Most people I talk to about their IRS problem have already built the worst-case scenario in their head. The reality is usually much more manageable. I'm Darrin Mish, and I've been representing taxpayers before the IRS for 32 years. Here's what actually tends to happen.

I'm Darrin Mish. Tampa tax attorney, 32 years in, more than $100 million in IRS debt resolved. What follows isn't theory – it's what I've actually watched work.

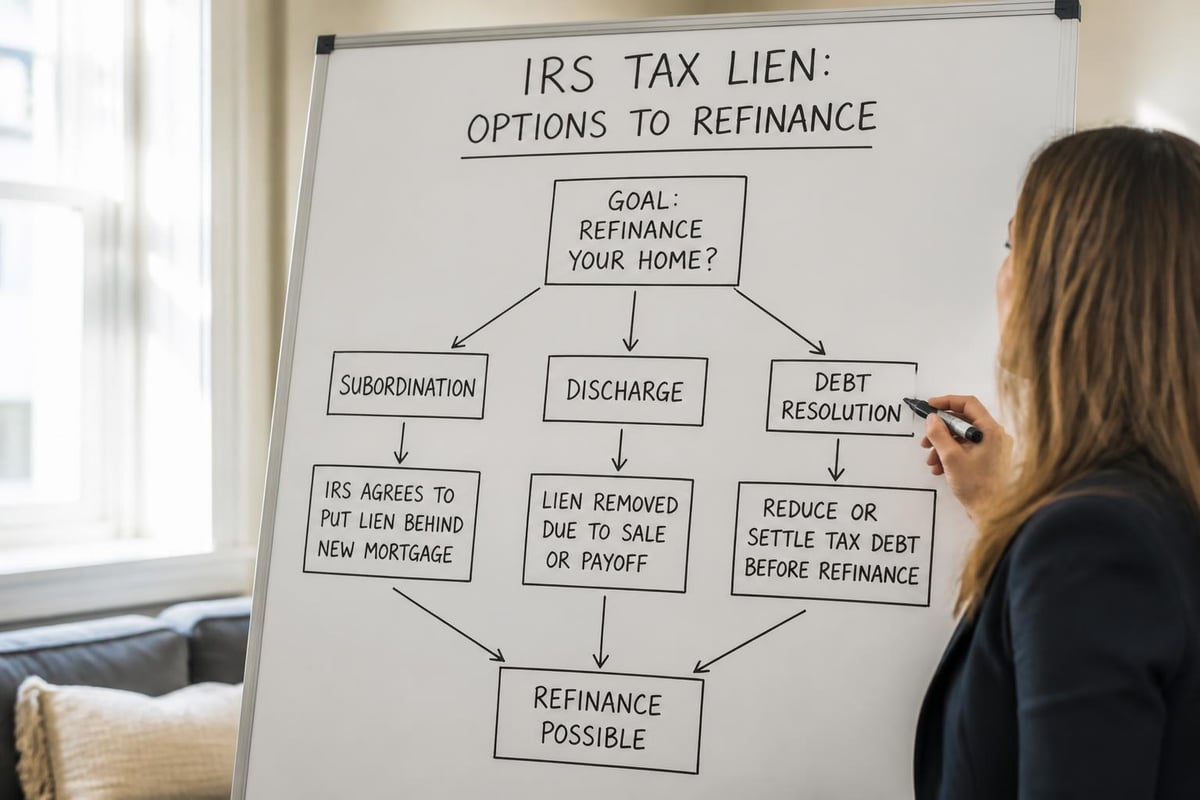

You owe the IRS. They filed a Notice of Federal Tax Lien against your property. Now you need to refinance your mortgage, but no lender will touch the deal because the IRS has priority over everything. An IRS lien subordination refinance mortgage transaction can solve this-if you know how it works and meet the requirements.

Subordination doesn't erase the lien. It doesn't reduce what you owe. It just lets the new mortgage lender step ahead of the IRS in line, which is exactly what they need to approve your loan. The IRS still gets paid, but from a position behind your new first mortgage instead of in front of it.

What IRS Lien Subordination Actually Does

When the IRS files a federal tax lien, it attaches to all your property-real estate, cars, bank accounts, future assets. It's public record. First in time, first in right. That lien takes priority over anything filed after it, including new mortgages.

A lender won't refinance your home if they're second in line behind the IRS. They need first position. If you default and they foreclose, they want their money before anyone else touches the sale proceeds.

Subordination changes the order. The IRS agrees to move behind the new lender. Your new mortgage becomes first priority, the IRS drops to second, and the refinance can close. The lien itself stays filed-it's still on record, still attached to your property-but it's no longer blocking the transaction.

This isn't automatic. The IRS won't subordinate just because you ask nicely. They'll only do it when it serves their collection interest, which usually means they're more likely to get paid with the subordination than without it.

