If you've got an IRS letter on your desk right now, you have a decision to make, and the clock matters. I'm Darrin Mish. I've spent 32 years helping people with exactly this kind of situation. Here's what you should do.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

A CP2000 notice lands in your mailbox claiming you underreported income by thousands of dollars. Your stomach drops. The number looks wrong, the math doesn't match your records, and the IRS wants payment within 30 days. You need a cp2000 disagree response letter sample, but more than that, you need to understand what actually makes the IRS reverse these assessments. Template letters from the internet won't cut it-you need a response built on your specific facts, with evidence the IRS can't dismiss.

The IRS issues CP2000 notices when their computers find a mismatch between what third parties reported (W-2s, 1099s, K-1s) and what you claimed on your return. It's not an audit. It's an automated proposal based on data matching. The good news: you can challenge it without setting foot in an IRS office. The bad news: if you ignore it or write a vague protest, the assessment becomes final.

Understanding What Triggers a CP2000 Notice

The IRS receives information returns from every bank, brokerage, employer, and client who paid you more than the reporting threshold. A computer program called the Automated Underreporter (AUR) system compares those third-party reports to Line 1 through Line 8 of your Form 1040. Any discrepancy over a certain dollar amount generates a notice.

Common triggers include 1099-INT for interest you forgot to report, 1099-B for stock sales where you only reported net proceeds instead of gross, or Schedule K-1 income that didn't make it onto your return. Sometimes the third party made the mistake-reported the same income twice, assigned income to the wrong tax year, or issued a corrected form you never received. Sometimes you made the mistake. Either way, the burden falls on you to explain the discrepancy with documentation the IRS accepts.

The 30-Day Window Is Real

From the date printed on your CP2000 notice, you have 30 days to respond. Not postmarked-by-30-days. Not approximately a month. Thirty calendar days. Miss that window and you get a Statutory Notice of Deficiency (also called a 90-day letter), which starts the clock on your right to petition Tax Court. Understanding how to respond properly within that timeframe prevents escalation.

If you need more time, you can request an extension, but you need to request it before the 30 days expire. The IRS usually grants 30 additional days if you ask. That gives you time to gather records, reconstruct basis, or track down corrected forms from the issuer.

Building Your CP2000 Disagree Response Letter

A cp2000 disagree response letter sample needs to accomplish three things: identify the specific line items you dispute, explain why the IRS calculation is wrong, and provide documentation that proves your position. The IRS receives millions of these responses. Yours needs to be clear enough that a processor in Fresno or Kansas City can resolve it without requesting more information.

Start with your identifying information in the upper right corner: your name as shown on the return, Social Security number, tax year, and the CP2000 notice number (usually starts with "CP2000" followed by a long string of numbers). The IRS uses this to match your response to the notice in their system.

Opening Statement and Scope of Disagreement

Your first paragraph states that you disagree with the proposed changes and identifies which items you're disputing. Be specific. "I disagree with all proposed changes" is too vague. "I disagree with the proposed unreported income of $8,450 from ABC Financial (1099-INT) and the $12,300 adjustment for XYZ Brokerage (1099-B)" tells the processor exactly what to review.

If you agree with some items but not others, say so. Partial agreement speeds up processing. The IRS can accept the agreed items and focus on the disputed ones.

| Response Type | What It Means | Processing Time |

|---|---|---|

| Full Agreement | You owe the amount stated | Immediate assessment |

| Full Disagreement | You dispute all proposed changes | 60-120 days review |

| Partial Agreement | Some items correct, others wrong | 45-90 days review |

Line-by-Line Explanation Section

For each disputed item, create a separate paragraph or numbered section that follows this structure:

- Item identification: Reference the payer name, form type, and amount exactly as shown on the CP2000 notice

- Your position: State what the correct treatment should be

- Supporting explanation: Explain why with specific facts

- Evidence reference: Point to the attached documentation

For example: "The CP2000 notice includes $15,000 from Form 1099-B issued by Schwab for the sale of 500 shares of Tesla stock. This amount represents gross proceeds, not taxable gain. My original cost basis was $12,000, documented on the attached purchase confirmations from 2024. The correct taxable gain is $3,000, which was properly reported on Schedule D, Line 8b. See attached: original brokerage statements showing purchase date and price, and Schedule D from my filed return."

