I hear from people every week who think their tax problem is the end of the world. It usually isn't. I'm Darrin Mish. I've resolved over $100 million in tax debt for clients. Here's what you should know.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

You're behind on taxes. The IRS sent letters. Maybe they've already started taking your wages or bank accounts. You want this fixed now, and you're looking at companies that resolve IRS tax debt fast. Here's what you need to understand about speed, about promises, and about what actually stops collection enforcement before it ruins your finances.

What "Fast" Actually Means in IRS Tax Resolution

The IRS doesn't move fast. Their systems are decades old, their backlog is measured in millions of cases, and their internal review processes have mandatory wait periods baked in. When companies that resolve IRS tax debt fast make promises about immediate relief, they're talking about stopping collection activity. Not erasing debt overnight.

Stopping a levy or wage garnishment can happen in days if the paperwork is right and the representative knows which IRS phone numbers actually get answered. That's the speed you're paying for. The underlying resolution-the installment agreement, the offer in compromise, the penalty abatement-takes weeks to months depending on the program.

Here's the realistic timeline for each major resolution option:

| Resolution Type | Typical Timeline | What Causes Delays |

|---|---|---|

| Installment Agreement | 30-60 days | Missing financials, balance disputes |

| Offer in Compromise | 6-12 months | Incomplete documentation, asset verification |

| Penalty Abatement | 30-90 days | Lack of reasonable cause evidence |

| Currently Not Collectible | 30-45 days | Income/expense verification issues |

| Lien Withdrawal | 30 days after debt paid | Payment processing delays |

| Levy Release | 1-7 days | Communication delays with IRS |

Speed matters most when enforcement is active. If the IRS is about to seize your bank account or your next paycheck is getting garnished at 25%, you need someone who can get on the phone with the IRS that day and negotiate a hold. That's where qualified representation earns its fee.

How to Identify Legitimate Tax Resolution Firms

Most companies advertising fast IRS debt resolution aren't law firms. They're marketing operations that sell your case to a network of tax professionals after collecting an upfront fee. Some are legitimate clearinghouses. Many are not.

Red flags that indicate you're dealing with a sales operation:

- They quote you a settlement amount before reviewing your actual financial situation

- They guarantee a specific percentage reduction in your tax debt

- They require full payment upfront before any work begins

- Their "tax professionals" are unlicensed call center employees reading scripts

- They can't tell you which attorney or CPA will handle your case

- They use high-pressure tactics about immediate IRS seizures that haven't been threatened

Green flags that indicate qualified representation:

- Licensed attorney, CPA, or enrolled agent will personally handle your case

- They explain why your case might not qualify for certain programs

- They request your IRS transcripts and financial documents before quoting fees

- They offer a free initial consultation to assess your actual situation

- They're explicit about what they can and cannot do

- They discuss realistic timelines based on your specific resolution path

The IRS maintains a public directory of payment and resolution options that any legitimate firm should reference when explaining your choices. If a company contradicts official IRS guidance, that's a problem.

What Credentials Actually Matter

Only three types of professionals can represent you before the IRS in all matters: attorneys, CPAs, and enrolled agents. Anyone else-tax consultants, resolution specialists, financial advisors-can't negotiate on your behalf beyond basic payment plans.

Attorneys have attorney-client privilege. That means everything you tell your tax attorney is confidential and can't be disclosed to the IRS or used against you. CPAs and enrolled agents don't have that same protection in all jurisdictions. When you're discussing unreported income or missing returns, that privilege matters.

The Four Resolution Paths Companies Actually Use

Companies that resolve IRS tax debt fast aren't inventing new programs. They're using the same four options available to anyone: installment agreements, offers in compromise, currently not collectible status, and penalty abatement. The difference is knowing which one fits your financial situation and executing it correctly the first time.

Installment Agreements: The Most Common Path

You owe $40,000. The IRS wants it now. You can't pay it now. An installment agreement spreads that $40,000 over 72 months at roughly $600/month plus interest. For most taxpayers with steady income and manageable debt, this is the fastest resolution because the IRS approves it almost automatically if you owe less than $50,000 and haven't defaulted on a previous agreement.

