Knowledge is protection when the IRS is involved. I'm Darrin Mish, a tax attorney in Tampa with 32 years of experience representing taxpayers nationwide. Here's what I want you to understand.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

You opened your paycheck and 25% was gone. The IRS sent the levy notice to your employer weeks ago, and now every pay period bleeds money you need for rent, groceries, your car payment. The panic is real because the garnishment doesn't stop on its own-it continues until the debt is paid or you take specific action. The good news: wage garnishment IRS stop options exist, but they require immediate action and the right approach.

How IRS Wage Garnishment Actually Starts

The IRS doesn't garnish wages without warning. You received multiple notices first-probably four or five letters over several months. The first was a balance due notice. Then came increasingly urgent collection letters. The final notice before garnishment is typically a CP-504 or Letter 1058, titled "Final Notice of Intent to Levy and Notice of Your Right to a Hearing."

That final notice gives you 30 days to respond. Most people ignore it, thinking it's another threat letter. It's not.

Once those 30 days expire, the IRS can legally garnish your wages without further warning. They send Form 668-W directly to your employer. Your boss has no choice-federal law requires compliance within one pay period.

The Garnishment Calculation No One Explains

The IRS doesn't take a flat 25%. They take everything above a protected amount based on your filing status and dependents. For a single person with no dependents in 2026, that protected amount is roughly $400 per week. Earn $1,200 weekly? They take $800.

That's not 25%-that's 66%.

Married with three kids? Your protected amount increases to maybe $800 weekly. But if you're the sole earner bringing home $2,000 biweekly, they still take $600. The math is brutal because the IRS wage garnishment formula leaves you with subsistence-level income regardless of your actual obligations.

Five Ways to Stop Wage Garnishment IRS Enforcement

Every wage garnishment IRS stop strategy requires documentation and follow-through. The IRS releases a levy only when you give them something better-a payment arrangement, proof you can't pay, or full satisfaction of the debt.

Pay the Full Balance

The fastest wage garnishment IRS stop method is paying everything you owe. The levy releases within days, usually after the payment clears. But if you had that cash available, you probably wouldn't be reading this. Most people facing garnishment don't have $30,000 sitting around.

Still, it's worth checking if you can borrow the money at a lower cost than continuing the garnishment. A 401(k) loan or family assistance might be cheaper long-term than losing 60% of your income for months.