Documentation That Actually Works

The IRS doesn't take your word for it. They need third-party verification or contemporaneous records. Bank statements showing you already paid tax on rollover income that generated a 1099-R. Brokerage statements showing the cost basis the 1099-B left blank. A letter from the payer acknowledging they issued a corrected form.

Canceled checks don't prove income wasn't taxable-they prove you received money. To exclude income from your return, you need documentation showing why it wasn't taxable. IRA contribution proof to offset a 1099-R distribution. A trustee's letter explaining a 1099-INT reported interest on a trust where you weren't the beneficial owner. Form 8606 showing basis in a Roth conversion.

What Counts as Adequate Support

Strong documentation is specific, dated, and comes from a neutral source. A self-prepared spreadsheet claiming you tracked cost basis in Bitcoin transactions won't carry much weight. Exchange transaction histories showing purchase dates, amounts, and sales with matching trade IDs will.

- Bank statements: Prove deposits, withdrawals, and dates

- Brokerage confirmations: Show purchase price, sale price, dates, and transaction fees

- Corrected 1099s: Must come from the original issuer on their letterhead

- Professional appraisals: For property basis, charitable contributions, casualty losses

- Prior year returns: Show carryover amounts, NOLs, or basis adjustments

Organize documents in the order you reference them in your letter. If your letter discusses five disputed items, attach five tabs or sections labeled to match. The processor shouldn't have to hunt through a pile of papers to find your proof.

Common CP2000 Disputes and How to Handle Them

Some scenarios appear in nearly every CP2000 response pile. Understanding how the IRS views these situations helps you craft a response that aligns with their procedures rather than fighting against them.

Missing Cost Basis on Stock Sales

Brokerages started reporting cost basis to the IRS in 2011 for stocks, 2012 for mutual funds, and 2014 for options. Sales of securities purchased before those dates often show up on 1099-B forms with blank basis fields. The IRS computer assumes zero basis and proposes taxing the entire proceeds amount.

Your response needs to establish basis through purchase confirmations, year-end statements from the year of purchase, or transaction histories. If you inherited the stock, you need the date-of-death value. If you received it as a gift, you need the donor's basis and proof of the gift date. Generic statements like "I paid $10,000 for these shares" won't work-you need documentation showing when and at what price.

Duplicate Income Reporting

Sometimes two 1099 forms report the same income-an original and a corrected version, or separate reports from a company merger where both entities reported the same payment. Your response needs to explain the duplication and provide copies of both forms showing identical income with different form numbers or issuers.

A letter from the payer confirming the duplication helps, though the IRS may accept your explanation with copies of both 1099s if the amounts and dates clearly match. When dealing with income reporting disputes, documentation consistency matters more than volume.

Income Reported in the Wrong Year

You received a January 2026 payment for December 2025 services. The payer issued a 2026 Form 1099-MISC. You reported it on your 2025 return using the accrual method. The IRS computer sees 2026 income missing from your 2026 return.

Your response explains your accounting method, cites the relevant tax code section (usually IRC Section 451 for accrual method taxpayers), and provides your 2025 return showing the income reported and your business accounting records showing the accrual. Most processors understand this once you explain it clearly.