The IRS offers several installment agreement types:

- Guaranteed Installment Agreement: Under $10,000, automatic approval, 36 months or less

- Streamlined Installment Agreement: Under $50,000, minimal financial documentation required

- Non-Streamlined Installment Agreement: Over $50,000, requires full financial disclosure

- Partial Payment Installment Agreement: Monthly payment doesn't cover full balance before collection statute expires

A competent representative can get a streamlined installment agreement approved in 30 days. They'll also ensure the monthly payment doesn't trigger financial hardship and that you're not overpaying based on the collection statute expiration date. The IRS has detailed resolution timeline expectations that professionals should know cold.

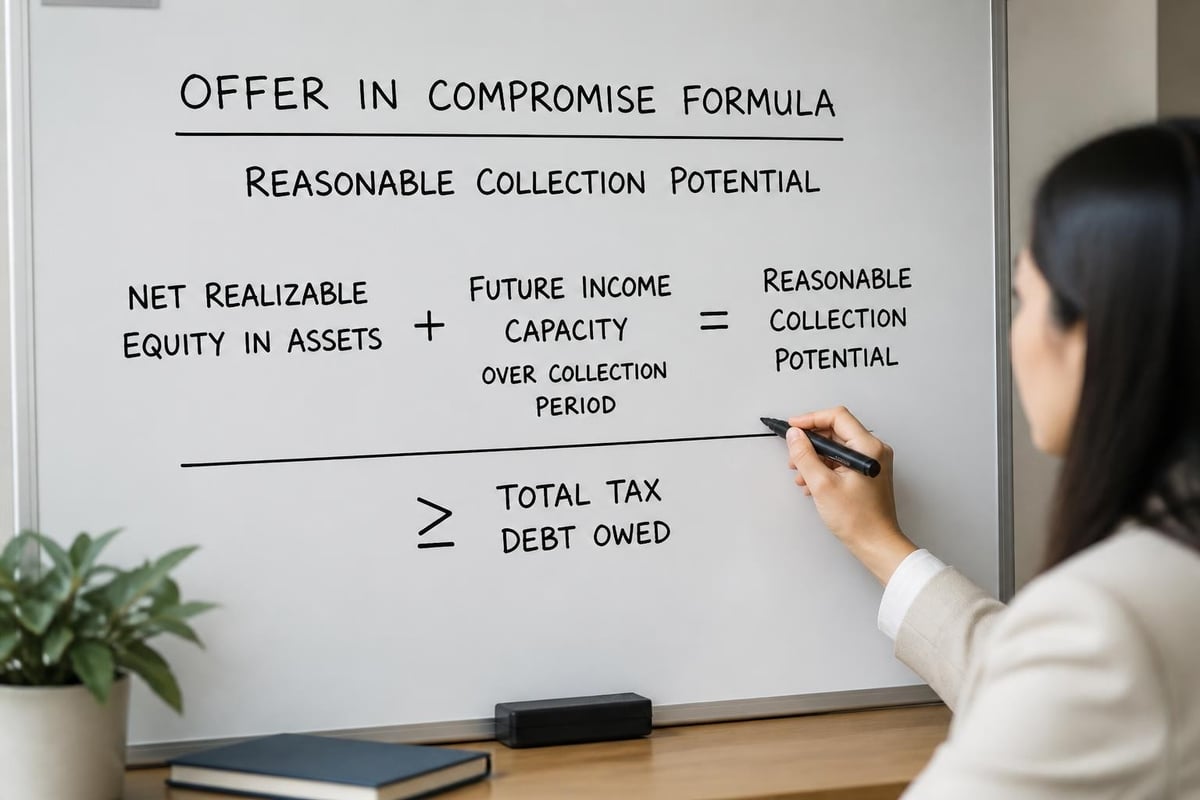

Offers in Compromise: The Program Everyone Wants

You've seen the ads: "Settle your IRS debt for pennies on the dollar!" Those ads reference the Offer in Compromise program, and yes, it's real. The IRS accepts about 40% of offers filed. The other 60% get rejected because taxpayers or their representatives don't understand the qualification criteria.

The IRS uses a formula: your realizable asset value plus your future income potential over 12-24 months. If that number exceeds your tax debt, you don't qualify. Period. Companies that promise offer acceptance without reviewing your assets and income are lying to you.

Pre-qualification requires honest answers to these questions:

- Do you own real estate with equity beyond allowed exemptions?

- Do you have retirement accounts you could access without penalty?

- Do you have future income potential that could pay the debt within the collection statute?

- Have you filed all required tax returns and are you current on estimated payments?

- Are you in an open bankruptcy proceeding?