When the IRS Will Subordinate a Lien

The IRS has guidelines laid out in Internal Revenue Manual 5.12.10, and they're not flexible. You need to show that subordination will make it easier for the IRS to collect what you owe.

The most common scenario: You're refinancing at a lower interest rate, pulling out equity, and using some of that cash to pay down your tax debt. The IRS looks at the numbers. If they're getting a meaningful payment now, and the subordination doesn't hurt their ultimate collection ability, they'll usually approve it.

They'll also subordinate if the refinance doesn't increase your total debt against the property and doesn't pull out cash that disappears into your pocket. A straight rate-and-term refinance-same balance, lower rate, lower payment-can work if it improves your financial position enough that you can start making payments on the tax debt.

| IRS Subordination Approval Factors | What the IRS Looks For |

|---|---|

| Equity increase | Does the refinance generate cash to pay the IRS? |

| Payment capacity | Will lower monthly payments free up money for tax debt? |

| Lien position safety | Will the IRS still be able to collect if you default? |

| Total debt burden | Are you taking on more debt or reducing it? |

The IRS won't subordinate if you're cash-out refinancing to buy a boat. They won't subordinate if the new loan pushes your total mortgage debt so high that there's no equity cushion left for them. They need to see that they're not worse off after the subordination than before.

The Application Process for Subordination

You'll file Form 14134, Application for Certificate of Subordination of Federal Tax Lien. It's a six-page form that asks for detailed financial information, property valuations, and specifics about the refinance transaction.

You need current documentation. Recent property appraisal, payoff statement from your existing lender, loan estimate from your new lender, and a full financial statement showing income, expenses, assets, and liabilities. The IRS wants proof that the numbers you're claiming are real.

The application goes to the IRS Advisory Group in Covington, Kentucky. They review it. They check your equity position, verify the loan terms, calculate whether subordination makes collection sense. Processing takes 30 to 60 days if everything's complete and accurate. Longer if they need to request additional information.

Steps to File Form 14134

- Get a current property appraisal from a licensed appraiser, dated within the last 90 days

- Obtain a loan estimate from your lender showing the new loan terms, rate, closing costs, and cash-out amount if any

- Request a payoff statement from your current mortgage lender showing the exact balance

- Complete Form 14134 with accurate financial information and attach all supporting documents

- Submit the application to the IRS Advisory Group at least 45 days before your closing date

- Follow up if you don't receive a response within 30 days

Timing matters. Don't wait until three days before closing to file this. Your lender needs the subordination certificate in hand before they'll fund the loan. Start the process as soon as you have a loan estimate and appraisal.

The Taxpayer Advocate Service provides guidance on the subordination process, including common reasons for denial and how to address them. Worth reading before you file.

How Much It Costs and What You Get

The IRS charges a user fee for processing subordination applications. As of 2026, it's $330. You pay it when you submit Form 14134. No refund if they deny your application.

If approved, you'll receive a Certificate of Subordination. It's a formal document stating that the IRS agrees to subordinate its lien to the specific mortgage loan identified in your application. It names the lender, describes the property, and specifies the terms under which the subordination is valid.

Your lender files this certificate with the county recorder's office at closing. It becomes part of the public record, showing that the IRS lien-while still filed-is now junior to the new mortgage.

The certificate is specific to that one transaction. If you refinance again later with a different lender or different terms, you'll need a new subordination application and another $330 fee.

Subordination vs. Discharge vs. Withdrawal

People confuse these terms. They're different tools with different effects.

- Subordination moves the IRS behind another creditor but keeps the lien in place

- Discharge removes the lien from a specific piece of property but keeps it attached to your other assets

- Withdrawal pulls back the public Notice of Federal Tax Lien as if it was never filed

For an irs lien subordination refinance mortgage, you're asking for subordination. You're not asking them to discharge the property or withdraw the lien. You just need them to step back in priority so the lender can take first position.

Discharge makes sense when you're selling property and using the proceeds to pay the IRS. Withdrawal happens after you've paid the debt in full or entered into certain installment agreements. Those aren't refinance scenarios.

When Subordination Won't Work

The IRS will deny subordination if the numbers don't support their collection interest. I've seen denials for several recurring reasons.

Insufficient equity. If your property is worth $300,000, you owe $280,000 on your existing mortgage, and you want to refinance for $290,000, there's only $10,000 in equity. The IRS won't subordinate when there's barely any cushion. They need enough equity that if you default and the property sells in foreclosure, there's a reasonable chance they'll still get something.

Cash-out with no IRS payment. If you're pulling $50,000 in cash out and none of it goes to the IRS, they'll deny the application. Why would they subordinate so you can spend money they could have collected?