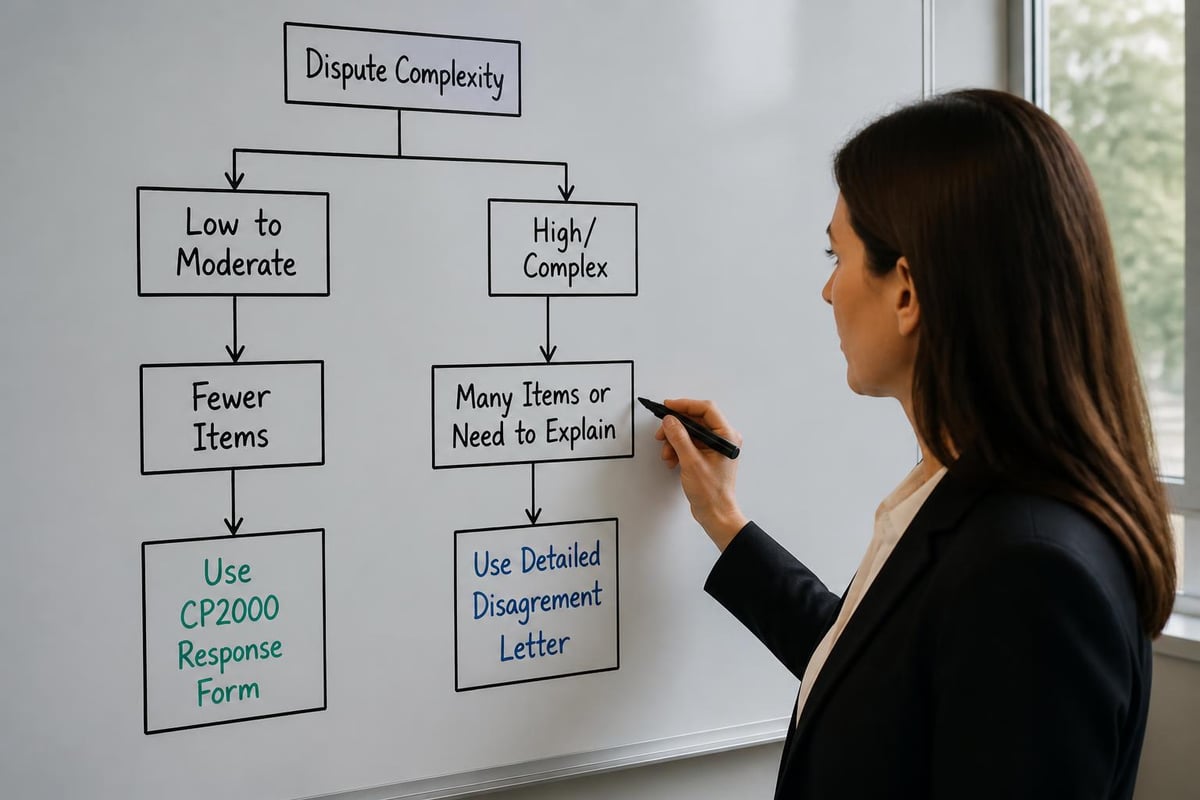

The CP2000 Response Form Alternative

Instead of writing a full disagree letter, you can use the response form included with your CP2000 notice. It has checkboxes for "agree," "disagree," and "partially agree," with space for a brief explanation. This works fine for simple disputes-one or two items with straightforward explanations and clear documentation.

For complex situations involving multiple disputed items, calculations spanning several forms, or arguments requiring detailed explanation of tax law, a separate letter gives you room to build a complete case. The IRS provides guidance on completing the response form, but nothing prevents you from attaching additional pages to that form.

| Scenario | Response Form | Separate Letter |

|---|---|---|

| Single item, clear error | Best choice | Unnecessary |

| 2-3 items, simple explanations | Works well | Optional |

| Multiple items, complex facts | Inadequate space | Recommended |

| Legal arguments needed | Too limited | Required |

Combining Form and Letter

Many effective responses use both: check the "disagree" box on the form, write "see attached explanation" in the comments section, and attach a detailed letter with supporting documents. This ensures the IRS system logs your response type correctly while giving you space to make your full argument.

Mailing and Tracking Your Response

Send your response by certified mail with return receipt requested to the address shown on your CP2000 notice. The IRS has different processing centers for different regions-using the wrong address can delay your response by months. The correct address appears in the "If you disagree" section of your notice, not the return address on the envelope.

Keep copies of everything. Your letter, every page of supporting documents, the certified mail receipt, and eventually the return receipt showing the IRS received it. Processing can take 60 to 120 days depending on the complexity of your dispute and the backlog at the processing center. During that time, you may receive additional notices-some automated, some requesting more information.

