've filed for 20 years but had a penalty in 2024, you don't qualify for FTA in 2026.

Arguing hardship instead of reasonable cause. Financial hardship isn't reasonable cause for accuracy-related penalties. The IRS doesn't care that you couldn't afford to pay-they care whether you had a valid reason for underreporting.

When Professional Help Pays Off

Some CP2000 notices are simple. The IRS caught a 1099 you forgot, you agree, you pay. No abatement argument needed.

Others are complex: multiple discrepancies, disputed amounts, professional tax preparer errors, or large penalties that require reasonable cause arguments. That's when representation matters.

A tax attorney can:

- Review the CP2000 for IRS errors

- Draft abatement requests that match IRS standards

- Negotiate with IRS examiners before assessment

- File Appeals if the initial request is denied

- Coordinate abatement with collection alternatives

After 32 years representing taxpayers, I've seen the patterns. The IRS grants abatement when you speak their language-citations, documentation, procedural compliance. Emotional appeals don't work. Evidence does.

IRC Section 6662 and the Substantial Understatement Rule

The accuracy-related penalty under IRC Section 6662(b)(2) applies when your understatement exceeds the greater of 10% of the correct tax or $5,000. For corporations, the threshold is $10,000 or 10% of correct tax (but not less than $10,000).

The IRS can waive this penalty if you show reasonable cause and good faith under IRC Section 6664(c). The burden is on you-the IRS assumes the penalty applies unless you prove otherwise.

Good faith means you made a genuine effort to comply. Reasonable cause means you had a valid reason for the understatement despite that effort. Together, they create your defense.

Substantial authority is another defense under IRC Section 6662(d)(2)(B)(i). If you had substantial authority for a tax position-based on statutes, regulations, case law, or revenue rulings-the penalty doesn't apply even if the position ultimately fails. But that's a high bar. Most CP2000 situations involve missing income, not debatable tax positions.

Interest Abatement: The Exception, Not the Rule

You can't abate interest except when the IRS caused unreasonable delay. IRC Section 6404(e) allows interest abatement if an IRS error or delay in performing a ministerial or managerial act caused interest to accrue.

Ministerial acts are procedural-processing a return, posting a payment. Managerial acts involve discretion or judgment. The IRS rarely admits either type of error caused interest to accrue.

You can request interest abatement on Form 843 (Claim for Refund and Request for Abatement), but expect denial unless you have clear documentation of IRS error with timeline proof. Understanding what qualifies as IRS error helps set realistic expectations.

State CP2000 Equivalents and Double Penalties

If you're in a state with income tax, your CP2000 can trigger a state-level discrepancy notice. California, for example, issues comparable notices for underreported income. States often follow IRS adjustments automatically.

That means double penalties-federal and state. But penalty abatement works at both levels. California’s one-time penalty abatement mirrors federal FTA. Other states have similar programs.

Request federal abatement first. Once approved, use that as leverage with the state. Many states defer to federal determinations on reasonable cause, especially if the facts are identical.

Don't assume state penalties will disappear just because federal penalties did. You need to request relief separately.

Amended Returns and CP2000 Interaction

Sometimes the correct response to a CP2000 is filing an amended return (Form 1040-X). If the IRS caught missing income but you also have offsetting deductions or credits you forgot to claim, an amended return can reduce or eliminate the proposed tax.

File the amended return and attach it to your CP2000 response. Explain that you're correcting the return rather than accepting the IRS proposal. If your corrected return shows less tax due than the CP2000 proposes, the penalties shrink proportionally.

Amended returns don't automatically trigger penalty abatement, but they can eliminate the understatement that caused the penalty. No understatement, no accuracy-related penalty.

You can also request abatement alongside the amended return. "I'm filing this amended return to correct the understatement. I also request First-Time Penalty Abatement for any remaining penalties." Cover both bases.

The Audit Reconsideration Alternative

If you ignored the CP2000 and the IRS already assessed the tax and penalties, you're not out of options. Audit reconsideration under IRS Policy Statement 8-47 allows you to challenge an assessment after the fact if you have new information.

File Form 12661 (Disputed Issue Verification) with documentation showing why the assessment was wrong. If the IRS agrees and reverses the adjustment, the penalties vanish with the tax.

You can request penalty abatement during audit reconsideration even if the tax stands. The IRS reviews both issues if you raise them.

Audit reconsideration is slower and harder than responding to the CP2000 on time. But it's the path when you missed the deadlines.

CP2000 penalty abatement isn't guaranteed, but it's available if you know the rules and respond correctly. The IRS grants relief when you meet their standards-clean compliance history for FTA, solid documentation for reasonable cause. If you're staring at penalties you can't afford and don't know where to start, Law Offices of Darrin T. Mish, P.A. has handled CP2000 notices and penalty abatement for 32 years. Let's talk-free consultation, plain answers, no runaround.