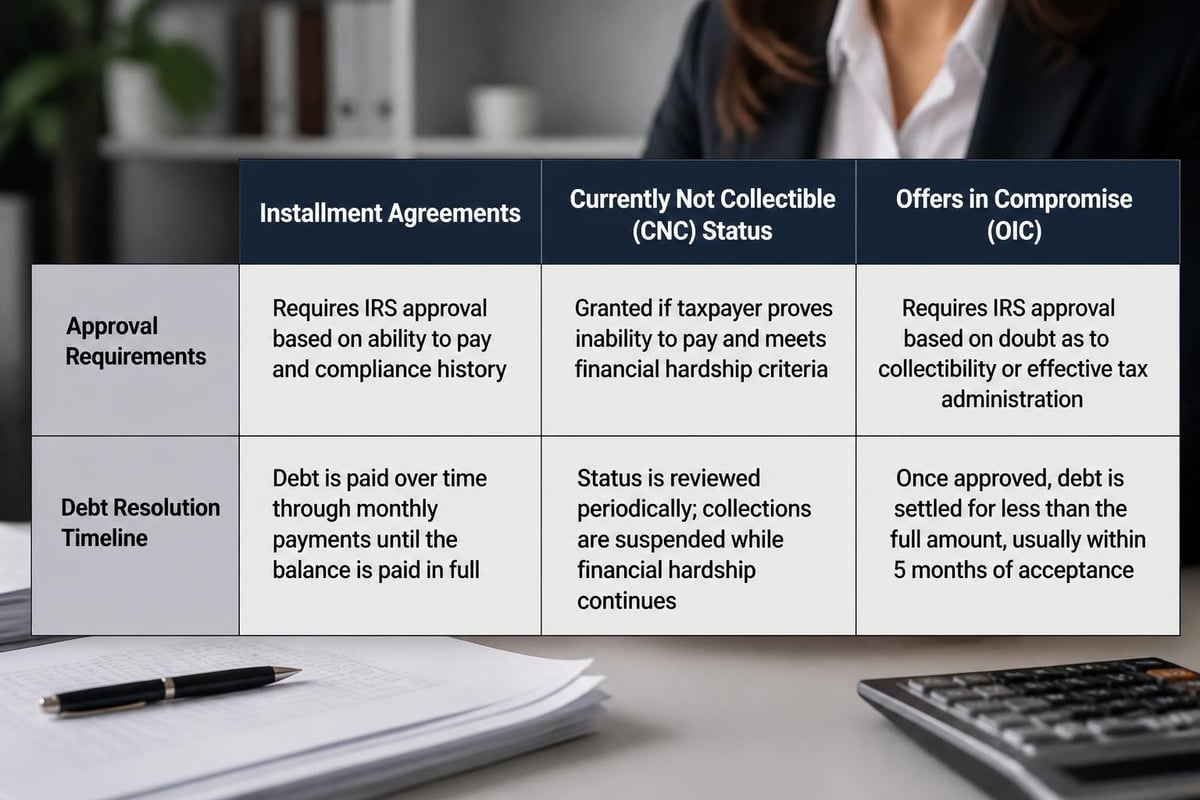

Set Up an Installment Agreement

An installment agreement tells the IRS you'll pay monthly over time. Once approved, they release the wage garnishment within one to two pay cycles. The IRS prefers predictable monthly payments over garnishment because it's administratively easier for them.

You need to propose a realistic monthly amount. The IRS uses financial standards to verify you can afford what you're offering. Low-ball offers get rejected. Aggressive offers you can't sustain get you right back into default.

| Agreement Type | Debt Limit | Approval Process | Release Speed |

|---|---|---|---|

| Streamlined IA | Under $50k | Quick approval, minimal docs | 1-2 pay periods |

| Standard IA | $50k+ | Full financial disclosure | 2-4 weeks |

| Partial Payment IA | Any amount | Detailed financials, IRS review | 3-6 weeks |

The streamlined option works for balances under $50,000 and requires less documentation. You can often set it up online through the IRS website. For larger balances, you'll submit Form 9465 and complete Form 433-F showing income, expenses, assets, and debts.

Request Currently Not Collectible Status

If you genuinely can't pay anything-your income barely covers necessities-you can request Currently Not Collectible (CNC) status. The IRS verifies your financial hardship through Form 433-F and supporting documents like pay stubs, bank statements, and expense receipts.

CNC stops all collection activity, including wage garnishment. But the debt doesn't disappear. Interest and penalties continue accruing. The IRS revisits your financial situation annually and can restart collection if your situation improves.

Currently Not Collectible status works best when you're facing temporary hardship-medical crisis, job loss, family emergency. It buys time without requiring monthly payments.

File an Offer in Compromise

An Offer in Compromise settles your tax debt for less than you owe. The IRS accepts offers when they determine they'll never collect the full amount. You prove through detailed financials that your reasonable collection potential is less than the debt.

Getting an offer accepted while under wage garnishment is harder because the garnishment proves you have income. But filing the offer triggers an automatic stay-the garnishment stops while the IRS evaluates your application. That evaluation takes six to twelve months.

If rejected, the garnishment resumes. If accepted, you pay the settlement amount and the debt disappears. Success requires accurate financial disclosure and a compelling case that you can't pay the full balance even over time.

Request a Collection Due Process Hearing

If you're still within 30 days of receiving the final notice (Letter 1058 or CP-504), you can request a Collection Due Process (CDP) hearing by filing Form 12153. This triggers an automatic stay-the IRS cannot start or continue wage garnishment while your hearing is pending.

The CDP hearing happens with an independent appeals officer, not the revenue officer pursuing collection. You get to argue for alternative collection methods, challenge the underlying tax liability if you haven't had a prior opportunity, or present evidence the levy creates economic hardship.

The problem: most people miss the 30-day window. Once it's gone, you can still request an equivalent hearing using the same form, but it doesn't automatically stop collection. Understanding your rights during IRS collection means acting within those narrow timeframes.

What Doesn't Work for Wage Garnishment IRS Stop

The internet is full of bad advice. Some tactics delay collection temporarily. Others make your situation worse.

Ignoring the Garnishment

The wage levy doesn't expire. It continues until the debt is satisfied, the statute of limitations runs (ten years from assessment), or you take formal action to stop it. Hoping it goes away guarantees it won't.