Unstable income. If your financial statement shows irregular income, recent job loss, or mounting debt in other areas, the IRS will question whether you can sustain the new mortgage payments. If you can't, the property will eventually sell in foreclosure, and the subordination will have damaged their position for nothing.

| Common Denial Reasons | Why the IRS Says No |

|---|---|

| Minimal equity | Not enough value to protect IRS interest |

| No payment to IRS | Cash-out doesn't benefit tax debt collection |

| Excessive new debt | Total mortgage too high relative to value |

| Poor payment history | Pattern of default or late payments |

You can appeal a denial, but you'll need to address the specific reasons the IRS cited. Sometimes it's a matter of adjusting the loan terms-borrowing less, contributing more to the IRS, or waiting until the property appraises higher.

Refinancing Strategy with an Existing Lien

If subordination is the only way to refinance, you need a clear plan before you apply. Talk to your lender first. Make sure they're willing to do the deal if you can get the subordination certificate. Not all lenders will close a loan secured by property with a federal tax lien, even a subordinated one.

Get pre-approved. Know exactly how much you can borrow, at what rate, with what closing costs. The IRS wants firm numbers on Form 14134, not estimates or guesses.

Consider how much you'll pay toward the tax debt. The more you can contribute from the refinance proceeds, the stronger your subordination application. Even if you're doing a rate-and-term refi with no cash-out, calculate how much your monthly savings will be and show the IRS how that frees up cash for tax payments.

Alternatives to Subordination

Sometimes subordination isn't the best path. If you qualify for an Offer in Compromise, you might be able to settle the debt for less than you owe. Once you pay the accepted offer amount, the IRS releases the lien. Then you can refinance without needing subordination.

If you're current on an installment agreement and your payments are reliably made through direct debit, the IRS might withdraw the lien under the Fresh Start program. No lien means no subordination needed.

If your equity position is strong and you're selling the property, a discharge might make more sense than subordination. The IRS removes the lien from that one property, lets the sale close, and takes their share from the proceeds. Lien discharge procedures apply differently than subordination, but the result-closing the transaction-can be the same.

What Lenders Need from You

Your mortgage lender will have their own requirements separate from the IRS. They'll want proof that the subordination was approved. They'll review the Certificate of Subordination to confirm it matches the loan they're funding. They'll verify that all other title issues are clear.

Expect additional title insurance costs. Insuring a property with a subordinated IRS lien carries more risk for the title company. They'll charge more for the policy, and some won't issue one at all.

Lenders will also scrutinize your overall financial picture more carefully than they would in a standard refinance. You have tax debt. That's a red flag. They need confidence that you can make the new mortgage payments and stay current on your IRS obligations at the same time.

Some lenders specialize in working with borrowers who have tax liens. They understand the subordination process, they've dealt with the IRS before, and they know how to structure deals that get approved. If your regular lender won't touch it, find one who will.

The Equity Calculation That Matters

The IRS bases subordination decisions on equity. You need to understand how they calculate it because their math determines approval or denial.

Equity = Current Fair Market Value – Senior Liens – Selling Costs. Senior liens include any mortgage or lien filed before the IRS lien. Selling costs are typically calculated at 8% to 10% of the property's value-real estate commissions, closing fees, title charges.

If your home is worth $400,000, your first mortgage balance is $250,000, and estimated selling costs are $32,000, your net equity is $118,000. The IRS looks at that number. If you're refinancing for $300,000, your new equity after subordination would be $68,000. That's a meaningful cushion. Approval is likely if the rest of your application is solid.

But if your home is worth $400,000, your first mortgage is $380,000, and selling costs are $32,000, your equity is negative $12,000. The IRS won't subordinate. There's nothing for them to collect.

How Subordination Affects Your Tax Debt

Subordination doesn't reduce your balance with the IRS. It doesn't stop interest from accruing. It doesn't pause the collection statute. It's purely a lien priority tool.

You still owe the full amount. The IRS can still levy your wages or bank accounts. The lien is still attached to all your property, not just the home you're refinancing. Subordination just makes this one transaction possible.

If you use refinance proceeds to pay down the tax debt, that payment applies to your balance like any other payment-interest first, then penalties, then principal. The IRS won't credit it differently because it came from a subordinated refinance.

Working Through the Timeline

Here's the realistic timeline for an irs lien subordination refinance mortgage transaction from start to finish:

- Week 1-2: Lock your interest rate with the lender, get a loan estimate, order the appraisal

- Week 3: Receive the appraisal, obtain the current mortgage payoff statement, gather financial documents

- Week 4: Complete Form 14134, compile all attachments, submit the application to the IRS Advisory Group

- Week 5-10: IRS reviews the application, requests additional information if needed, issues a decision

- Week 11: Receive the Certificate of Subordination, deliver it to your lender and title company

- Week 12: Close the refinance, record the new mortgage and subordination certificate

That's a best-case scenario. If the IRS requests more documentation, if your appraisal comes in low and you need a second opinion, if your lender changes terms midstream, add weeks or months.