If you qualify, the process takes 6-12 months because the IRS assigns a designated examiner who investigates your entire financial life. They want bank statements, asset valuations, proof of expenses, employment verification, and explanations for any large deposits or transfers. The comprehensive overview of IRS tax debt resolution options shows exactly what documentation each program requires.

Currently Not Collectible Status: Temporary Relief

You're unemployed. Your only income is Social Security. Your expenses exceed your income. The IRS can designate your account "currently not collectible" and halt all enforcement. Your debt doesn't disappear-it stays on the books-but collection activity stops until your financial situation improves.

This is the fastest resolution for taxpayers in genuine hardship because it doesn't require asset liquidation or payment agreements. A representative files Form 433-F with supporting documentation showing you can't meet basic living expenses and make tax payments. The IRS typically responds within 30-45 days.

The downside: Interest and penalties keep accruing. The IRS reviews your status annually. If your income increases, they'll restart collection. But when you're choosing between food and IRS payments, currently not collectible status gives you breathing room.

Penalty Abatement: Reducing What You Owe

About 40% of your IRS debt might be penalties for late filing, late payment, or accuracy issues. The IRS will abate penalties if you have "reasonable cause"-basically, circumstances beyond your control that prevented compliance. Death of a family member, serious illness, natural disaster, reliance on incorrect professional advice.

First-time penalty abatement is even easier. If you've been compliant for the past three years, haven't had penalties abated before, and have filed all required returns, the IRS will remove failure-to-file and failure-to-pay penalties administratively. No lengthy explanation required.

This isn't a complete resolution strategy, but removing $15,000 in penalties from a $40,000 debt makes the remaining $25,000 manageable through an installment agreement. Penalty abatement often pairs with other resolution options to reduce total debt before negotiating payment terms.

What Happens After You Hire a Firm

You sign the engagement letter and pay the initial fee. Now what? Companies that resolve IRS tax debt fast should immediately file a power of attorney (Form 2848) so the IRS communicates with them instead of you. This stops the panic-inducing letters and lets your representative handle all IRS contact.

The first 30 days typically involve:

- Requesting your IRS account transcripts to verify the actual debt

- Analyzing the collection statute expiration date for each tax year

- Reviewing your financial situation through Form 433-A (individuals) or 433-B (businesses)

- Identifying which resolution option fits your circumstances

- Stopping any active levies or wage garnishments

If enforcement is active-your bank account is frozen or your employer received a wage garnishment notice-your representative should contact the IRS collection division within 24-48 hours to negotiate a temporary hold pending resolution. This is where experience matters. The IRS answers about 20% of incoming calls. Knowing which numbers to call, what information revenue officers require, and how to frame the hardship request determines whether the levy releases in two days or two weeks.

Communication and Case Updates

You should receive regular updates. Not daily-tax resolution isn't that fast-but you should know what's happening at each stage. When did the IRS receive your offer? What additional documentation did they request? When is the expected response date?

Reasonable communication expectations:

- Weekly updates during active negotiation or enforcement

- Bi-weekly updates during pending review periods

- Immediate notification of IRS correspondence or deadline changes

- Access to your representative via phone or email within one business day

Radio silence for weeks at a time indicates either a processing delay (common) or a firm that took your money and deprioritized your case (also common, unfortunately). The IRS has launched online tools in 2026 that help taxpayers track their resolution status, which your representative should be checking regularly.