Quitting Your Job

Some people quit to escape garnishment. The levy follows you to your next employer. The IRS simply sends Form 668-W to the new company once they discover where you're working-usually through tax return filings, new hire registries, or credit bureau data.

You've now lost income with no job and still face garnishment at your next position. It's one of the worst possible responses.

Filing Bankruptcy Without Understanding the Discharge Rules

Chapter 7 or Chapter 13 bankruptcy triggers an automatic stay that stops wage garnishment immediately. But not all tax debt discharges in bankruptcy. Income taxes discharge only if they meet specific timing requirements: the tax return was due at least three years ago, you filed it at least two years ago, and the IRS assessed the tax at least 240 days before your bankruptcy filing.

Penalties and interest on dischargeable taxes also discharge. But recent taxes, payroll taxes, and fraud penalties survive bankruptcy. You stop the garnishment temporarily, but the debt may remain.

Bankruptcy and tax debt is complicated. Filing without understanding the discharge rules wastes money on attorney fees and court costs while leaving you with the same IRS problem.

Negotiating With Your Employer

Your employer has no authority to reduce or stop the garnishment. They received a federal levy order. Compliance is mandatory. Some employers will work with you on timing-holding the garnishment until after the first paycheck to give you time to resolve it-but they risk penalties for non-compliance.

Talk to the IRS, not your boss. Your employer is legally obligated to send the money.

The Timing Problem Most People Miss

Wage garnishment IRS stop strategies work best before the garnishment starts. Once it's active, you're fighting uphill because the IRS already has reliable income access.

That 30-day window after the final notice is your best opportunity. File for a CDP hearing, set up an installment agreement, or request CNC status. Any of these actions taken during those 30 days prevents the garnishment from starting.

After the garnishment begins, you can still do all of those things-but resolution takes longer. The IRS has less incentive to negotiate quickly because they're already collecting.

The Multiple Pay Period Gap

You contact the IRS today and set up an installment agreement. Great. The garnishment doesn't stop until the IRS processes your agreement, issues a levy release, sends it to your employer, and your employer implements the release. That's two to four pay periods minimum.

You just lost $3,200 to $6,400 depending on your wage garnishment amount. Acting earlier saves that money.

How Much Does Professional Help Actually Cost?

Hiring a tax attorney to stop wage garnishment ranges from $1,500 to $5,000 depending on complexity. That sounds expensive until you calculate garnishment losses. If the IRS is taking $1,000 per paycheck biweekly, professional help that stops it one month sooner saves $2,000.

We've resolved more than $100 million in IRS debt over 32 years. Most wage garnishment cases resolve within 30 to 90 days through installment agreements or Currently Not Collectible status.

The calculation is simple: compare attorney fees to continued garnishment losses plus the value of your time and stress dealing with IRS bureaucracy. For many taxpayers, professional help is cheaper even purely financially.

Financial Hardship Documentation the IRS Actually Reviews

Claiming hardship isn't enough. You prove it with numbers. The IRS uses national and local expense standards to evaluate your financial situation. They don't care what you actually spend on groceries-they care what their tables say is reasonable for your family size.

Required documentation includes:

- Three months of pay stubs

- Three months of bank statements

- Current bills and expense records

- Mortgage or rent agreements

- Vehicle loan statements

- Medical bills and necessary expenses

- Form 433-F (Collection Information Statement) completed accurately

The IRS compares your income to necessary living expenses using their standards. If your actual rent is $2,500 but their local standard is $1,800, they allow only $1,800. Discretionary spending gets eliminated. Cable TV, streaming services, gym memberships-all gone in their calculation.

Your disposable income is what remains after allowed expenses. That's what they expect you to pay monthly toward the tax debt. If nothing remains, you qualify for Currently Not Collectible or a partial payment installment agreement.

The Garnishment Release Timeline Nobody Tells You

You've arranged an installment agreement or CNC status. When does the wage garnishment actually stop? The IRS issues a levy release (Form 668-D) and faxes it to your employer. Most employers process it within one pay period, but they're not legally required to rush.