Don't panic if you get a follow-up letter asking for clarification or additional documents. It means a human processor is reviewing your case. Respond promptly with exactly what they request. Each round of correspondence adds 30 to 60 days to resolution time.

What Happens After You Respond

The IRS assigns your response to an examiner who reviews your explanation and supporting documents. If your documentation clearly establishes your position, they'll issue a closure letter showing no additional tax due. If they need more information, they'll send a request. If they disagree with your position, they'll send an explanation and give you another opportunity to respond.

In some cases, the examiner accepts part of your response but maintains some adjustments. You'll receive a revised CP2000 showing the reduced assessment. You can agree to that amount, continue disputing, or explore payment options like installment agreements if you can't pay the remaining balance immediately.

When the IRS Requests Additional Information

Information requests typically give you 30 days to respond. They'll specify exactly what they need-more documentation for a particular item, clarification of your accounting method, or explanation of a discrepancy between your records and third-party reports. Treat this as seriously as the original response. Failure to respond results in default assessment.

If you genuinely don't have the requested documentation (records destroyed in a fire, ancient stock purchased decades ago with no surviving records), explain that in writing and provide whatever alternative evidence you can. The IRS has provisions for establishing basis through reasonable reconstruction when original records are unavailable, but you need to make that argument explicitly.

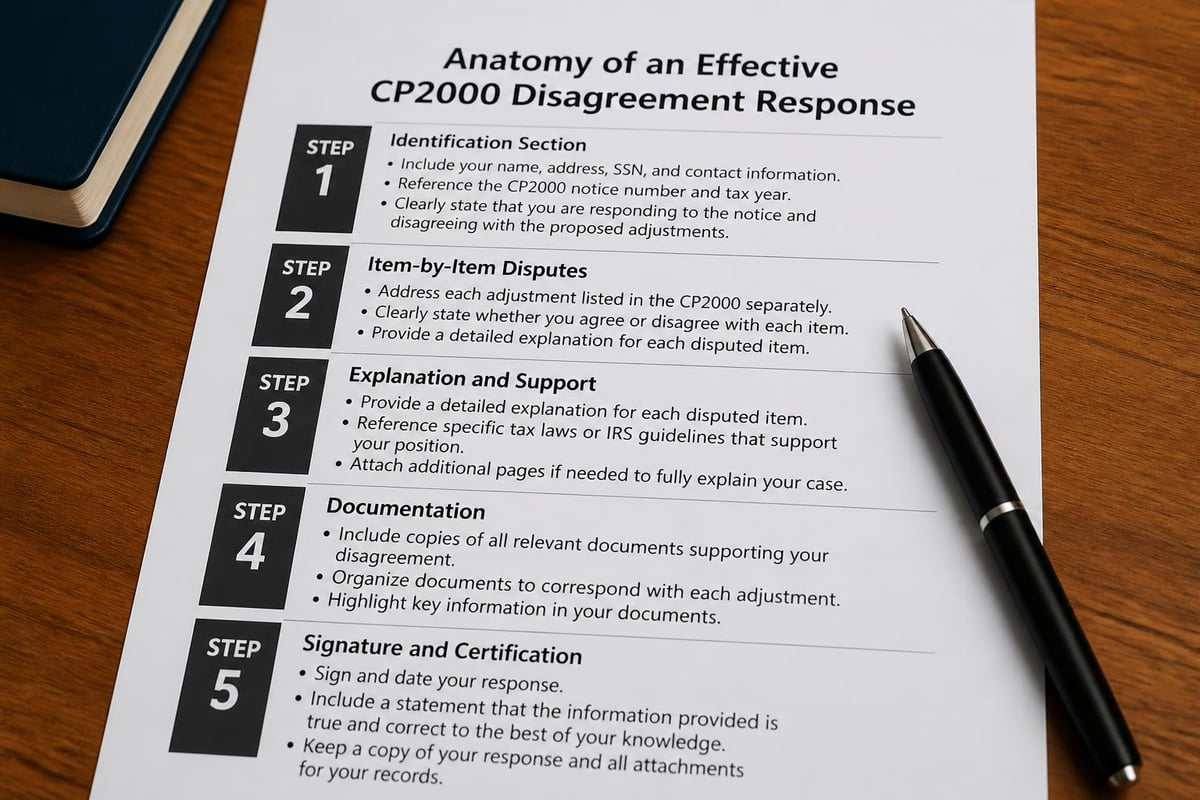

Sample CP2000 Disagree Response Letter Structure

A complete cp2000 disagree response letter sample follows this outline:

Header Section:

- Your name and SSN

- Tax year in question

- CP2000 notice number and date

- Current date

- IRS mailing address from notice

Opening Paragraph:

"I received CP2000 Notice [number] dated [date] proposing additional tax of $[amount] for tax year [year]. I disagree with the proposed changes for the reasons explained below."

Item-by-Item Dispute Section:

For each disputed item:

- Payer name and form type

- Amount IRS proposes to add

- Your position on correct treatment

- Factual explanation

- Reference to supporting documents

Supporting Documents Reference:

"I have attached the following documentation in support of my position:

- Tab 1: [description]

- Tab 2: [description]"

Closing Paragraph:

"Based on the explanation and documentation provided, I request that you adjust the proposed assessment to reflect the correct amounts. Please contact me if you need additional information."

Signature Block:

Your signature, printed name, phone number, and date

Penalty Abatement Opportunities