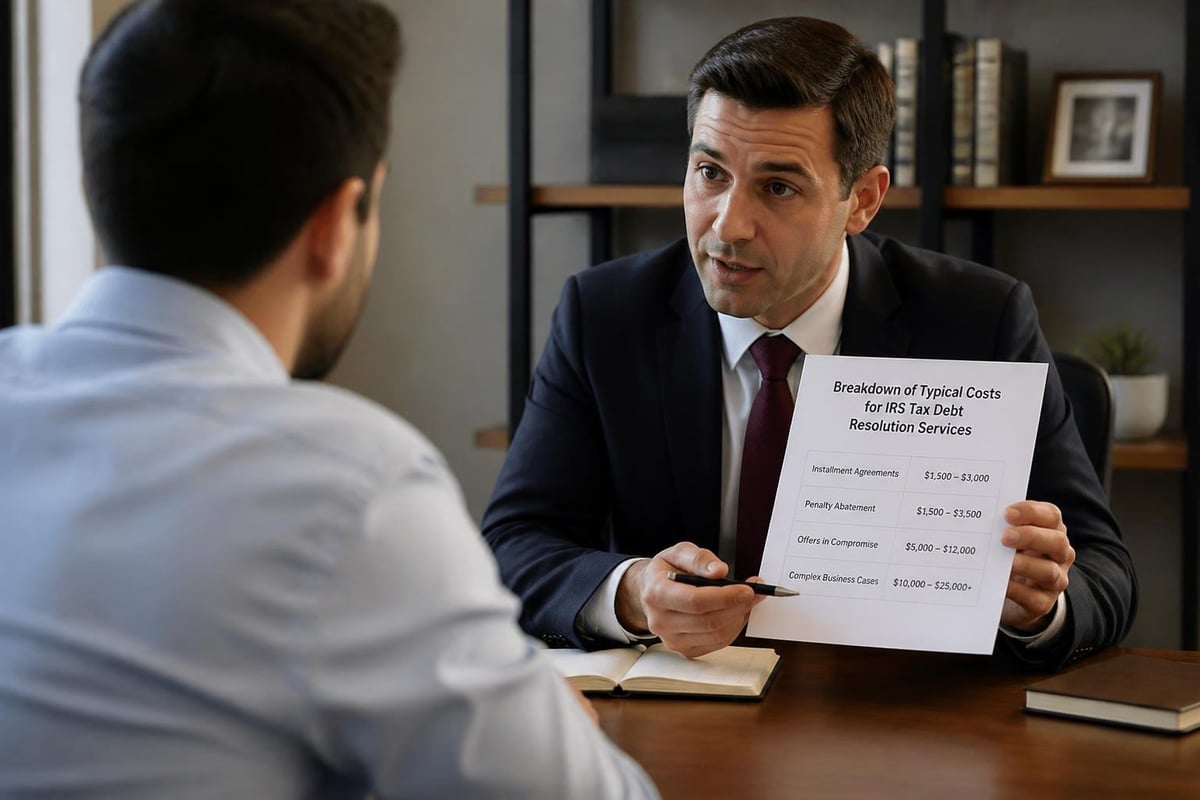

The Cost Structure of Fast IRS Debt Resolution

Most tax resolution firms charge $2,500-$7,500 for straightforward cases and $7,500-$15,000 for complex offers in compromise or business tax debt. Some charge flat fees. Others bill hourly. A few charge contingency fees based on the debt reduction they achieve, though this is ethically questionable and prohibited for attorneys in many states.

Typical fee structures:

| Service Type | Average Cost | Payment Terms |

|---|---|---|

| Simple Installment Agreement | $1,500-$3,000 | 50% upfront, 50% at filing |

| Currently Not Collectible | $2,000-$4,000 | Flat fee or hourly |

| Penalty Abatement | $1,500-$3,500 | Flat fee |

| Offer in Compromise | $5,000-$12,000 | Retainer plus monthly or staged payments |

| Complex Multi-Year Business Tax | $10,000-$25,000+ | Retainer plus hourly billing |

Firms advertising extremely low fees ($500-$1,000) are either adding hidden costs later or providing template-level service where a paralegal fills out forms without customizing strategy to your situation. Firms charging $20,000 upfront for a basic installment agreement are price-gouging.

Ask for a written fee agreement that specifies exactly what services are included, what triggers additional charges, and what happens if the IRS rejects your proposed resolution. If they refuse to put it in writing, walk away.

Questions to Ask Before Hiring

You've narrowed it down to two or three firms. They all claim to be companies that resolve IRS tax debt fast. They sound similar on the phone. Here's how to separate competent representation from commissioned salespeople.

Ask these specific questions:

- "Which licensed professional will personally handle my case, and can I speak with them before signing?"

- "What percentage of your offers in compromise are accepted by the IRS?" (National average is 40%; lower is concerning)

- "Can you explain why my case might not qualify for an offer in compromise?" (If they can't articulate disqualifying factors, they don't understand the program)

- "How do you handle it if the IRS rejects our initial proposal?" (You want a clear appeal or alternative strategy, not a shrug)

- "What happens to my fee if I decide the proposed resolution doesn't work for me?" (Ethical firms have partial refund provisions)

The answers matter less than how they answer. Confident, specific responses backed by examples from similar cases indicate experience. Vague assurances or pivoting to how great their success rate is indicates scripted sales tactics.

Also ask about their experience with your specific issue. Wage garnishment cases require different strategies than unfiled tax returns or payroll tax debt. A firm that handles everything but specializes in nothing might not be the best fit for complex situations.