Some employers take two or three pay cycles to implement the release. You can't force them to move faster. The law requires compliance with the levy-it doesn't mandate speed on the release.

| Action Taken | IRS Processing | Employer Implementation | Total Time to Stop |

|---|---|---|---|

| Installment Agreement | 1-3 days | 1-2 pay periods | 1-3 weeks |

| CNC Status | 3-7 days | 1-2 pay periods | 2-4 weeks |

| Offer in Compromise | Same day (stay) | 1-2 pay periods | 1-3 weeks |

| CDP Hearing Request | 2-5 days | 1-2 pay periods | 1-3 weeks |

The fastest releases happen with installment agreements because they're processed automatically once approved. CNC status requires manual review, which takes longer. Offers trigger an immediate stay but require mailing or faxing to the employer.

State Tax Wage Garnishment Works Differently

This article focuses on federal wage garnishment IRS stop methods, but state tax authorities can also garnish wages. Each state has different procedures, protected amounts, and release processes.

Florida has no state income tax, so if you're in Tampa, you only worry about federal garnishment. But if you owe other states-maybe from years you lived elsewhere-those states can garnish your Florida wages. California, New York, and other high-tax states pursue collection aggressively.

State garnishment usually takes less than federal-often 10% to 25% depending on state law. But you face the same resolution options: payment plans, hardship status, or settlement. The procedures and forms differ by state.

When Garnishment Affects Security Clearance or Professional Licenses

Some careers face additional consequences from IRS wage garnishment. Security clearances require financial responsibility. Active garnishment for tax debt raises red flags during clearance reviews and renewals. It doesn't automatically disqualify you, but it requires explanation and demonstration that you're resolving the debt.

Professional licenses in accounting, law, real estate, and financial services can be suspended or revoked in some states for unresolved tax debt. The IRS shares information with state licensing boards. An active wage garnishment signals serious tax problems that licensing authorities may view as professional misconduct.

Resolving tax debt quickly becomes critical if your job or license depends on financial good standing. An installment agreement shows you're addressing the problem responsibly even if you can't pay immediately.

The Penalty and Interest Problem During Garnishment

While your wages are being garnished, penalties and interest continue accruing on the unpaid balance. The garnishment applies first to penalties, then interest, finally principal. For a $30,000 debt, it might take six months of garnishment just to cover accrued penalties and interest before touching the actual tax owed.

The combined penalty and interest rate runs about 8% annually in 2026. On $30,000, that's $2,400 per year. Your wage garnishment needs to exceed $200 monthly just to keep pace with new charges.

This is why wage garnishment IRS stop strategies matter even if you plan to eventually pay the full debt. An installment agreement stops penalties (though interest continues). An Offer in Compromise eliminates both if accepted. Even CNC status prevents new penalties while active.

Letting garnishment run its course maximizes your total payment because penalties and interest compound throughout the collection period.

Multiple Tax Years Create Garnishment Complications

The IRS garnishes for all tax years simultaneously. If you owe for 2022, 2023, and 2024, one wage levy covers everything. The total debt might be $75,000 across three years. Setting up payment arrangements requires addressing all years together.

Some taxpayers have unfiled returns for additional years. The IRS won't approve installment agreements or Offers in Compromise while you have unfiled returns. You must file all required returns first, even years you can't pay. Filing unfiled returns becomes a prerequisite to wage garnishment release.

The IRS applies garnished wages to the oldest tax year first, then works forward. But if you owe trust fund taxes from a business payroll-those always get priority over personal income taxes. Trust fund recovery penalties jump to the front of the payment line.

After Garnishment Stops: Staying in Compliance

You've stopped the wage garnishment through an installment agreement. Now you need to stay compliant or the agreement defaults and garnishment resumes. Compliance means two things: making every monthly payment on time and filing all future tax returns on time with full payment.

Miss one installment payment? The agreement defaults. File your 2026 return late or with a balance due? The agreement defaults. Default means the IRS can immediately garnish wages again without sending new notices. You lost your one chance.

The IRS is absolutely rigid on compliance. Set up automatic payments from your bank account. Don't rely on memory or manual payments. One forgotten payment costs you everything.

Wage garnishment IRS stop strategies work, but they require immediate action and accurate financial disclosure. The IRS releases levies when you give them a better collection method or prove legitimate hardship. For 32 years, the Law Offices of Darrin T. Mish has stopped wage garnishments and resolved tax debt for clients nationwide-more than $100 million in IRS debt negotiated down or eliminated. If your paycheck is being garnished or you've received a final levy notice, let's talk before you lose another pay period to the Law Offices of Darrin T. Mish, P.A.