Don't let your rate lock expire while you're waiting on the IRS. Budget for an extension or accept that you might need to re-lock at whatever rate is available when the subordination finally comes through.

Professional Help vs. DIY Filing

You can file Form 14134 yourself. It's not a complicated form if your financial situation is straightforward and you're comfortable gathering the required documentation. The IRS doesn't require an attorney or tax professional to submit the application.

But subordination denials are common. If the IRS says no, you've lost time, you've lost the $330 fee, and you're back at square one. If the application was incomplete or the documentation didn't support your case, you'll need to start over with a stronger submission.

I've handled hundreds of lien subordinations. The difference between approval and denial often comes down to how you present the numbers and what explanations you provide. An experienced tax attorney knows what the IRS looks for, can structure the refinance terms to maximize approval odds, and can respond effectively if the IRS raises objections.

If your tax debt is substantial, your equity is marginal, or you've had prior issues with the IRS, get help. The cost of professional representation is usually less than the cost of a failed subordination and a blown refinance opportunity.

Multiple Liens and Subordination

If the IRS has filed more than one lien against you-say, for different tax years-each lien needs its own subordination. Form 14134 covers all periods included in the lien notices, but you need to identify each one specifically.

Sometimes taxpayers have multiple tax debts, some with liens and some without. Only the liened debts require subordination. The IRS won't subordinate unlien debts because there's no lien to subordinate.

If you have state tax liens in addition to federal liens, you'll need subordination from the state taxing authority too. The process varies by state. Some states follow procedures similar to the IRS, others are more difficult to work with. Your lender will require all liens affecting the property to be subordinated or discharged before closing.

| Multiple Lien Scenarios | Required Action |

|---|---|

| Multiple IRS tax years | Include all in single Form 14134 |

| IRS + state tax liens | File separate subordination with each agency |

| Senior private liens | No IRS action needed; already have priority |

| Junior private liens | May need separate subordination agreements |

After the Subordination Is Approved

You've received the Certificate of Subordination. Your closing is scheduled. What happens next?

The certificate is time-sensitive. It's valid for the specific transaction and property identified in the application. If your loan terms change significantly between approval and closing-different loan amount, different lender-the subordination might not cover it. The IRS can revoke the certificate if the actual transaction doesn't match what was approved.

At closing, your title company will record the new mortgage and the subordination certificate simultaneously. The public record will show your new first mortgage with the lender, then the IRS lien in second position. Any future creditors searching the title will see that order.

Your responsibility doesn't end at closing. You still need to address the underlying tax debt. If you used cash-out proceeds to pay the IRS, confirm the payment was properly applied to your account. If you committed to a payment plan as part of the subordination application, stick to it.

What Happens If You Default

If you stop making payments on the new mortgage, the lender will foreclose. They're in first position now, so they get paid first from the sale proceeds. The IRS lien-still attached to the property-gets paid from whatever's left.

If the foreclosure sale brings $400,000 and the mortgage balance is $300,000, the lender takes $300,000 plus foreclosure costs. The remaining $100,000 goes toward your IRS debt. If there's nothing left after the lender is paid, the IRS gets nothing from that property, but the lien remains attached to your other assets.

Subordination doesn't limit the IRS's other collection tools. They can still levy your bank accounts, garnish your wages, or seize other property. The lien stays active until the debt is paid in full or the collection statute expires.

Rate and Term vs. Cash-Out Refinancing

The type of refinance affects your subordination odds. A rate-and-term refinance-where you're just lowering your interest rate and keeping the same principal balance-carries less risk for the IRS. Your equity position doesn't change much, and your improved cash flow might make it easier to pay the tax debt.

Cash-out refinancing is trickier. You're increasing your mortgage balance and pulling equity out. The IRS will approve this only if they're getting a significant portion of that cash. If you're cashing out $60,000 and paying the IRS $50,000, they'll likely say yes. If you're cashing out $60,000 and paying the IRS $5,000, probably not.

When you're planning the refinance, work backward from what the IRS needs to see. What payment amount makes subordination approval likely? Can you structure the loan to deliver that number and still accomplish your refinancing goals?

IRS lien subordination refinance mortgage transactions aren't simple, but they're manageable when you understand what the IRS requires and plan accordingly. Subordination gives you access to better loan terms, lower payments, or cash you need-without waiting years to pay off the tax debt first. If you're sitting on equity but stuck with a lien, subordination might be the only way forward. For 32 years, the Law Offices of Darrin T. Mish, P.A. has helped taxpayers work through subordination applications, negotiate with the IRS, and close refinance transactions that seemed impossible. Let's talk.