DIY vs. Professional Representation: When to Hire Help

You can request an installment agreement directly through the IRS website in about 20 minutes. The IRS approves streamlined agreements under $50,000 almost automatically if you're current on filing obligations. You can save $2,500 in professional fees by filling out the online form yourself.

You probably don't need a tax professional if:

- You owe less than $25,000

- Your income and expenses are straightforward W-2 employment

- You haven't received a levy or lien notice

- You can afford the monthly payment the IRS calculator suggests

- You're not disputing the underlying tax assessment

You probably do need professional help if:

- You owe more than $50,000

- You're self-employed or have business tax debt

- The IRS has already started enforcing collection through levies or garnishments

- You can't afford the standard installment payment amount

- You have unfiled returns for multiple years

- You're considering an offer in compromise

- You're facing criminal tax investigation

- Your case involves innocent spouse relief or injured spouse claims

The typical tax resolution process timelines show that complex cases benefit dramatically from experienced representation, while simple agreements don't justify the cost.

Regional Representation vs. Nationwide Firms

The IRS is a federal agency. Your tax attorney doesn't need to be in the same state, though some taxpayers prefer working with local counsel. Nationwide firms often have more resources and specialized staff for different resolution types. Regional firms often provide more personalized service and direct attorney access.

Neither is inherently better. What matters is the individual professional handling your case and their specific experience with situations like yours. A Tampa-based tax attorney can represent a California taxpayer just as effectively as a Los Angeles firm because all communication with the IRS happens via phone, fax, and mail regardless of geography.

If you're in the Tampa area and prefer face-to-face meetings, regional options in Hillsborough County, Pasco County, or Pinellas County provide that option. Most complex tax resolution happens remotely anyway, even with local firms.

How Long Results Actually Take

I told you installment agreements take 30-60 days and offers take 6-12 months. But that's processing time after submission. The total timeline includes preparation.

Full timeline from initial consultation to resolution:

- Week 1-2: Initial consultation, document gathering, IRS transcript requests

- Week 3-4: Financial analysis, strategy development, engagement letter signing

- Week 5-6: Power of attorney filing, stopping active enforcement if necessary

- Week 7-10: Preparation of resolution proposal and supporting documentation

- Week 11-12: Submission to IRS

- Week 13-26+: IRS review, response to additional information requests, negotiation

An "easy" case might resolve in 8 weeks total. A complex offer in compromise with asset disputes and multiple tax years might take 14 months. Companies that resolve IRS tax debt fast can accelerate the preparation and submission phases but can't control IRS processing time.

The 2026 IRS tax debt help tool helps taxpayers understand realistic expectations for their specific situation before engaging professional help, which prevents disappointment when the promised "fast resolution" takes six months.

What Actually Makes Resolution Fast

Speed comes from three things: stopping active enforcement immediately, submitting complete and accurate documentation the first time, and knowing which IRS employees to contact about specific issues.

A competent representative should be able to get a levy released or a wage garnishment stopped within one week by contacting the assigned revenue officer (if one exists) or the automated collection system and negotiating a temporary hold pending resolution. That's the "fast" part that matters when your bank account is frozen.

The actual resolution-whether it's an installment agreement, an offer, or currently not collectible status-takes as long as it takes because the IRS has statutory review requirements and processing queues that no amount of phone calls will shortcut. What professional representation prevents is resubmissions, rejections for missing documentation, and procedural errors that restart the clock.

After 32 years of this work, I can tell you the difference between a case that resolves in three months and one that drags for a year usually comes down to complete financial disclosure up front and accurate calculations the first time. The IRS doesn't move fast, but they move faster when you give them exactly what they need to make a decision.

The companies that resolve IRS tax debt fast aren't magic-they're experienced professionals who know IRS procedures, prepare complete submissions, and stop enforcement quickly when necessary. Whether you need an installment agreement, an offer in compromise, or currently not collectible status depends entirely on your financial situation, not marketing promises. The Law Offices of Darrin T. Mish, P.A. has spent 32 years navigating exactly these issues for taxpayers nationwide, resolving more than $100 million in IRS debt through complete financial analysis and accurate representation. If you're dealing with IRS collection enforcement or trying to figure out which resolution path fits your situation, let's talk-Law Offices of Darrin T. Mish, P.A. offers free initial consultations to assess your specific case and explain realistic options in plain English.