If you end up owing some tax after the CP2000 resolution, the IRS automatically calculates penalties and interest from the original due date of the return. For many taxpayers, the penalties exceed the underlying tax. You can request penalty abatement separately if you have reasonable cause for the underreporting.

First-time penalty abatement applies if you haven't had penalties in the prior three years and you've filed all required returns. It's administrative relief-the IRS can grant it without detailed reasonable cause arguments. For accuracy-related penalties on CP2000 assessments, reasonable cause usually involves reliance on incorrect information from third parties, complexity of tax law, or illness and hardship during the filing period.

Professional Help With Complex CP2000 Disputes

Simple disputes-a missing 1099 you can document, a duplicate form, clear basis records-you can handle yourself with a well-written response. Complex situations involving business income, investment transactions across multiple accounts, foreign income reporting, or disputes over multiple tax years benefit from professional representation.

A tax attorney or CPA experienced with IRS audit defense knows what arguments work with specific types of income, how to present documentation in the format IRS processors expect, and when to escalate to appeals rather than continuing with the examination division. Before responding to a CP2000 notice, understanding your options prevents costly mistakes.

The cost of representation needs to balance against the tax at stake. For a $2,000 proposed adjustment you can clearly disprove with documentation you already have, paying a professional $1,500 doesn't make economic sense. For a $45,000 adjustment involving complex partnership K-1 allocations, stock option exercises, and multi-year carryovers, professional help pays for itself.

State Tax Implications

Federal CP2000 adjustments flow through to your state return if your state uses federal adjusted gross income as its starting point. Most states do. If the IRS assessment becomes final, expect your state to issue a similar adjustment notice 6 to 18 months later. Some states have information-sharing agreements that trigger automatic state adjustments.

Your federal CP2000 response should protect both federal and state positions. If you successfully dispute the federal adjustment, the state issue disappears. If you partially agree, you'll need to file an amended state return reflecting the changes. State tax implications vary by jurisdiction, but the federal response drives the state outcome.

Getting a CP2000 notice right means building a response on facts and documentation, not hope and vague protests. If your situation involves multiple disputed items, complex income types, or significant tax at stake, getting it wrong costs you appeal rights and potentially years of payment plans. For 32 years, I've walked taxpayers through CP2000 responses that work-clear arguments, organized evidence, and explanations the IRS actually accepts. Let's talk about your specific notice and build a response that holds up. Law Offices of Darrin T. Mish, P.A. handles CP2000 disputes nationwide with free initial consultations-we'll review your notice and tell you exactly where you stand.